Send this article to a friend:

October

14

2023

|

Send this article to a friend: October |

|

Bad Money—The Bane Of Liberty And Prosperity, Part 1

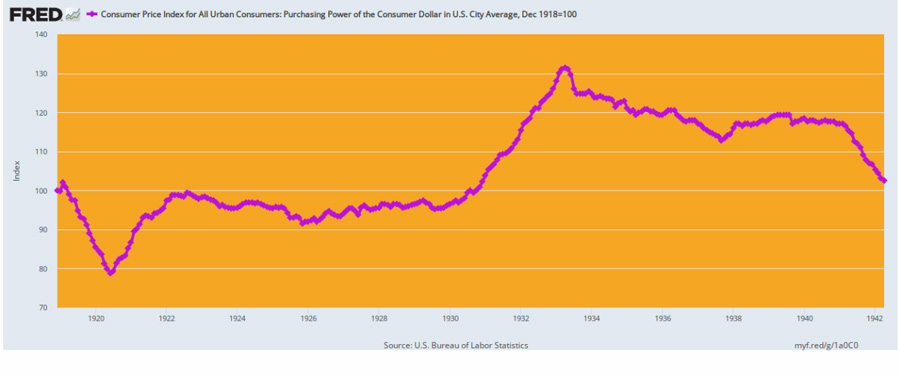

To be sure, it didn’t start that way upon its legislative enactment on Christmas Eve 1913. The original statute as crafted by the great Congressman (and later Senator) Carter Glass actually omitted—and deliberately so —the two core features of today’s rogue central bank, which features underlie all our present-day troubles. To wit, there was no provision for the nation’s new central bank to own, borrow or collateralize the public debt. There was also no mandate or mechanism for it to be in the macroeconomic management business, nor was it contemplated that the 12 new Federal Reserve Banks, spread among the regions of the United States, would play any role at all in the stock and bond markets and that only one of these 12 banks— the New York Fed—would ever get within 100 miles of Wall Street. Most importantly, rather than function as the dominant, centralized influencer and price-setter in the banking and financial markets, as per today’s Fed, the new Federal Reserve system was designed to be a decentralized price-taker and last resort liquidity provider to Member banks within each of its 12 regions. That is to say, the gold coin standard was the basis for anchoring the value of hand-to-hand currency and commercial bank deposit money, and the free market was the forum for pricing money claims, debt, equity and other financial assets. Accordingly, today’s modality of monetary central planning and financial domination by a monetary politburo comprised of a dozen central bank apparatchiks was not even a gleam in the eye of the Fed founders. All of this was a product of relentless mission creep over the years and the raw grasping for power by Fed officials and their enablers on both ends of today’s Acela Corridor. In this original setting, therefore, the Federal Reserve was a passive player even when it came to the issuance of central bank credit. Rather than proactively targeting either Milton Friedman’s money supply or Alan Greenspan’s Federal funds rate, Fed officials were only empowered to don green eyeshades, figuratively pull up a chair behind the discount window of each of the 12 Reserve Banks and sit back and wait for customers in the form of Member banks seeking cash advances. In responding to these discount window requests, they were to assess the collateral presented by Member banks to support their discount loans strictly in terms of commercial soundness and the prospects for near-term repayment. Consequently, the expansion or contraction of Federal Reserve credit at each bank and for the system as a whole would be driven by the ebb and flow of main street commerce, not the whims of central bankers targeting either financial or macroeconomic variables. Moreover, “eligible” paper was called “real bills” during that era—that is, claims on goods already produced or sold and usually due for repayment with 90-days or less. Properly administrated, the real bills doctrine was inherently noninflationary for two reasons, First, holders of bank deposit money (checking account balances) could always convert it to currency upon demand under this arrangement, and, in turn, currency could be redeemed for gold, also upon demand. Secondly, the commercial collateral that stood behind new cental bank credit (i.e., the 12 regional Fed printing presses) was self-liquidating. That is, supply had already been created before the Fed discount windows enabled new commercial bank credit, and the incremental demand it represented. In effect, the dollar was double anchored—to both gold and also to the supply-side of the US economy. Of course, the key feature here was the presumption of free market pricing of bank deposits and loans. That was the lynchpin of the entire scheme as Carter Glass and