Send this article to a friend:

September

14

2024

|

Send this article to a friend: September |

|

A Plague On Both Your Monetary Houses

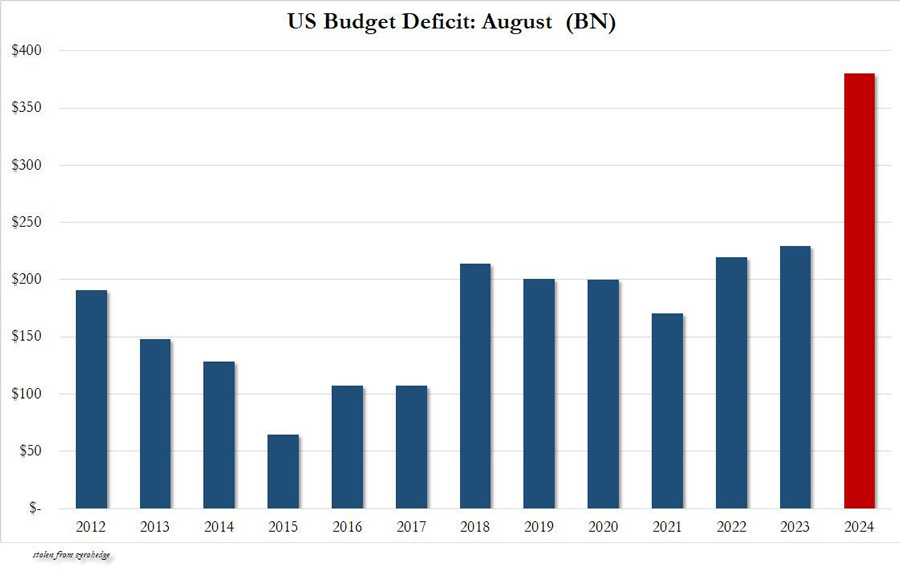

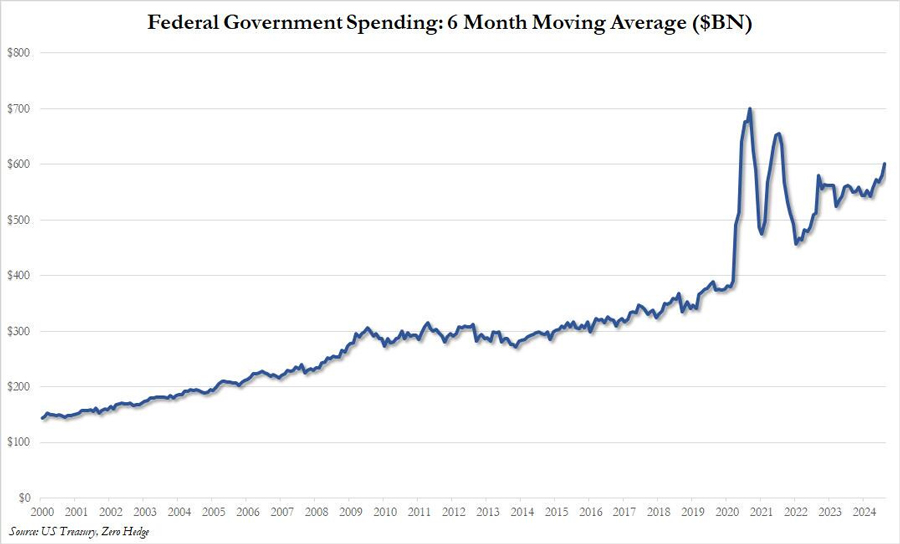

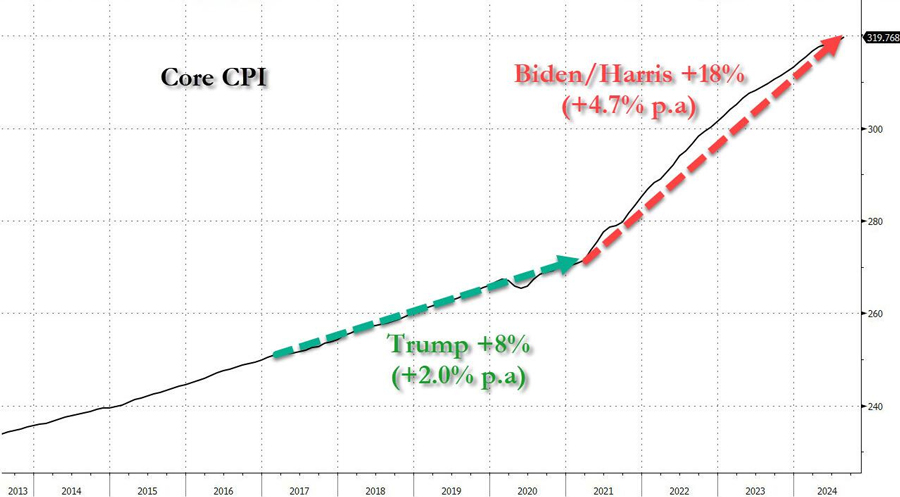

For all the huffing and puffing I do about politics, you’d think that both candidates would have substantially different ideas for monetary policy, should they be elected. After all, this is supposed to be a finance blog. But the truth is, they don’t. While I do think the Republican Party is more inclined to decrease the size of government and cut some spending—both things that we desperately need to do in order to fight inflation and streamline our economy—President Trump has also promised to cut interest rates when he’s in office, a move that would normally add fuel to an inflation fire that the Fed has not yet put out. Despite my whining, it’s a certainty that the national debt is going to go up, no matter who is elected president. With President Kamala Harris, it likely rises much quicker, and spending spirals even further out of control than it has been under the Biden administration (for a primer on just how screwed our nation’s finances are, listen to this podcast and then read this Zero Hedge article).

Chart: Zero Hedge With President Trump, at least there would likely be some deregulation, lower taxes, and modest spending cuts that could slow our descent into monetary and fiscal Armageddon.

