Send this article to a friend:

October

24

2022

|

Send this article to a friend: October |

|

When the 60/40 Investing Strategy Doesn’t Work, Do THIS

A carefully designed retirement plan with the right amount of risk and strategic asset allocation is what we need. The problem is, that’s much easier said than done. Economic climates change, and what works well during the long bright summer of a stock bull market stumbles during the biting winter of a bear market. That means it’s also important to decide when to alter or shift strategies, and possibly reconsider retirement asset allocation. Is now could be one of those times? It certainly has been for an awful lot of people, especially those following the conventional investing wisdom… The most popular allocation strategy is withering on the vine One of the most popular asset allocation strategies that financial advisors have recommended for decades is called the “60/40.” According to Schroders, the overall definition and aim of this strategy is fairly straightforward:

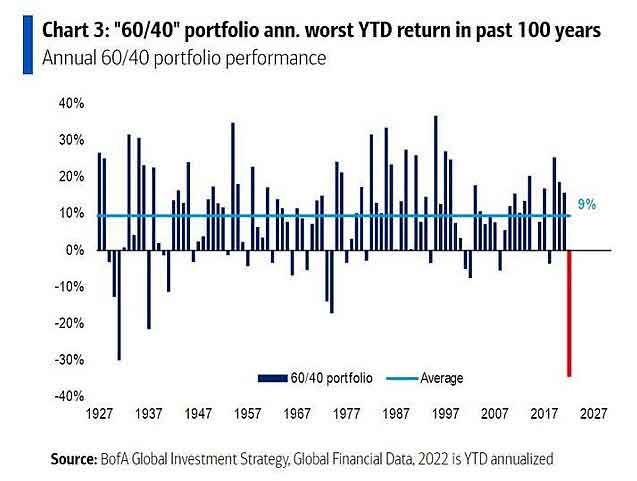

The theory is that a 60/40 portfolio should provide equity-like returns while smoothing out the extreme highs and lows (volatility) that come with an equity only portfolio. There’s another benefit to diversifying between different asset categories like this: stocks and bonds tend to be negatively correlated, which sounds bad but isn’t. It means their prices tend to move in opposite directions – which has the overall effect of lower volatility, smaller swings in price. Now, for decades, folks who weren’t sure how to save their money, who didn’t know a stock from a bond or an IRA from a 401(k), were recommended this simple no-brainer strategy. Stocks and bonds, combining high risk/reward and low risk/reward side by side was considered “bulletproof.” It’s easy to get the impression you could set up your portfolio, then forget it. Just keep contributing every month and, one day, retire to Fiji to work on your tan. Unfortunately, that isn’t the case. The latest research from Bank of America Global Investments shows how this strategy is performing right now:

Don’t rub your eyes – 2022 is actually a worse year for this “time-tested” investing strategy than 1929, with its Black Monday and Tuesday 23% two-day crash that inaugurated the Great Depression. Forbes recently described today’s dire picture:

If nothing else, I hope I’ve convinced you that naively following the 60/40 investing strategy may not be in your best interest. Its historically bad performance begs two questions: Do I give up on 60/40? What does work? Let’s see what professional financial advisors have to say… What some economic “experts” suggest You might be thinking, “If the 60/40 allocation is performing so badly, then redistributing that allocation over a different group of assets might be better.” We call that diversification. Generally speaking, diversification is a good thing. Here’s what the Securities and Exchange Commission (SEC) has to say:

The Nobel Prize-winning economist Harry Markowitz famously called diversification “the only free lunch in investing.” Okay, so diversification is good. The problem, according to the BofA report, is that you have to be considerate about how you diversify. Simply choosing more asset classes might not be enough:

Neither the 60/40 allocation strategy nor the 25/25/25/25 strategy is working very well right now. So some “experts” are providing simple, one-size-fits-all advice for Americans saving for retirement. One Blackrock advisor suggested “flipping” the 60/40 strategy around, lowering the amount of high risk stocks to 40% and putting 60% of your funds into bonds. Well, that’s one idea to consider – but it’s not really diversifying, is it? It’s more like shifting the deck chairs on the Titanic… Omar Aguilar, CEO and CIO at Schwab Asset Management suggested thinking long-term as he was talking to other advisors:

That seems like good common sense, especially his idea of rebalancing the risk in your portfolio. Let’s dig a little deeper… This decision fortified the 60/40 strategy during tough times Let’s take a look at one example of rebalancing risk by diversifying a standard 60/40 stock/bond allocation with physical gold. Now, all this has to be hypothetically speaking. We can’t buy past performance. If an American saving for retirement had started with $100,000 back in the year 2000, and allocated 15% of that fund to physical gold (the rest to stocks and bonds), here’s how it would have played out when compared to employing a 60/40 allocation by itself:

Once again, let me repeat, we can’t buy past performance. The best we can do is look to history and learn what we can to help us succeed in the present (and future). Having said that, an awful lot of people would be much happier today if they’d diversified their retirement savings with real, physical gold in a Precious Metals IRA. Based on recent research, Oxford Economics identified an “ideal” allocation to silver, as well:

Is diversifying with physical gold and silver right for you? Maybe so, if you’re interested in a safe haven investment in economically uncertain times. If you’re interested in the benefits of “The Magic of Diversification” and “the only free lunch in investing.” You can learn more about Gold IRAs here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)