his advisors had envisioned it. The traditional criticism of the real bills doctrine, of course, was that the central bank might set its discount rate too low, thereby inducing excess demand for discount loans from Member banks in order to accommodate inflationary expansion of commercial credit. But that argument was circular. To wit, if the discount rate was “mobilized” rather than “administered”, excess demand for credit would push market interest rates higher, which, in turn, would be reflected in the cost of Fed discount loans. The latter would automatically float higher with the market, topped-off by a penalty spread above the mobilized discount rate. At length, high market-driven discount rates would choke-off speculative demand, nipping inflation in the bud. Needless to say, that scheme did not offer much daylight for inflation-minded central bankers to befoul free market capitalism. Indeed, the beauty of the scheme was that it brought together the virtues of gold money, Say’s Law and the free market. That was a combination hard to beat and thereby embodied a structural rebuke to today’s financial poisons. To wit, government debt wasn’t eligible collateral—so there was no risk of encouraging the politicians to run chronic fiscal deficits on the basis of artificially cheap yields on the public debt. Likewise, the Wall Street game of securitizing debt and creating daisy chains of debt-upon-debt-upon-debt would never have gotten off the ground. That’s because none of today’s securitized instruments—CLO’s, CDOs, CDS and countless other forms of “structured” debt—would have been eligible for discount. Accordingly, speculators could chase rising financial rabbits to their hearts’ content, but it would not be done on the basis of cheap credit created by the central bank. That is to say, Mr. Market would have remained in charge of the discipline department. As it happened, of course, the temptation to set aside Carter Glass’ sound money rules in order to finance America’s costly and pointless adventure in old world corruption and political intrigue was temporarily too great to resist after Wilson threw an unprepared America and upwards of 4 million doughboys into WWI in April 1917. Indeed, the temptation to enlist America’s infant central bank in the resulting explosion of war finance was so great that the effort was actually led by Carter Glass himself, who because the Secretary of the Treasury during 1918-1919, and proceeded to discount billions of Liberty Bonds sold to everyday Americans to finance the war. Nevertheless, after the 1920 recessionary purge of the inflationary wartime boom, the original Fed scheme was largely restored. The Federal Reserve banks steadily liquidated their Liberty Bond based loan portfolios and returned to a commercial market-oriented discount window lending modality, even as the New York Fed experimented with open market securities investment and rudimentary efforts to tweak the business and trade cycles. As it turned out, however, the price level on the eve of full-scale mobilization for WWII in January 1942 was virtually the same as it had been at the end of WWI in December 1918. That is to say, notwithstanding war finance distortions before and after this 24 -year period there was no net inflation during peacetime. And despite the sequential boom of the Roaring 20s and bust of the Great Depression, the fact is that the US economy expanded in real GDP terms by upwards of 80% during that period. In a word, during the first thirty years of its existence the Fed was not inflationary outside of draft duties on behalf of war finance. And the real GDP of $146 billion in 1919 rose to $264 billion by 1941, or by nearly 3% per annum, without inflation or Fed stimulus and in spite of the depredations of the Great Depression and the New Deal cures that prolonged and deepened it. CPI Price Level Indexed to December 1918 Through January 1942

