Send this article to a friend:

December

12

2023

|

Send this article to a friend: December |

|

Grinding Down Into Deflation: The National Debt Disaster No One Is Talking About

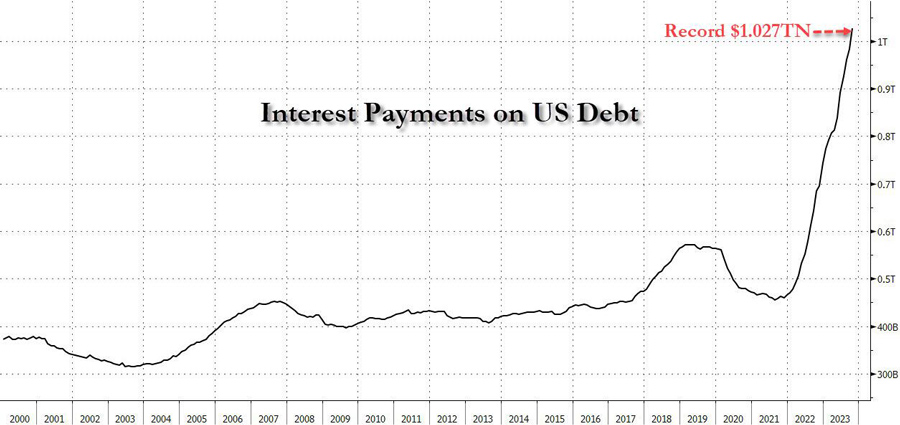

The process of stagflation is difficult to track because there are multiple paths that it can take, many of them largely dependent on the whims of the central bank and its policy decisions. All we can really do is look back at the limited number of historic examples and guess at what will happen next. In the 1970s, stagflation nearly crushed the country with inflation rising by 7% to over 14% per year for a decade while the general public eventually faced high unemployment. When I hear Zennials complain about being born into the “worst economy ever,” I have to laugh because they really have no clue. The 1970s was FAR worse in terms of erosion of buying power as well as overall poverty. If you look at film footage and photos of urban areas from LA to NY to Philadelphia during that time, many parts of these cities looked like bombed out war zones. The country was truly on the edge of disaster. In the early 1980s, the Federal Reserve jacked interest rates up to over 20% – This stopped the inflation crisis but triggered a deflationary plunge that would sit like a giant boulder on the chest of the American consumer and small business owners for years to come. My own grandfather lost millions in his trucking and freight company during the rate spike; many people lost their businesses and homes. In other words, as bad as the situation is now, we haven’t seen anything yet. Of course, we are quickly moving towards similar conditions and there is one thing we have today that the 1970s didn’t: A massive snowballing national debt. Currently, the US national debt is $33.8 trillion and has a 120% debt-to-GDP ratio. In a single month (October) the US added over $600 billion to the debt, and at the current pace the total official debt will hit over $41 trillion in one year. The speed of this accumulation is frightening. To put this in perspective, the Obama Administration and the Federal Reserve added around $9 trillion to the debt in 8 years during the corporate bailouts. Under Joe Biden, this is set to happen in a little over 1 year. How is this happening? As I have noted in the past, the US economy has stacked so much fiat and so much debt that any deviation in interest rates is going cause huge ripple effects. We don’t even need to hit the 20% interest rates of the early 1980s – A constant rate of near 6% is enough to cause debt to skyrocket. Then there is the problem of “compounding interest.” The US government is borrowing money to make interest payments, but it also borrows to roll over the principal payments, and it borrows still more to fund the general spending which is in excess of taxes collected (deficit spending).

At higher interest-rate levels, borrowing enters a destructive spiral. There’s interest payments on debt, which was itself borrowed to make interest payments on debt. To put it in simple terms, it’s a bit like a broke person taking on a stack of new credit cards to make the interest payments on a stack of old credit cards. It’s financial suicide. Eventually the avalanche of debt will stall inflation but it will also pop multiple asset bubbles cross numerous market sectors and trigger a deflationary crisis. We are already seeing this trend with a crash in manufacturing as well as frozen wages. We are seeing it in the freight industry, with layoffs and bankruptcies piling up in a shocking downturn indicating impending recession. Not to mention US home sales have plunged to a 13 year low as prices continue to rise. These are all red flags of an impending deflation event that WILL lead to large scale job losses, likely within the next year. It would seem the magic of covid stimulus measures is finally fading away and we are beginning to see the real economy underneath. All the negative news has led to a spike in stock markets recently. Why? Because bad news is good news for equities. The expectation among investors is that the Fed is poised to cut rates or return swiftly to QE. This is not going to happen, at least not anytime soon. The Fed, I believe, wants a crash. After addicting markets to easy money for over a decade, the central bankers know EXACTLY what will happen as they continue to cut off the drug supply. I suspect we are about to see a major change in the behavior of the economy going into 2024. The stagflation phase is nearly over. The discussion around dinner tables across America will turn to the exploding national debt, and debt in general. The big debate will once again turn to this: Will the Fed keep rates steady, risking deflationary implosion and debt default, or, will they cut rates, return to stimulus to pay the debt and risk double digit inflation? These are the two choices in front of us as debt overwhelms the system. If you would like to support the work that Alt-Market does while also receiving content on advanced tactics for defeating the globalist agenda, subscribe to our exclusive newsletter The Wild Bunch Dispatch. Learn more about it HERE. As the world moves away from dollars and toward Central Bank Digital Currencies (CBDCs), is your 401(k) or IRA really safe? A smart and conservative move is to diversify into a physical gold IRA. That way your savings will be in something solid and enduring. Get your FREE info kit on Gold IRAs from Birch Gold Group. No strings attached, just peace of mind. Click here to secure your future today. You can contact Brandon Smith at: You can also follow me at – TwitterX: @AltMarket1

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)