Send this article to a friend:

October

12

2023

|

Send this article to a friend: October |

|

4 IRA Mistakes That Could Destroy Your Savings

One part of that planning is deciding how you are going to roll over the funds into any new vehicle(s) and begin to enjoy the fruits of your labors. The IRS website nicely summarizes the main reason why many Americans who are saving for a stress-free retirement would do this:

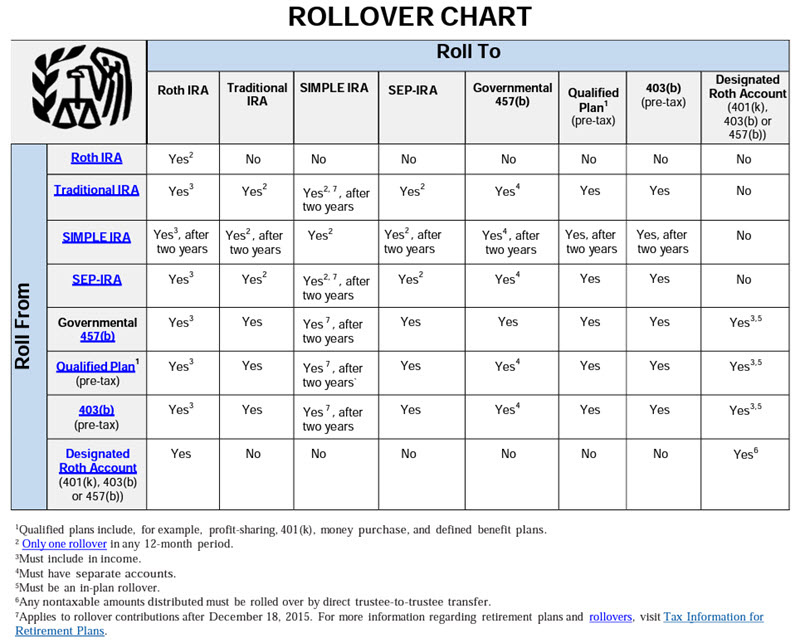

Generally, it’s prudent to complete this process within 60 days in order to avoid any potential tax consequences or penalties. We’ll clarify that in just a second. But just taking a quick look at the official chart and you can see why making a wise choice requires consideration:

On top of the potential confusion any older American might feel after looking at the chart above, Denise Appleby, CEO of Appleby Retirement Consulting found that people make 3 key mistakes when rolling funds into a new retirement vehicle. She listed them as follows:

So let’s briefly go over these in a bit more detail, so you can plan your retirement a bit more effectively. #1: Breaking the one-per-year limit This happens more often than you might think! Appleby said: “The biggest one is breaking the one-per-year IRA to IRA rollover rule, and that happens because people are impatient.” Impatience can cost you big in terms of annual “excess contribution” taxes and other penalties. (Like a 10% penalty if you’re under 59 ½ years old.) With that in mind… #2: Missing the rollover deadline Make the mistake of missing this deadline and you’re shooting yourself in the foot:

Missing the deadline basically means pre-tax income could be treated as regular income during tax season. Let’s make sure not to miss out on this advantage. (See the official IRS guidelines to learn more.) Let’s continue… #3: Ignoring tax exceptions Here’s the summary of the 10% penalty taken from the IRS website:

This is an “extra” tax, because unqualified withdrawals are both taxed as income and another 10% withdrawal penalty minimum (in some cases, the withdrawal penalty rises to 25%!). On the other hand, once you turn 60, in most cases you won’t be subject to these punitive taxes. But there are other exceptions to this tax to consider before you turn 60. For example, three of the exceptions taken from the IRS chart are as follows:

You can see how following the 60-day rule described above is important. There is still one more mistake that Appleby didn’t address in her comment from above, though… #4: Failure to diversify your investments You have a critical opportunity to consider when you roll over your savings from one retirement vehicle into another: The opportunity to appropriately diversify your portfolio. We cover diversification of assets on this website quite extensively, and with good reason. Properly diversifying your retirement savings can help ensure your financial future is stable regardless of the state of the economy. After all, we all want to maximize our chances of enjoying our golden years. (And, if we’re fortunate, pass on a legacy to our heirs.) Rollover time is a great moment to consider diversifying your retirement savings with physical precious metals like gold and silver. They’re historical safe-haven assets, great protection against inflation and they have intrinsic value that isn’t devalued by money-printing. Want to learn more about proper diversification? Learn more about the benefits of diversifying with physical precious metals here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)