Send this article to a friend:

September

19

2025

|

Send this article to a friend: September |

Gold's Surge Is an Economic Warning

Precious metals markets aren’t puzzling to well-informed investorsBrookings Institution's Robin Brooks is puzzled. Ever since Federal Reserve Chair Jerome Powell’s Jackson Hole speech, the one where he vaguely hinted at rate cuts, Brooks says financial markets have been “super weird.” Here’s what’s supposed to happen: Every asset that’s boosted by debt, from corporations to governments, should go up. Every intrinsically-valuable asset (commodities) should go up. Essentially, all risk-on assets from Brent crude to bitcoin are supposed to go up. Instead, Brooks notes:

In order to understand why Brooks is concerned, you have to understand why lower interest rates are good for procyclical assets. When the Fed lowers interest rates, essentially that is expected to lower the cost of borrowing throughout the economy. (The Fed doesn’t control this directly – really, all the Fed does is tell banks what APY they’re going to pay on reserve cash. When that number is low, reserve cash goes elsewhere.) So lower interest rates means more circulating cash, less saving and more lending. As you probably remember from the Great Financial Crisis, more lending leads to higher asset prices. Brooks is worried because the feedback loop between capital markets and the Federal Reserve seems to be breaking down. He’s right to be concerned! I’ve been pounding my keyboard about this for months now. Two things have changed:

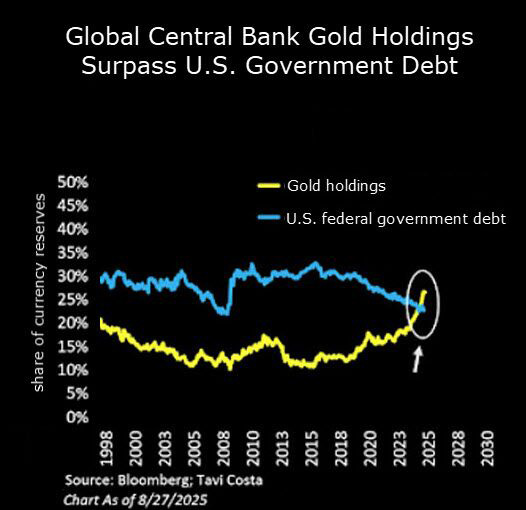

I’ve been telling you about record-shattering central bank gold buying since 2022. Global demand for gold, and lack of demand for our federal government’s debt, has hit a tipping point:

Original chart via Kitco Consider China. Officially, its central bank reports modest monthly purchases of one to ten tons. But according to World Gold Council strategist Joe Cavatoni, actual buying may be as much as ten times higher. Even at the low end, that puts China on track for an extra, unofficial 100-1,000 tons in its gold reserve every year. Whether you take the conservative or aggressive estimate, the signal is the same: nations are steadily moving reserves away from the dollarand into gold. The U.S. is struggling with weak demand for government debt. It’s not just the U.S. either – other G7 nations are facing difficulties in managing their debt burdens. Both France and the UK have experienced debt crises this year. We’ve talked about President Trump’s ongoing campaign to bully the Fed into lowering interest rates, too – bad news for the dollar. Which is bad news for everyone who owns dollars, saves or spends dollars, especially those of us who are paid in dollars. (Yes, me too.) The takeaway here is really nothing new. But I’ll let Brooks tell you in his own words:

It's probably time to get your hands on some real money, if you haven’t already. Whether you want to buy gold bullionor get in on the bargain that silver looks like today, we’re here to help. Speaking of silver, here’s why I think it could turn into the precious metals story of the decade… Silver vs. gold: Why the “outperformance” story falls apart According to a recent piece from Bitcoin Info News, a crypto-focused publication if you couldn’t tell from the title, silver has “outperformed” gold over the past year. On paper, sure – that’s factually true. But you and I know that numbers can be made to tell your preferred story. As someone who has followed precious metals for decades, I can tell you that framing doesn’t hold up under scrutiny. Here’s the context that’s missing from that story: Silver’s price history shows decades of stagnation compared to gold. In 1980, silver briefly hit $50 an ounce during the Hunt brothers’ infamous squeeze – that’s about $147/oz adjusting for inflation. Yet today, more than 40 years later, silver is trading around $40. Gold, meanwhile, was was about $600 in 1980. Today, it’s approaching $3,700. Does that sound like silver outperforming gold? The more accurate way to look at it is through the gold-to-silver ratio – a simple measure of how many ounces of silver equal one ounce of gold. Since the end of Bretton Woods, that ratio has averaged about 55:1. At today’s prices, the ratio sits above 85:1. By historical standards, silver is deeply undervalued. To simply revert to the long-term average, silver would need to rise to at least $66 an ounce at today’s gold price. On top of that, silver supply fundamentals tell a story the mainstream media prefers to ignore. The Silver Institute reported a 150-million-ounce supply deficit in 2024 – the fifth consecutive year of deficit. If we count the 2025 forecast, that’s a cumulative shortfall of 800 million ounces – coincidentally, almost exactly the quantity of silver bullion in London vaults. Even in a severe recession scenario, analysts expect the shortfall to remain around 50 million ounces this year. That’s not weakness – that’s structural scarcity. But it’s not reflected in today’s silver price – not yet. So when I see claims that silver is “outperforming” gold, I tend to think of them as misdirection rather than meaningful analysis. Silver has lagged badly for decades, and simple math says it has a lot of catching up to do. Today’s silver price simply doesn’t reflect reality.Accusations of price suppression abound. I’m not a conspiracy-theory guy by nature, but when I look at the numbers, it’s impossible to explain why silver is so grossly undervalued. Exactly why many seasoned analysts expect triple-digit silver in the next 1-2 years. Here's the takeaway: Don’t let headlines fool you. Don’t trust a simple story because it’s simple. Remember, gold remains the world’s ultimate safe haven asset. Silver is both similar and different – a hybrid commodity, an irreplaceable industrial input that’s also a widely respected tangible asset. The “poor man’s gold.” I believe silver’s price is poised to play catch-up to the price of gold in ways that will startle even long-time investors and analysts alike.

|

Send this article to a friend:

|

|

|

The Brookings Institute calls gold’s rise “weird” – but it isn’t. Nations are dumping dollars, debt demand is down and silver faces historic scarcity. The message is clear: Government promises have fallen out of favor, and here’s what’s replacing them…

The Brookings Institute calls gold’s rise “weird” – but it isn’t. Nations are dumping dollars, debt demand is down and silver faces historic scarcity. The message is clear: Government promises have fallen out of favor, and here’s what’s replacing them…