Send this article to a friend:

December

14

2023

|

Send this article to a friend: December |

|

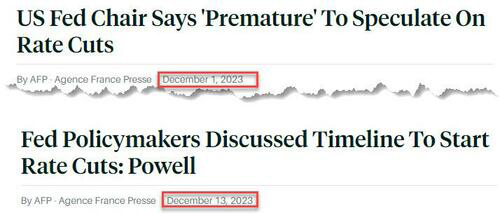

Now It All Makes Sense

One day after the Fed's bizarre, unexpected pivot, many are struggling to wrap their heads around what happened: what exactly changed in less than two weeks for Powell to go from telling the market it was "premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease" to suddenly warning that rate cuts are something “that begins to come into view, and is clearly a topic of discussion out in the world and also a discussion for us at our meeting today."

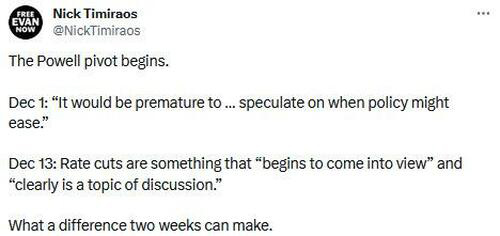

Even Powell's own mouthpiece, WSJ reporter Nick "Nikileaks" Timiraos, was confused remarking sarcastically after the FOMC "what a difference two weeks can make."

Ok, so let's take a closer look at the two weeks between Dec 1 and Dec 13 when supposedly everything changed. What we find is that the main economic events that took place were the ISM Services on Dec 5, the November Payrolls report on Dec 8, the University of Michigan Consumer Sentiment report, the CPI report on Dec 12 (and let's add today's retail sales data just for additional context). Turning to each of these in order, we start with the ISM Services report which was a clear beat and rebound from the previous month...

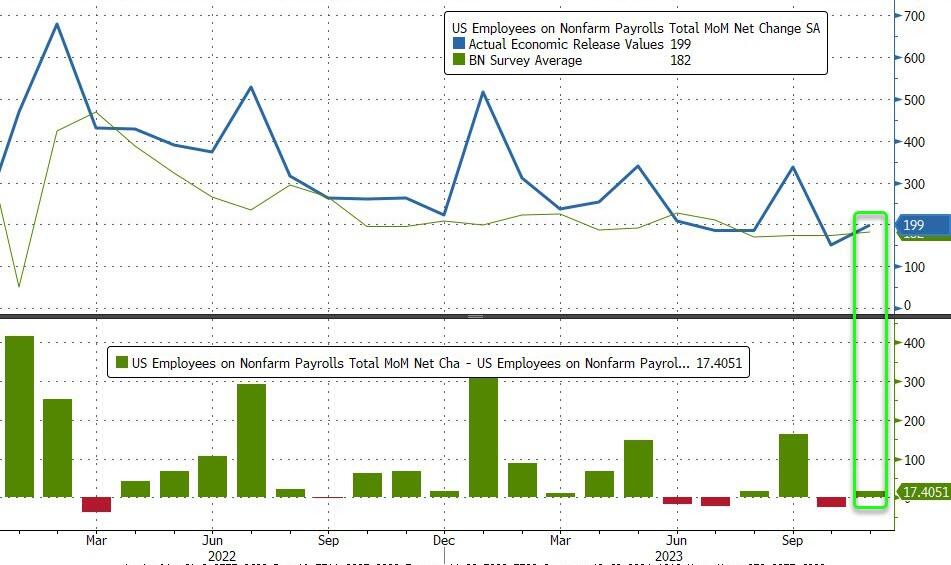

... the jobs report was an impressive beat and also a significant improvement from the previous report...

... not to mention the unemployment rate which came in far below expected and was a big drop from the previous one (the Sahm's Rule watchers, who were worried it would telegraph an imminent recession, could relax)...

... average hourly earnings also came in hotter than expected (i.e., inflationary)...

