Send this article to a friend:

July

31

2023

|

Send this article to a friend: July |

|

Inflation will return

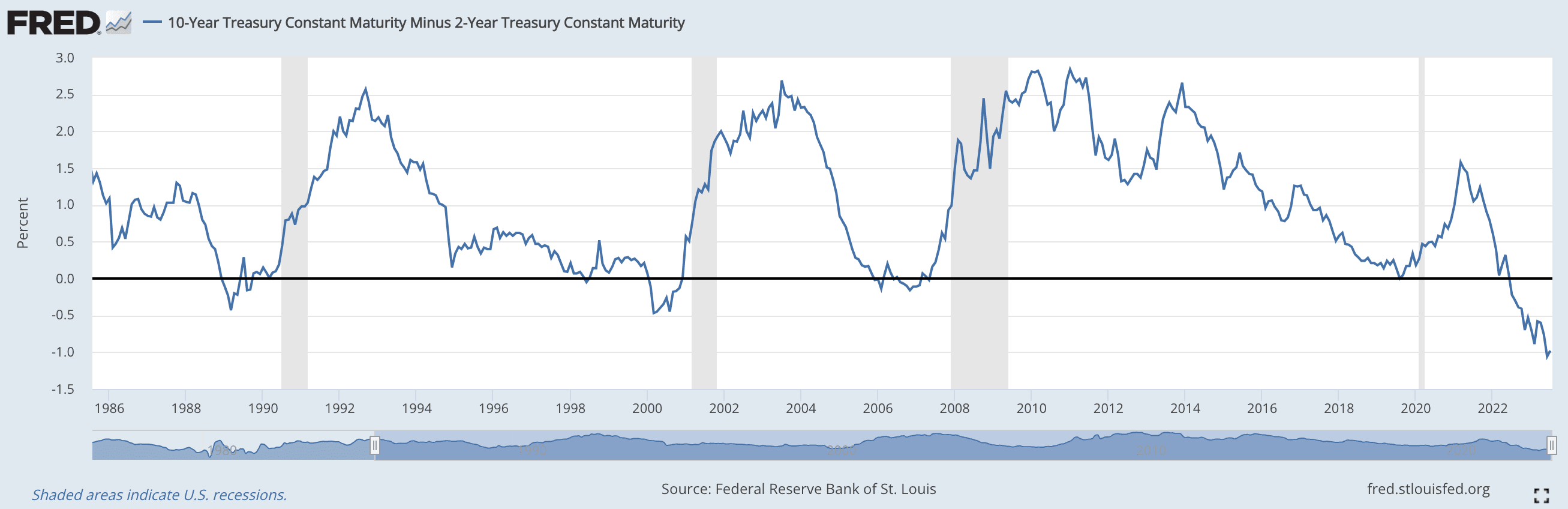

The misunderstanding is to assume that the widely expected recession will lead to further falls in consumer price inflation, and that therefore interest rates and bond yields will decline. These hopes are based on Keynes’s rejection of Say’s law, which simply points out there is no such thing as Keynes’s general glut because the unemployed stop producing. A further point is that banks are increasingly scared of lending risk, which is leading to a credit squeeze. This raises the question, as to how can interest rates fall when there is a growing shortage of credit? The current economic setup for the US, the Eurozone, and the UK seems set to increase central bank credit replacing commercial bank lending, which will undermine their currencies. Additionally, government funding requirements will increase materially at a time when cross-border investment flows are threatened by financial bear markets. The timing of a new BRICS gold-backed settlement currency and China’s determination to consolidate the BRICS and Shanghai Cooperation Organisation’s sphere of influence have the potential to offer alternatives for capital flows escaping from the collapsing finances of the western alliance led by America. Above all, we are witnessing the death of fiat, because it is increasingly difficult to see how the current currency regime based on the dollar will survive. Market misconceptions Equities and bonds are priced in the expectation that consumer price inflation will subside and that interest rates will start falling in the not too distant future. This is the underlying reason behind a negative yield curve, with 10-year bond yields yielding significantly less than 2-year maturities. And the chart below shows that this disparity is the highest it has been since the 1980s.

A negative yield curve is also associated with a recession to follow, and the chart confirms that negative yield curves are indeed followed by recessions. But the rate of price inflation will have to remain subdued, because expectations of low long-term rates must be confirmed by events. Indeed, the apparent success of monetary policy over the period covered by the chart without leading to persistent inflation has contributed to the widespread belief that official monetary policies work. But is the wager in financial markets correct, that this credit cycle will conform with those of the last forty years and that a negative yield curve tells us that with consumer demand dropping, price inflation will subside, and short-term interest rates fall? This is the essence of the belief that bond yields along the yield curve will normalise with lower yields at the front end and that the bull market in equities will remain intact. Sticking with the chart for the moment, you will notice that at minus 1% the negative yield on the curve far exceeds that of previous occasions, which surely must raise concerns that for once the past is not a guide to the future. Perhaps the forecast recession will be considerably worse than anything in living memory. Perhaps the long end of the yield curve is badly mispriced, being far too low. If the latter is the case, as this article will argue, the outlook for financial asset values is extremely poor. Illustrated below, charts of the yields on 10-year bonds around the world give little comfort.

