Send this article to a friend:

December

02

2023

|

Send this article to a friend: December |

|

Bidenomics Is Bankrupting Americans, and Here’s the Proof

In fact, the U.S. economy could be heading for one of the most painful periods of economic turmoil of the last 15 years. And it’s all thanks to the disastrous policies known as “Bidenomics.” People aren’t prospering in the Biden economy It would be easy enough for the Biden administration to simply own up to the economic turmoil we’re all facing. Of course, that would be political suicide. They’re never going to do that. So, instead, they’re resorting to obfuscation to make things seem better than they actually are. One way they’re doing this is by focusing on the forest while ignoring the trees. This idea was encapsulated pretty well in a recent column on the People’s Policy Project (PPP):

Our own article from earlier this week expanded on the above idea in more detail. Paul Krugman also fell into a similar trap of turning a blind eye to miserable outcomes a few weeks ago. That’s because he appears to suffer from the same perpetual cherry-picking and moving of the goal posts that the Biden administration does. The problem for policymakers deepens once you factor in a key misunderstanding they often fall prey to, according to the PPP:

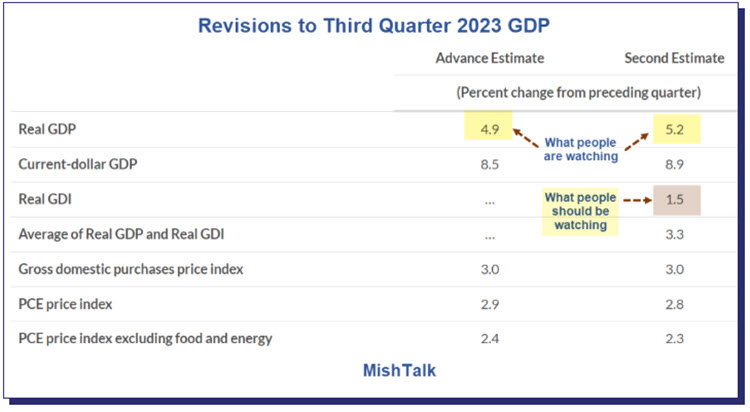

But even if you leave aside the misunderstandings, goalpost shifting, and macroeconomic mistakes, you’re still left with verifiable data. There are a few more data snapshots that reveal how bad it is for most people. This chart shows real gross domestic income (GDI), a measurement of worker pay. As the Bureau of Economic Analysis tells us, GDI is:

Theories are fine. But why is GDI so much different from the GDP measurement we keep hearing about?

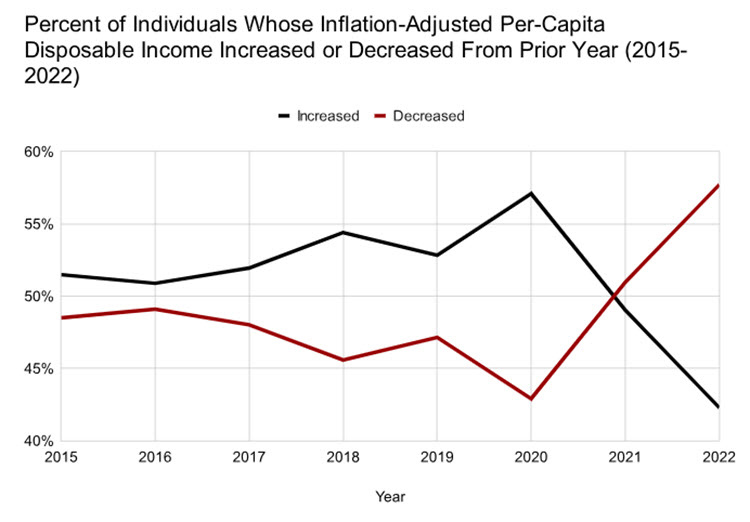

Mike Shedlock explains why this difference is significant: “Based on GDI, a very reasonable case can be made that the economy went into recession and/or is still flirting with recession.” “Great” economic recoveries don’t usually include a recession at all. But there’s a lot more… Take a look at the chart below. It shows an obvious difference between people who increased their disposable income from the prior year, and people who have had their disposable income drained since 2020. Note this is disposable income, meaning “what’s left over when all the bills are paid.” Discretionary funds, or what a business might call free cash flow. When the bills go up, free cash flow suffers. Now, even though this chart is “adjusted for inflation,” you can see that the official inflation measurements simply don’t capture the actual expenses of everyday Americans. Otherwise they wouldn’t have less money to spend!