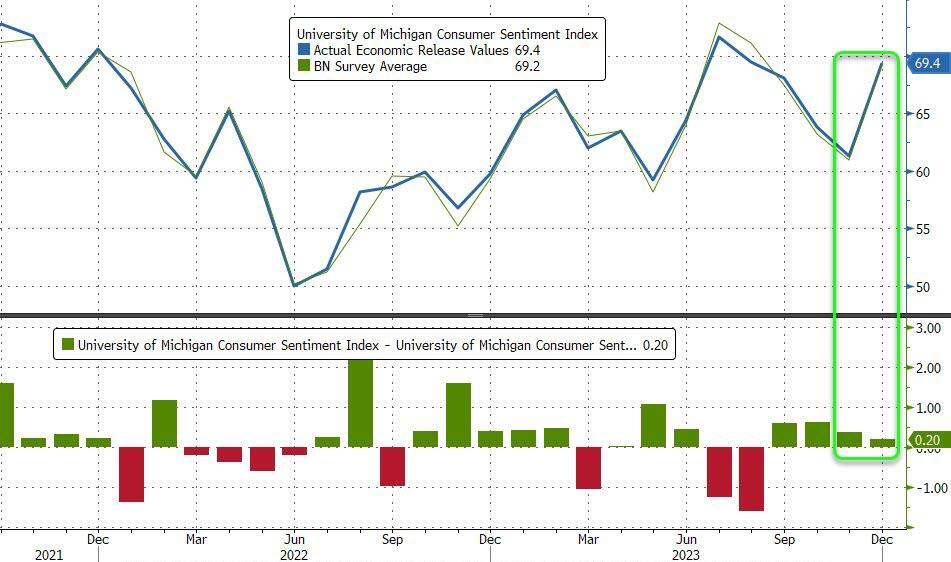

... which in turn helped the UMichigan Consumer Sentiment report, which exploded higher from 61.3 to 69.4 (smashing estimates of 62.0)...

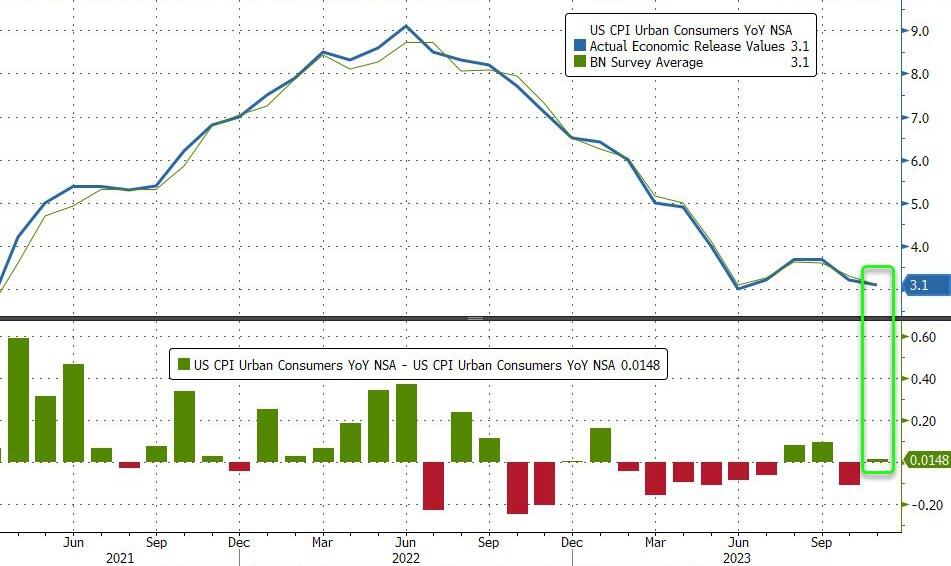

... as for the inflation print, well November CPI came in hotter than expected (so contrary to whatever disinflationary trend the Fed may be falling back on to justify its dovishness).

Last but not least was today's retail sales which came in scorching hot - the 5th consecutive beat in a row - and confirmed that contrary to what the Fed is telegraphing, the US consumer is not only not slowing but supposedly spending much more than Wall Street expected. Maybe Powell did not have that data, but he certainly had access to the same real-time card spending data that Bank of America has, and which allowed to correctly predict just how big of a beat today's retail sales data would be.