Any technical analyst would describe these charts as being in strong bull markets, merely consolidating before going higher. In the cases of Germany and the UK, the shape of the consolidation is immensely bullish. We are, of course, discussing bond yields, which means bond prices are set for further substantial falls. And if bond prices fall, equity values will fall as well. Based on the experience of the last forty years, this is the opposite of what is priced into financial markets. That a recession will follow seems assured. The bank credit cycle is seeing to that, with money supply not growing or even contracting alarmingly in some jurisdictions. And the neo-Keynesians who make up the bulk of the establishment and investing communities believe recessions are caused by falling demand leading to a glut of unsold products. Therefore, they believe that a recession will always knock inflation on the head. And being forward looking, markets can be expected to discount falling inflation in the expectation of recession. So much for Keynesian expectations. Keynesians were confused by events in the 1970s, when recession was accompanied by inflation. They had difficulty explaining this phenomenon, believing that inflation of prices was only the result of overstimulation of an economy. They had discarded Say’s law, which pointed out there could be no such thing as a general glut because production output declined with employment. They also airbrushed the conditions of every great fiat currency inflation out of their minds, ignoring the fact that if the GDP statistic had been invented earlier, Germany’s nominal GDP would have risen off the charts in 1918‑1923. And that the lagging inflation deflator would have even shown the economy to be remarkably healthy in real terms through the whole episode of the paper mark’s collapse, which for other than exporters being paid in hard currency impoverished the vast majority of the population. An additional problem is in the monetarists’ approach, which rarely, if ever, distinguished properly between credit and money. Admittedly, the early warnings of a downturn in economies came from monetarists who pointed to the slowdown of monetary growth in the broad money statistics. They were correct in assuming a correlation between GDP and growth in broad money. But they fell into the trap of believing that the authorities should manage economic policy in the light of changes in the quantity of money. In other words, they have become statists themselves, turning their backs on the ability of free markets to set demand for credit. Doubtless, today’s monetarists would claim they are merely being practical in the context of the current system, but they cannot have it both ways. In any event, their claims over the relationship between the money supply and prices only hold water in a limited context, as the following conundrum illustrates. Let us assume that Nation A has an economy of a certain size, measured by output volumes instead of GDP credit totals. Let us also assume that Nation B, using the same currency units and with the same quantity of human resources has an economy twice the size in terms of volume outputs. What will be the difference in the purchasing power of their common currency units? The first thing to note is that other things being equal, there will be substantial expansion of credit to finance the extra production. In other words, on the same population base, money supply could be approximately twice as high in Nation B compared with Nation A. But this does not mean that prices will be higher in Nation B. It is more likely they will be lower in Nation B than in NationAbecause of higher output volumes benefitting from economies of scale, investment in more efficient production, and enhanced competition. From this we can deduce a simple rule governing the monetary relationship. So long as expanded credit is provided for the enhancement of commerce it will not result in price inflation. If, in the example above, Nations A and B were simply the same nation under different conditions, doubling the quantity of credit would not result in similar increases in prices. And the purchasing power of a circulating medium is determined by markets, not its quantity. There is a further distinction to be made, in this case between credit backed by sound money, which is gold, and credit backed by fiat currency. Sound money is the universally accepted money without counterparty risk, which both legally and derived from long-standing human acceptance is gold. In an earlier article[i], I showed that the expansion of bank credit (which makes up over 90% of the circulating medium) can have a short-term cyclical effect, while the more permanent destruction to its purchasing power comes from the state increasing the quantity of bank notes and commercial bank deposits on its central bank’s balance sheet. The example where the expansion of central bank credit is strictly controlled, while commercial bank deposits are determined by market factors is illustrated in the following chart of Britain under its gold standard for over nine decades, taken from the article referred to above:

