Send this article to a friend:

October

22

2022

|

Send this article to a friend: October |

|

Everyone Seems to Have Forgotten About the Financial Weapons of Mass Destruction

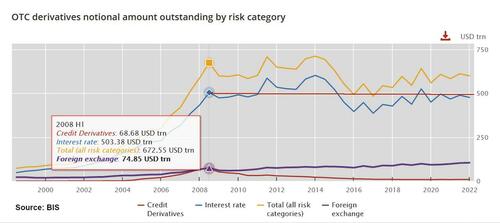

Though most of the financial headlines have been recently dominated by UK bond market illiquidity that threatened to destroy the retirement pensions of UK citizens that necessitated emergency BOE intervention and of similar possible developing conditions in UK Treasury markets due to the Fed’s continuing interest rate hikes, I believe a greater threat exists in global interest rate derivative markets. Remember how the dominant news of the 2008 global financial crisis, besides subprime MBS (mortgage backed securities) about financial weapons of mass destruction – the global derivatives market of $1.2 to $1.4 quadrillion? If you didn’t follow my writings back then, you may have been fooled over the years into believing that everything is now under control, with the total amount of global derivatives last reported in H2 2021 at $598 trillion. Apparently, the mass media has been completely fooled into believing this fake statistic because they have not reported global financial derivatives as a possible trigger for volatile moves in asset prices in what seems like at least a decade or longer. And if you assume the perspective that bankers have cut their positions in these extremely risky products that can collapse like a procession of dominoes if one large bank defaults on any major category of these derivatives, you would be wrong. The reason the global derivatives market has been cut in half since 2008 was due to a simple accounting trick that literally cut the amount in half overnight, not because banks actually reduced their exposure to derivatives by half. Thus, the created perception of a massive decrease in the global derivative market is not real. Another way of thinking about this is to compare it to Apple’s 4:1 stock split it executed in mid-2020 when Apple’s share price was $380. After the 4:1 split, Apple’s share price fell to $95 a share but those that owned Apple shares didn’t experience a massive loss in their stock valuation because they received 4 shares of Apple at $95 a share for every one share they previously owned at $380. Thus, when we look at the below chart, because the BIS has not elected to disingenuously portray this “halving” of the global derivatives market, we can see that there has been virtually no decline in the overall global derivative market size or in the overall global interest rate market size since they were once viewed in 2008 as a potential source of collapse for the entire global banking system.

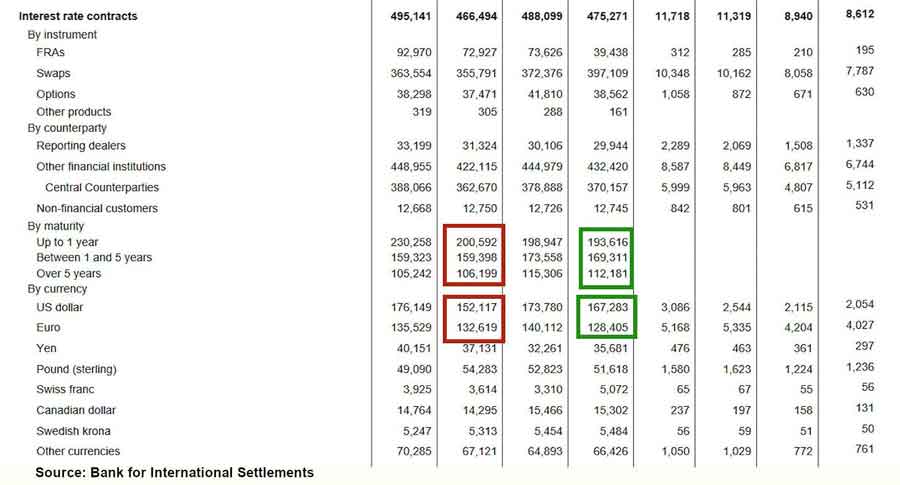

Recently, on my substack platform, I published an article titled, “Are US Central Bankers About to Go Rogue?”, in which I posed the question, Will US Central Bankers elect to continue their escalation of the Fed Funds rate to ensure USD hegemony in the global fiat currency arena despite the obvious negative consequences these actions will have in other domestic and global arenas?Though the verdict has yet to be declared to this question, let’s take a look at the global interest rate derivative market to understand the implications of US Central Bankers going rogue to preserve USD hegemony. There are two sets of data points I want to direct your focus towards. The set in red, which reflects the market data for H2 2020 and the set in green which reflects the latest reported data for H2 2021.

For interest rate derivatives with a maturity between 1-5 years and over 5 years, we observe that from H2 2020 to H2 2021, both of these figures increased, indicating that not only were all the longer-term interest rate derivative contracts rolled forward from 2020 to 2021, but that bankers around the world also added to these positions. Since we do not have H1 2022 data for this category of contracts yet, we do not know if this same pattern persisted from 2021 to 2022. But even if this category did not grow but remained the same, if we summate these two categories from H2 2021, this amounts to $281.5 trillion (but in reality, in excess of $560 trillion as this number was halved by the aforementioned accounting trick many years ago). Thus, there is obviously a massive amount of bank capitalization at stake in the future of Central Banking interest rate hakes. Though many deny this reality because they state that the $560 trillion of interest rate risk is only a national amount, and not a “real” amount, I will follow up this article here on my substack platform with another one to explain, how in situations of default, notional amounts of derivative contracts come into play. In the next set of data that I’ve encapsulated with green and red rectangles in the above chart, we see the breakdown of these interest rate derivatives by fiat currencies. I’ve been tracking this data for many years, even prior to Covid lockdowns as my long-term followers know, and used this data to accurately predict in 2021, when many were saying Covid lockdowns would end worldwide, the extension of Covid lockdowns in Asia into this year and into 2023. My analysis of global interest rate derivative market positions over the last five years have also enabled me to conclude that most of these interest rate derivative contracts were/are betting on the continuance of low USD and Euro interest rates. As you can observe above, the greatest composition of the global interest rate derivatives market is in USD interest rate contracts that amount to $167.3 trillion (or $334.6 trillion if we negate the aforementioned halving accounting trick that took place more than a decade ago). While the ECB seems to be keeping their end of the bargain in not imploding this critical derivative market, US Central Bankers have not. If the Feds really go rogue in continuing to drive the USD strength against all other major global fiat currencies higher, not only will this possibly create...To finish reading the rest of this article,click hereand to subscribe to the skwealthacademy substack newsletter for new financial and investment analysis you will never find in the mass media, click here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)