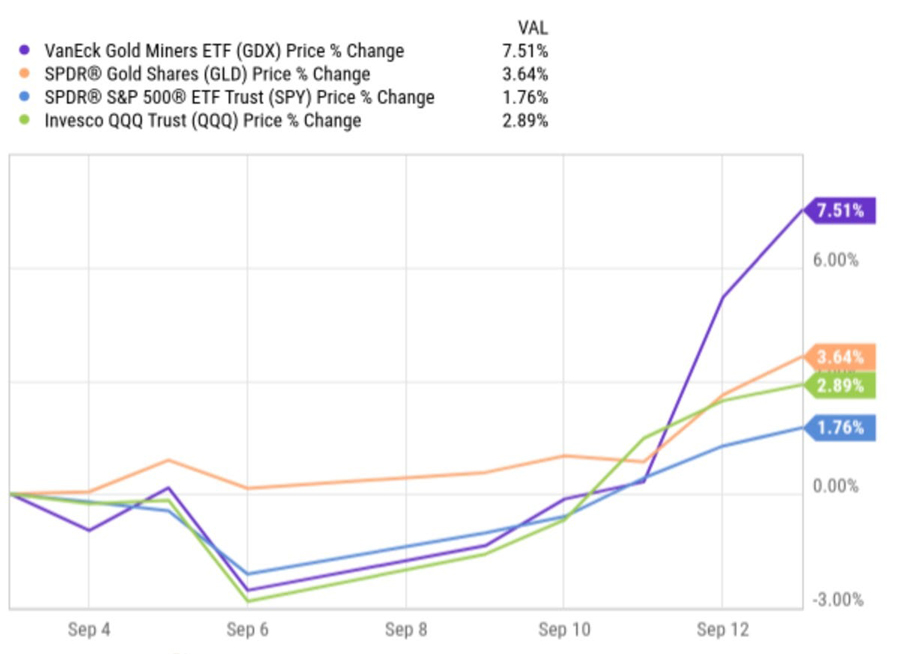

Chart: Zero Hedge This morning I find myself looking back at the week, trying to make sense of the stock market moves over the last 3 sessions. With the NASDAQ at about 37x earnings and interest rates at 5.5%, combined with both CPI and PPI numbers that came in hot this week and the fact that we just made a massive negative revision to the country’s labor statistics, you don’t necessarily expect the stock market to be raging higher. But the things that are supposed to happen with 5.5% interest rates after the largest debt bubble in history—namely, an increase in savings, less discretionary spending, lower financial asset prices, and a slowing economy—haven’t happened yet. I believe this simply means that the Fed’s fight against inflation hasn’t been won and very likely isn’t over, despite people claiming victory and a ‘soft landing’. Whoever comes into office next is going to be taking charge in the unique position of overseeing a Federal Reserve cutting interest rates with asset prices and the stock market at all-time highs, with inflation still well above the Fed’s 2% target. In essence, the Fed was trying to put out a house fire over the last two years, had finally contained it to just one or two rooms in the house, and before putting it out, is getting ready to switch the fire hose they’re spraying from water to gasoline. Both parties should really be ashamed of themselves for the way they approach monetary policy, but especially Republicans. If there’s one party that you could expect to embrace an Austrian economic mindset, it would be the GOP. After all, Democrats are the party of Stephanie Kelton and Paul Krugman. They are so far gone off of the economic fundamental reservation, there’s really no hope for them ever coming to their senses about fiscal or monetary responsibility. The GOP you could at least reasonably hold out some hope for. The stock market over the last few days looks to me like a market that has just thrown its hands up in the air and said “fuck it, we’re going the hyper-inflationary route”.

While I’m bracing for the inevitable outcome of inflation rising once again and financial assets rising with it, the fact that gold has risen through all-time highs with authority before the Fed has even started cutting, and in tandem with the stock market, leads me to believe that the market is ascribing this week’s froth to more money printing and inflation. The trading this week, with stocks as overpriced as they are, seems to me like a market that has quit on the idea of economic fundamentals and is rolling out the red carpet for years of Modern Monetary Theory to come.

