Send this article to a friend:

December

14

2023

|

Send this article to a friend: December |

|

Inflation Just Keeps Rising!

How they love to spin it. Drudge wrote the headline for today’s CPI report as follows: “Inflation coolsslightly.” Lie. It heated up. Plain and simple. MarketWatch started with a more honest headline but then spun it as follows to force it as positive as they could: “Stronger-than-expected services inflation [the honest part] won’t spur Fed rate hike, says BlackRock’s Gargi Chaudhuri.” Read the article, however, and you find it says, “we do not believe the Fed will prematurely cut interest rates in 2024 while inflation remains above target.” So, the actual effect of today’s CPI report was a bit more than just “not spurring” another rate hike. It practically assures the Fed will not even consider cutting rates in 2024 as the market universally believes the Fed will do. The headline downplays the impact because no one in today’s market believes the Fed will hike rates in 2024, so it’s easy to say the Fed won’t do that, thanks to this report, but everyone believes the Fed will cut rates (as many as four times) in 2024. Inside, the article cannot escape revealing that this inflation report actually presses the Fed to not cut rates all the way through 2024, which is how I retitled the article among the headlines below to help them get it right with what the article actually reveals:

In fact, once you get past the languid headline, you find the narrative is now shifting toward believing it would be “premature” for the Fed to cut interest rates in 2024, even though 2024 rate cuts have been the market’s broad assumption for several months as practically a given. With that shift, at least, some in the mainstream press are edging toward what has been my consistent position. The stock market, which rose today, may read beneath the algo-grabbing headlines tomorrow to see the starker truth they missed today. For today, however, the algorithms grabbed the headlines that were designed for them and bid the market aloft. Moreover,

All of that is actually completely in line with what I have been expecting to see—a slow upward increase in inflation, coming mostly from housing and healthcare in the sticky services sector. Still, they must spin it as positively as they possibly can:

Yeah, well it made a lot of progress EARLIER in the year, as I have said, but it has been going up for five months now. The financial media always want to focus on year-on-year because mathematically that has to be slower to turn back upward. It’s the longer-term measure. I was saying “three out of four months with the fourth being neutral” went upward, and, before that, “three months” went upward. You can see the trend. Inflation is going HIGHER for LONGER, stretching month after month. Inflation is going higher for longer, not just the Fed! We are now just tacking more and more months onto the new slowly rising inflationary trend. That means, of course, the Fed is also going to go “higher for longer” or, in the very least, will be holding high for longer because this is clearly the wrong direction for inflation to be flowing. Enough months of gradual rises will, as I’ve been harping on (because almost no one else is saying it), cause year-on-year inflation to start rising, too. While all of these latest months have been incremental rises, inflation has clearly moved in the wrong direction for five months now! So, let’s just dispense with the “inflation is going down” that we’ve heard every month just because YoY inflation (the bigger ship that turns more slowly) has not put in its turn yet; but even that paused this month. Still, the positive spinners whir away, putting all the optimism out there they can:

Wow! What a spinning merry-go-round from the mainstream financial media. All hype, even when the news is truly bad for inflation—five months now of rising. The brief pause last month did not manage to turn the recent new three-month trend back downward, as the move shown in this month’s report for November now proves. I didn’t think it would. It’s all baloney all the time from these guys. CNBC’s headline even went this far:

I suppose, if voters want month after month of increasing inflation, it will help Biden out, or if the press can keep spinning rising inflation as a success story enough to make the big lie come true in the minds of voters, then it should help him. The hoopla, of course, is helping markets get around the bad news, so stocks edged up today, more than happy to grab the fringe of the report and not even think about the fact that it’s the fifth month of an upward trend. If consumers are feeling better, as the title claimed, it is because the press has been outright lying for almost a half a year by saying inflation was falling each month, when it was rising each month but still falling year-on-year because of the earlier months when the Fed was having great success in it fight—something it has not had in months now. The last jobs report also said the Fed is no longer winning, which should mean it will likely have to tighten harder. The Fed can, of course, wait a spell to see if the lag time involved eventually starts to hand Team Fed some winning months; but still having the wrong team score a goal again and again cannot be called “winning.” It cannot be called “inflation is falling” when inflation is the team scoring each month, even if Team Inflation has not yet achieved a winning score for the whole game. What it does mean is the Fed’s feet will be held to the fire longer, which means more time for more economic damage to keep building. Neither the latest jobs report of the latest inflation reports give the Fed any latitude for backing down.

That’s one way to look at it, but a more direct way to look at it would be “Rising monthly inflation for almost half a year along with rising wages and falling unemployment showed that the Fed is no longer making any progress in fighting inflation, so it will have to tighten longer, increasing the likelihood that it creates a recession as it always has during its tightening cycles.” That wouldn’t be pessimism either. That would just be truth. With such lack of transparent truth as we read today in financial media that, by all appearances, wants to pump the markets and after hearing from the Biden Admin again today, it is no wonder that …

The statistics lie. So does the reportage. Didn’t the article headline just say they report more optimism? Maybe consumers feel the reality of inflation but keep readingthat it is going down; hence the unusual conflict in their feelings. Their reality keeps not squaring with what they are reading. (Which is why I write The Daily Doom to just call it as it is so your head doesn’t spin from all the gyrations in the news.)

Didn’t the headline also just say recent reports or surveys would boost his approval rating?

