Send this article to a friend:

September

22

2023

|

Send this article to a friend: September |

|

5 Ways the Fed Just Made Americans Poorer

After that meeting, Federal Reserve Chairman Jerome Powell announced that the Fed would (at least momentarily) pause their recent string of interest rate hikes. This decision surprised almost no one. An article on CNBC summarized the situation:

The Fed’s latest “dot plot” indicates one further interest rate hike before the end of the year. Should that actually happen, we could see another 0.25% increase in rates before the end of the year. The decision to leave rates unchanged right now obviously has consequences. Today, we’ll explore exactly what this decision means for you… What this pause in interest rate hikes doesn’t mean Metaphorically speaking, a pause in interest rate hikes is like setting cruise control on the highway. It’s intended to keep the car zipping along at a consistent speed. Unfortunately, that “consistent speed” means inflation is unlikely to subside. The most recent inflation reports put the Fed’s preferred measure, core personal consumption expenditures(core PCE), at 4.2%. up from June. That’s both more than twice their target, and going in the wrong direction. Core PCE ignores both food and energy, which, admittedly, are more volatile than other prices. On the other hand, these categories are significant expenses:

It’s arguably a mistake to focus on an inflation measure that ignores these costs, all of which are necessities. Rising prices on food, gas and energy tend to hit lower-income households harder. These expenses are what economists call “inelastic,” meaning demand stays fairly consistent regardless of price. It’s not like people stop eating when food prices rise, then eat twice as much when food prices fall. If we turn our attention to a broader inflation measurement, headline CPI, we see it’is on the rise again at 3.7% for August. We’ve seen it pulled down by a drop in energy prices, but that’s now abating. And recent rises in oil prices will keep headline inflation high. The Fed’s set the cruise control, at least for now. That means we can expect prices to continue rising at their current pace. Mission accomplished? Clearly not. Here’s how interest rate hikes work We all know the basics of how interest rates work, and how they affect our decisions. Here’s a brief explanation of how economists think of interest rates. Interest rates represent the cost of credit (borrowing money). When interest rates are higher:

When interest rates are lower:

Generally, higher interest rates reduce economic activity, which can lead to a recession. Lower interest rates increase economic activity, incentivize spending and can lead to speculative bubbles. Forgive me if you already know all this – remember, rates are higher today than they’ve been in 22 years. A lot of American households and businesses either never learned or have forgotten how above-zero interest rates change their everyday economic reality. Let’s move on to specifics… Five specific economic consequences Here’s how the pause in rate hikes will cost us: #1 – Higher credit card interest rates (20%+) stick around Even if you have good credit, you’re probably paying a whole lot more interest on any credit card balances. Maybe more than you can ever remember paying before. Today, the average rate sits at 24.45%. In January 2022, the average credit card interest rate was “only” 16.3%. In the last 21 months, credit card rates have risen 50%. If you’re carrying any credit card debt, it’s smart to prioritize paying it off. Lower-income households, who’ve been relying on credit cards to make ends meet, are in trouble. This recent poll confirms it:

Credit card delinquencies are currently at a 10-year high. Remember, higher interest rates make all borrowing more expensive… #2 – Mortgage rates well above 7% slow the housing market Already-high mortgage rates will stay higher for longer. The New York Times encapsulated what this could mean for you:

Homes cost more than they did at the peak of the 2006 housing bubble. The combination of higher home prices and steeper mortgage rates has made home affordability the worst in the nation since 1984. Black Knight, a mortgage technology and data provider, calculates that monthly mortgage payments for new homebuyers have risen 92% in the last two years. Andy Walden, vice president of enterprise research and strategy at Black Knight, added some context:

Which is more likely – a 28% drop in home prices, or 60% growth in income? The housing market looks grim. Time to reconsider #vanlife? Not so fast… #3 – Car loans head for 7% (at least, it could be much worse now)

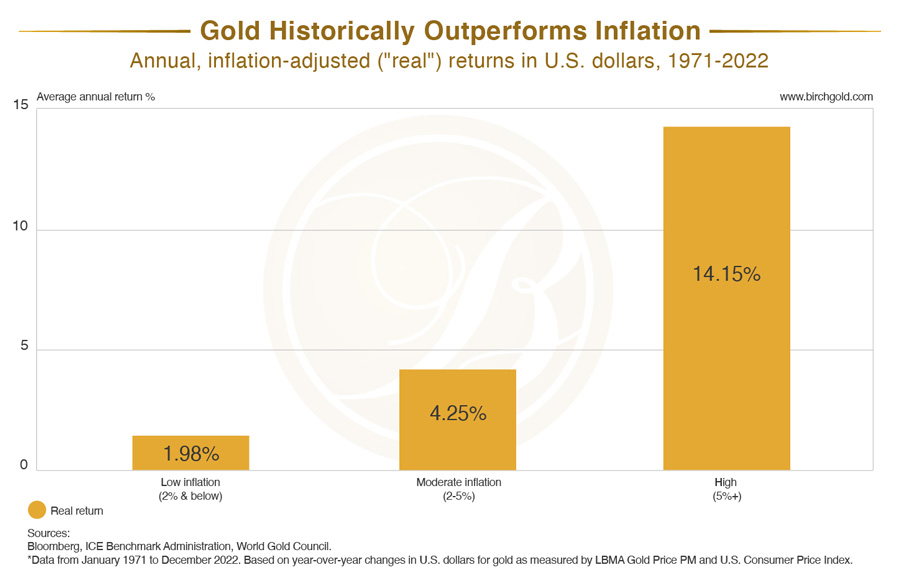

Loans, too, as this U.S. News article states the average auto loan interest rate as of August. According to that piece, if you have excellent credit (FICO score 750 or higher), you might secure an interest rate of 12.87% – 13.12% for a new or used car loan. If your credit isn’t excellent, expect higher (and much more expensive) rates. Both new and used cars are far more expensive. No wonder the average car on the road is a record 12.5 years old… #4 – Savings account interest rates are finally going up! Bank savings account rates are heading north of 5%, which appears like welcome news for people who might be looking for a safe place to tuck their money. Especially when you consider that those accounts were only paying 0.25% or less just a few years ago. But like we covered in a recent article, thanks to persistent inflation, you aren’t likely to benefit from that increase (it’s more of a mirage). #5 – Don’t expect prices to fall anytime soon Regardless of your financial situation, the pause in interest rate hikes means inflation is likely to stick around. At least until the combination of prices on essentials and higher borrowing costs finally crush demand, and cause a recession. But the good news is, you still have one way to potentially hedge against this rather persistent (and frustrating) trend… Since 1971, when the market was first allowed to set its price, physical gold handily outperformed inflation.

Note these are after-inflation returns – still positive when inflation is low, much higher when inflation burned hot. There’s no guarantee next time won’t be different, but in the absence of a crystal ball, historical performance is our next-best benchmark. (Our education page has the full scoop.) Along with other inflation resistant investments, diversifying your savings with physical precious metals like gold and silver could help preserve your retirement savings, maintain your buying power, and offer you a firm foundation for your financial future. We’ve even developed a free kit packed with information that explains why this is the case. While you’re at it, you can also visit our other education pages so you can make an informed decision.

|

Send this article to a friend:

|

|

|

The FOMC met Wednesday and Thursday.

The FOMC met Wednesday and Thursday.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)

{kind=link}