The upshot is that no matter who wins the election in November, they’re very likely going to have to deal with a massive recession and deflation in financial assets until the Fed decides to rush to the rescue with QE again. I still predict a crash before the QE spigot opens back up and, when that happens this time, there will be no doubt as to the path the country has taken with modern monetary theory. As I’ve said numerous times on this blog, there is no turning back from the monetary policy path that we are on because politicians and bureaucrats are too cowardly to let assets crash and a real correction take place. So I keep trying to remind myself that if my candidate doesn’t win in November, his opponent is likely going to be facing a financial crisis and monetary crisis the likes of which the country has never seen. Sure, a President Kamala Harris would be completely and totally unprepared for such a catastrophe, and would be advised by people like Biden’s useless economic advisor Jared Bernstein, who has no idea how quantitative easing works despite being in charge of economic decisions. I guess the silver lining is we’d all be able to point our fingers and say, “Ha! I told you so” to the candidate we loathe, instead of the one we voted for. Peter Schiff has joked that gold could be $10,000 an ounce before the end of Kamala Harris’s presidency—a prognostication he walked back a little bit in a recent Kitco interview that’s well worth watching. But I don’t think he could be that wrong. As gold investors and gold owners, what do we care if Kamala Harris presses the accelerator down to the floor and starts racking up another trillion dollars in debt every month? Isn’t that the point of investing in sound money assets? Conversely, if Donald Trump wins the election, he’s going to have to face similar discomfort, fiscally and monetarily. Trump has access to advisors with Austrian thinking, but his ego is not going to let him admit defeat or make monetary and fiscal policy decisions that would make things worse for the short term, even if they make things better in the longer term. Under his presidency, we’d likely have a similar scenario, just with more cutting and reduced spending. And with a monetary policy plague cast over both political houses, I guess that’s the best we can hope for — a hail mary prayer for just slight spending cuts and lower taxes. But just remember, no matter who you’re voting for or who you want to see win, the celebration as it relates to “fixing” our economy or “solving” inflation could wind up being very short-lived. QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important. Subscribe to QTR’s Fringe FinanceBy Quoth the Raven · Thousands of paid subscribers Liberty. Finance. Bullshit. . . .

|

Send this article to a friend:

|

|

|