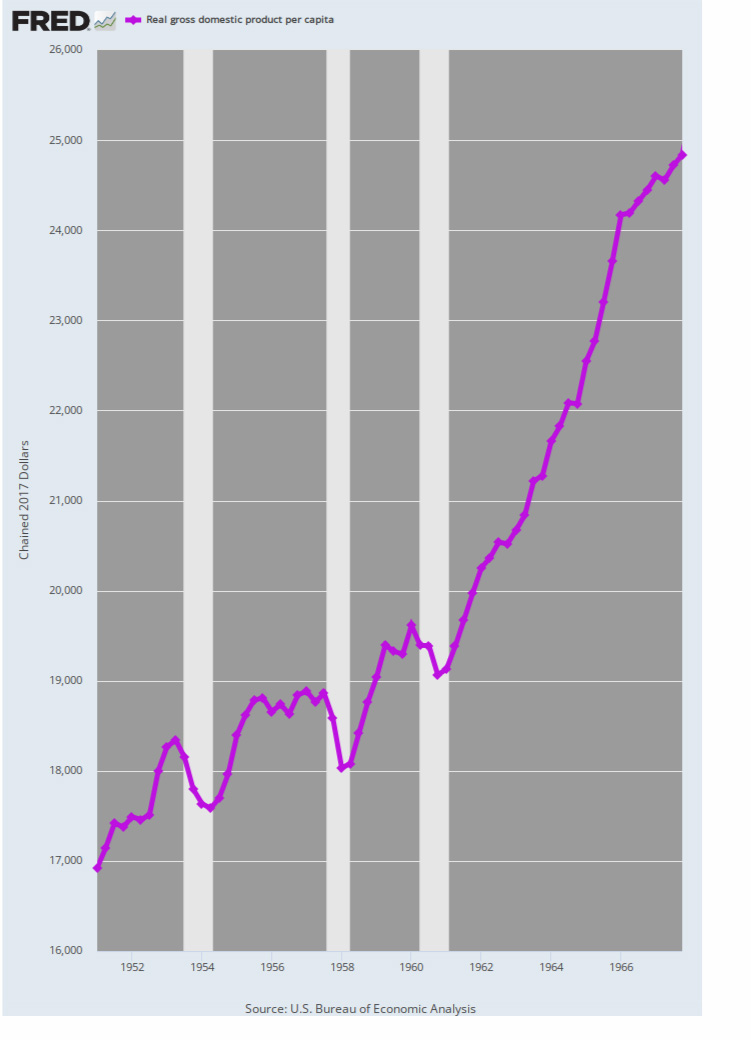

After early 1942 the US was back on heavy duty war mobilization and finance—a national emergency that included total allocation and control of economic activity and the drafting once again of the Fed into war finance duty. This time the latter occurred in the form of a rigid peg on interest rates— ranging from 0.375% on the 90-day treasury bill to 2.5% on the long bond. The residue of WWII war finance was not completely eliminated until the so-called Treasury Accord of March 1951, which finally got the Fed out of the interest rate pegging and public debt monetization business. Shortly thereafter the inflationary effects and controls of the Korean War were eliminated as well. So what followed was another period of reasonably sound monetary policy under William McChesney Martin. Specifically, between Q4 1951 and Q4 1967, the Fed’s balance sheet grew by just 2.0%per annum, while the CPI rose by only 1.6% per annum. During this same period real GDP increased by more than 84% or 3.9% per annum. Again, sound money at the Fed, very low inflation and the thriving growth of free market capitalism all coincided. Indeed, the ultimate measure of the latter is real GDP per capita. That figure grew by more than 2.3% per year—a level that far surpasses the gains of recent years. Since the pre-crisis peak in Q4 2007, for instance, real GDP per capita has grown by only 1.1% per annum, or just 48% of the 1951-1967 gain. Real GDP Per Capita, 1951 to 1967

Needless to say, that’s all she wrote on the noninflationary prosperity front. The “guns and butter” fiscal policies of LBJ and the awkward attempts by the Fed to accommodate these reckless policies lead to the unraveling of the gold-anchored Breton Woods monetary regime. As we will amplify in Part 2, thereafter Tricky Dick Nixon did not hesitate to drive a nail into the coffin of sound money, and it’s been off to the inflationary races ever since.

Former Congressman David A. Stockman was Reagan's OMB director, which he wrote about in his best-selling book, The Triumph of Politics. His latest books are The Great Deformation: The Corruption of Capitalism in America and Peak Trump: The Undrainable Swamp And The Fantasy Of MAGA. He's the editor and publisher of the new David Stockman's Contra Corner. He was an original partner in the Blackstone Group, and reads LRC the first thing every morning.

www.davidstockmanscontracorner.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)