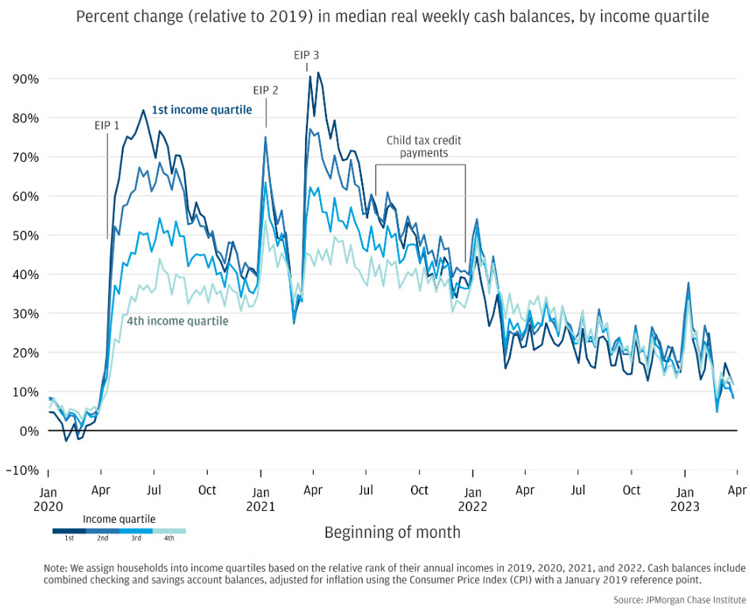

Expenses are up significantly, even after adjusting for “official” inflation numbers. A recent JP Morgan Chase report backed up my conclusion by revealing a sharp decline in cash balances at banks:

via JPMorgan In the good old days, when we ran out of cash, we just opened up a home equity line of credit (HELOC). Remember “your house is an ATM”? Those days are over. The PPP reports most people just can’t access their mortgage equity, nor can they downsize by moving to another home:

So, inflation has driven up prices on one hand, and increased rates are preventing access to potential financial relief on the other hand. What does Biden plan to do for the American people to get them out of this tough spot and back on the road to prosperity? Bureaucracy to the rescue!A quick look at an article on the Guardian website sheds light on Biden’s intention to “smooth out supply chains” through something called the Defense Production Act. Well, if supply chains were actually the problem, that might be helpful. But the global supply chain pressure index is lower right now than it’s been anytime in the last 25 years. That’s like buying a mousetrap because you have ants in the kitchen! Come to think of it, it’s also a lot like blaming “greedy oil companies” for high fuel prices after you sanction a major oil-producing nation! Inflation is caused by one thing: increasing the money supply. Exactly as the Federal Reserve has done – increasing it by 35%, to be precise, since the pandemic panic. (That’s actually down just a bit thanks to eight months of quantitative tightening.) Exactly as the federal government has done – by authorizing multi-trillion-dollar deficit spending sprees, year after year. Let me be perfectly clear – supply chains are NOT the problem. The ongoing devaluation of the dollar, through inflating money supply and deficit spending, is the problem. A new federal task force cannot solve that problem. It’s not a problem any single one of us can solve – we can only do so collectively. However, we can each do our best to preserve our purchasing power while fiscal insanity reigns in the White House… Wealth preservation has never been more important As you can plainly see from the data presented this week, the economy isn’t obviously in “good” shape, like Biden keeps touting. When we zoomed in and looked at only a few of the “trees” in the forest, the message was pretty clear: the average household is worse off, running out of savings, and probably buried under mounds of debt. Meanwhile, the purchasing power of our hard-earned dollars is evaporating, thanks to the toxic combination of money-printing and deficit spending. At times like these, it’s smart to consider every precaution that could help your retirement savings weather out the storm. Diversifying your retirement savings with precious metals like gold and silver could help you if you need to consider a safe haven store of value for your future. That’s because gold and silver have been historically proven to help preserve purchasing power, while they’re also considered inflation-resistant investments. Best of all, they’re some of the VERY few financial assets you can hold in your hands. They aren’t an IOU or a promise to pay. Don’t wait until it’s too late, take back control of your financial future while there is still time. You can get the information you need to consider precious metals in our free kit.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)