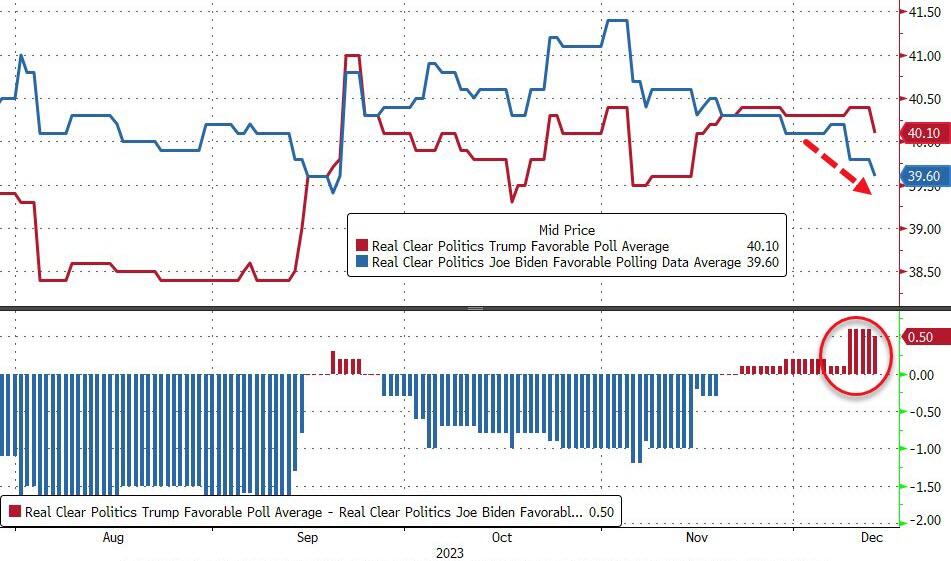

Yet, after all this stronger than expected and/or improving data, or hotter inflation, Powell made an unexpected 180 pivot on what he said two weeks earlier when the data was generally worse - and less inflationary - than it is today. And as the FOMC ‘pivoted’ in a dovish direction, its impact on markets was profound. Looking at the market this morning, the US 10y yield has plunged nearly 20bps since the decision, the 2y yield a little over 30bps. Markets are now pricing for six cuts of 25bp in 2024, with the first one fully priced in for March. Yet, clearly, the key driver of the sharp reaction by markets was the fact that Powell decided not to push back against market expectations of early (and significant) cuts for 2024. And the punchline: although the FOMC hasn’t taken the possibility of further hikes off the table, Powell admitted that the FOMC has started to talk about when to dial back rates, a huge reversal from what he said less than two weeks prior when he claimed that it was "premature" to speculate on rate cuts. He said that the Committee had not worked out the cutting cycle yet, but he did say they would not wait with cutting until inflation was at 2%, because they don’t want to overshoot. Of course, as we have shown above, none of this overshooting dangerwas in the recent data; if anything, the data has come in stronger since the start of the month as did inflation, so assuming the same Powell from his Dec 1 appearance at the Spelman College fireside chat was still around, what he should have said is doubling down on that very same message.... instead he did just the opposite. This, according to Rabobank, basically erodes the importance of any near-term inflation data that would still point to inflation above its target, whilst it elevates those data that support the view that inflation is on its way down. The Wall Street Journal’s Nick Timiraos tweeted that Powell said that some members even changed their minds halfway through the meeting, when (lower-than-expected) PPI numbers came out. But as even first-year financial analysts know, what PPI measures more than anything, is commodity input costs, i.e., oil, gasoline, food, and so on... all items the Fed religiously avoids in its preferred inflation measure, the core PCE. So the picture that emerges is a puzzling one: on one hand with weaker data in hand, the Fed Chair said it was "premature" to talk about rate cuts, yet less than two weeks later, with stronger data in place and with hotter than expected inflation, Powell suddenly flip-flopped 180 degrees, shocking even veteran traders, when supposedly the Fed now was looking at precisely those things (PPI) which it went to great lengths to avoid when inflation was soaring. Or maybe there is no puzzle at all: maybe what that happened in the past two weeks had nothing to do with economic data, the state of the US consumer, or how hot inflation is running and everything to do with... phone calls from the increasingly angry White House, the same White House which after seeing the latest polling data putting Biden at the biggest disadvantage behind Trump despite the miracle of "Bidenomics"...

... decided to pull its last political level, and had a back room conversation with the Fed Chair, making it very clear that it is in everyone's best interest if the Fed ends its tightening campaign and informs the market that rate cuts are coming. It certainly would explain why despite keeping the 2026 projected fed funds rate unchanged at 2.875%, the Fed just as unexpectedly decided to pull one full rate cut out of the non-election year 2025 and push it into the pre-election 2024. Nonsense, the Fed is apolitical, it would never yield to political pressure, you say!? Well, that dear reader, is bullshit, as even the NYT reminds us in this particular vivid anecdote from 1965 recounting the dramatic interaction between former US president Lyndon B Johnson and then-Fed president William McChesney Martin, when the head of the US central bank - much to LBJ's displeasure - hiked rates by half a percentage point, infuriating the Democratic president, to wit:

Ironically, in the end LBJ got what he wanted as the next episode from the NYT reveals:

Almost 60 years later, Powell decided not to "call the shot as he saw it" just two weeks ago, and instead of being shoved against the wall by Biden's thugs, to instead capitulate what little credibility the Fed had just so Biden's odds of getting reelected in 2024 were ever so fractionally higher...

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)