Send this article to a friend:

December

09

2023

|

Send this article to a friend: December |

|

This Hasn’t Happened Since 1933

Is it a frightful omen of lean times… a straw swaying in the wind… a looming menace? We do not know. Yet we hazard it rates an inquiry. An inquiry, incidentally, the mainstream financial press will not afford it. What is it? Answer anon. Let us first direct our gaze briefly to Wall Street… All Eyes Are on Friday After a series of defeats, stocks rediscovered their courage today. Each of the major averages reclaimed lost earth. The Dow Jones Industrial Average advanced 63 points. The S&P advanced 36 and the Nasdaq Composite advanced 193 points. Yet investors have their eyes on the morrow. That is when the Bureau of Labor (Misapplied) Statistics issues November’s unemployment data. Explains CNBC:

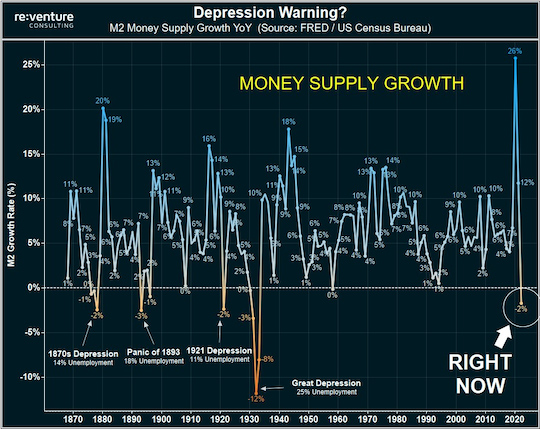

An ice bath indeed. Meantime, gold yielded back $2.20 today. The 10-year Treasury yield slinked slightly forward to 4.129%… for what it is worth. Oh My! Yet what phenomenon is the United States economy presently enduring that it has not endured since 1933? Here is the answer: The money supply — measured broadly — is contracting at a furious gait. The M2 money supply constitutes saving deposits, time deposits, certificates of deposit and money market funds. It has grown and grown for well past a century. It has endured some trembles, some slight contractions. Yet like the federal government of the United States… or its debts… it has expanded nearly inexorably. We instructed our minions to ransack the historical data. This Hasn’t Happened Since 1933They informed us that the M2 money supply has contracted by at least 2% — on an annualized basis — in six previous instances. These shrinkages transpired in the years 1878, 1893, 1921, 1931, 1932 and 1933. Each year coincided with economic frights of one sort or other. And now? We learn that the M2 contraction exceeds 2%. Here is the graphic evidence, courtesy of Reventure Consulting:

An Accelerating Contraction What is more, the contraction rate is itself accelerating. Mr. Ryan McMaken of the Mises Institute:

Just so. Yet it is not so much the direction of travel that riles us. It is rather the pace of travel:

We must agree. It is remarkable. M2 has nonetheless withdrawn 13% from its April 2022 summit — remarkably. Yet perhaps the foregoing analysis lacks… context. One Gigantic Anomaly We must consider that the monetary deliriums of 2020–21 were unique madnesses. They lack all precedent. We refer you once again to the above chart. And it is true. Never had the monetary sluice gates been flung so widely open. Never has a similar deluge washed over the nation. It is only natural — then — that money creation returns to some normal semblance once the crisis passed. Thus the vast contraction may less indicate contracting economic conditions… than merely illuminate the lunatic excesses of the pandemic period. In this telling we are merely witnessing a normal corrective. The Federal Reserve has merely accelerated the normalization. It has undertaken heroic anti-inflation exertions since March 2022. They have diminished the supply of money. Yet the facts remain the facts. In each instance that the M2 money supply has contracted 2% or more — in 1878, 1893, 1921, 1931, 1932 and 1933 — the United States economy was in for heavy weather. And the M2 money is presently contracting more than 2%. “The Year of Reckoning” Will this time prove the exception? Will the United States economy hold against the weather? As stated at the onset… we do not know. We have raised false warning flags before. Often, in fact. We will not do it again. Yet Jim Rickards forecasts that 2024 will be “the year of reckoning.” He has cited many reasons why. Among them are:

As we are fond to say, climate is what a fellow can expect. Weather is what he actually gets. It is possible the weather holds. It is possible the Federal Reserve and fiscal authorities will blow away the storm systems. Yet it is likewise possible they will not. And the plunging money supply is one reason why…

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)