Hmm. Didn’t the headline say that this article is about the economy “helping Biden with voters?” The stock-trading algorithms grab the headlines, but read the article and, when it finally gets to the topic of Biden’s campaign, it says the opposite. No wonder the economic mood of Americans is “confused” when they are surrounded by articles that contradict their own headlines because they are so packed with lies. It’s hard to see how another month of rising MoM inflation is going to help improve Biden’s relationship with voters. I thought inflation was the source of their “pessimism.” So, what a pile of mush.

I don’t see anything about today’s inflation report that is going to help Biden with that. Maybe CNBC just didn’t get today’s inflation memo before writing the article about inflation fears. Perhaps they should have waited another hour for the actual report to come in before writing their drivel about inflation. Or look at this CNBC title:

And then the summary comments that immediately follow: “Excluding volatile food and energy prices, the core CPI increased 0.3% on the month and 4% from a year ago…. The consumer price index, a closely watched inflation gauge, increased 0.1% in November, and was up 3.1% from a year ago, the Labor Department reported Tuesday. Economists surveyed by Dow Jones had been looking for no gain and a yearly rate of 3.1%.... While the monthly rate indicated a pickupfrom the flat CPI reading in October, the annual rate showed another decline after hitting 3.2% a month earlier…. The Fed “will probably talk about continued disinflation being good news.” In fact, however, if it hadn’t been for a significant decrease in fuel costs, overall inflation (headline YoY CPI) would have been notably higher, instead of incrementally lower, but even lower energy costs could not help MoM inflation look better than last month or core inflation. Zero Hedge gets the headline as it should be:

So, the decline in YoY inflation has now completely stalled (held flat), and the flat month we saw in MoM inflation in October has now resumed its new trend of rising. Everything is moving in the wrong direction for the Fed. Since the Fed pays attention to core inflation, there was NOTHING here to support the market’s Fed-pivot fantasy.

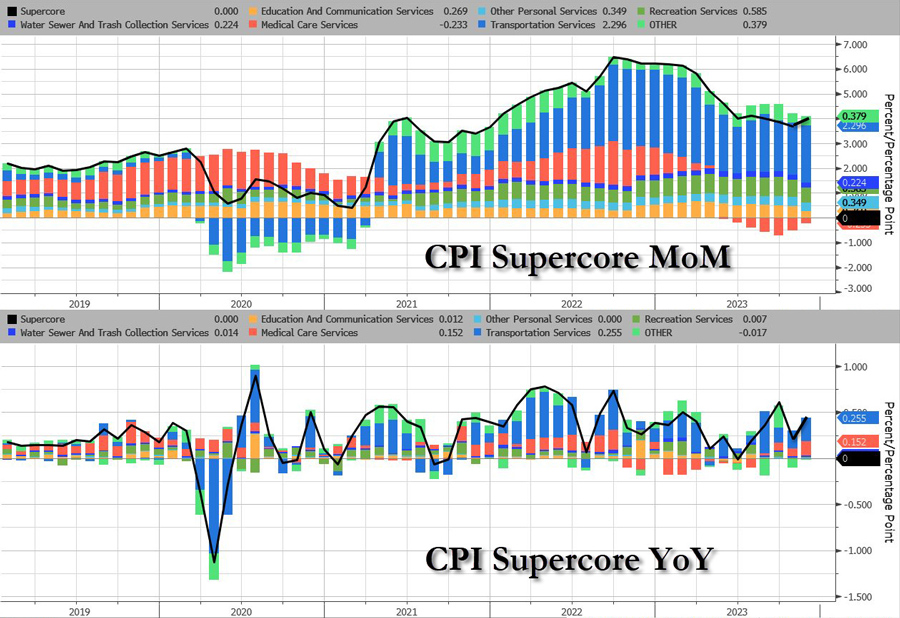

That’s what the focus in this report should be. Of course, ZH has often been one of the rate-cut hypers, itself, talking about the pivot being right around the corner because it believes Powell will weasel out. Sometimes they have practically been pivot champions. (Now that inflation is clearly not going that way, however, they subtly shift sides — as I’ve seen them do in the past — to pretend as if the rate-cut hypers are the other guys.) Still not gonna happen. NO PIVOT! Does the tail end of these graphs of the Fed’s top-watched numbers look like inflation is falling as the Fed will be looking for?

The MoM figures look like six months of getting nowhere. YoY looks like it has been on the rise from a low it put in half a year ago, during which time it took a one-month drop in its rate of rise and then went back to rising faster.

There is the small rise in medical expenses I commented on in October and the doubling of that, which I said we’d see in November because of how the Bureau of Lying Statistics manipulated medical insurance to reconcile its errors and baselined the index all the way back to 2018 for the start of this government fiscal year and how it is handling its transition back out of the adjustment. Even with all that effort, it is still showing a rise, which will grow because of the bizarre way the BLS handled the reconciliation of their errors. Shelter, as I’ve said in my latest articles, has such a lag in how it gets reported that it will continue to rise for some months to come. We see it doing exactly that. If OPEC+ scores a success and drives fuel prices back up, watch out for significant rises in inflation. Otherwise, the decrease from energy is helping keep the increase in inflation at a modest level, but still nothing like what the Fed needs to see in order to start cutting rates; and energy has likely stopped falling at this point, so should, in the very least, become more neutral.

Keep The Daily Doom coming by subscribing as either a free or paid subscriber; but, of course, the latter is what really keeps it coming.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)