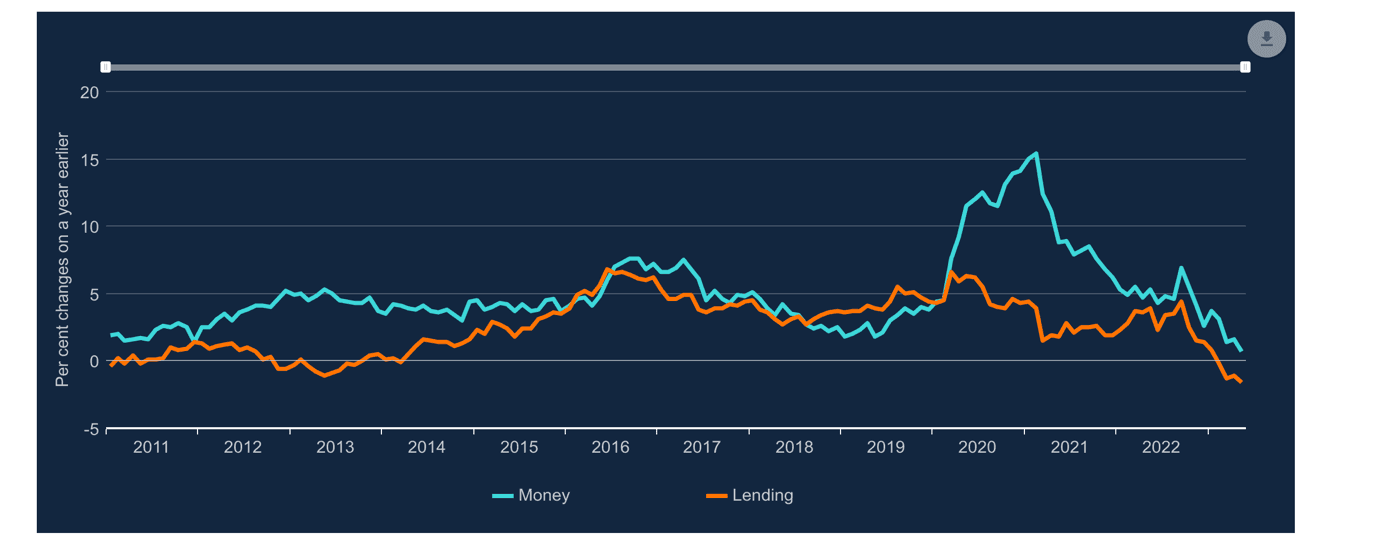

We can see from the first chart how under Britain’s gold coin exchange standard, the note issue was stable while commercial bank credit expanded. The crises of 1847, 1857, and 1866 which led to temporary suspensions of the Bank Charter Act of 1844 are notably reflected in wholesale price fluctuations in the lower chart, but the self-correcting nature of disruption to the general price level usually applies with there being almost no net change in the two price indices over sixty years. The disruptions to prices from the bank credit cycle diminished over time. Undoubtedly, much of this was due to improvements in the banking system. But there is another factor at play: over time, public confidence grew in the government’s commitment to maintaining the gold standard, so cyclical variations in the purchasing power of the currency diminished. In other words, instead of the quantity theory of money determining the relationship between changes in the quantity of currency and prices, it is its users who have the final say. In a gold-backed credit system, saving is a more attractive proposition. While bank credit expanded over the century, so did savings. According to the Bank of England’s statistical research, in 1830 savings represented 5.3% of GDP. By 1844, at the time of the Bank Charter Act it had risen to 14%. And by 1890, it hit a high of 22.5%. The proportions between current consumption and consumption deferred, which are savings, has a regulating influence on the general level of prices. Under a fiat currency regime, with respect to savings the same is true today as it was under Britain’s gold standard. In Japan and China, there is a high propensity to save. This means that the expansion of bank credit only partly fuels consumer demand. And the element which consumers save supports investment in production, which tends to reduce prices, thereby offsetting pressures for consumer prices to rise due to higher consumer spending. The point behind fiat currency, which has ruled us for the last 53 years, is that it gives governments an extra source of finance by inflating its quantity. In this it is fundamentally different from the sound money example which imposes a strict monetary discipline. And governments which have discouraged savings both by taxing them and by encouraging consumer spending have simply added to the tendency for consumer prices to rise and undermine the currency. Credit theory therefore attributes persistent non-cyclical inflation to the expansion of central bank currency and its credit, and both are associated with excessive government spending leading to budget deficits. For most advanced economies, a global slump leads to lower tax revenues and higher welfare costs. Consequently, budget deficits soar, undermining their currencies. And a currency undermined is reflected in higher consumer prices. The current lull in CPI inflation is merely temporary. Interest rate management by the state fails Markets are in thrall with central bank monetary policies, which centre on interest rate management. And despite the recent failure of these policies, economists and investors still believe that central bankers know best, and with a misreading of the great depression in mind, that their control is preferable to rates set by free markets. But there is no clearer example of policy failure than that which is exposed by current events. The suppression of interest rates to zero and below has contributed in no small measure to the mess central banks find themselves in today. Even so, critics blame the incompetence of individual central bank leaderships without appreciating the impossibility of official interest rate management to improve economic outcomes compared with leaving it to free markets. The groupthinking that pervades in central banking circles denies any radical reassessment of the relationship between interest rates and prices. The idea that interest rates reflect time preference, counterparty risk, and a market-based assessment of change in purchasing power of the currency is not even considered, presumably because an understanding of these factors would rule out the prospects of any official role in setting interest rates. And for the largest stock market priced in the world’s reserve currency, ignoring the true relationship between the dollar’s prospective purchasing power and interest rates is leading it towards disaster. Foreigners, who at the margin determine the dollar’s purchasing power are the first to turn sellers. They over-own dollars and dollar assets to the tune of $32 trillion, well in excess of US GDP. Not only are there moves afoot in an expanded BRICS to reduce dependence on the dollar, making its ownership less relevant for the nations involved, but if expectations of falling interest rates turn out to be incorrect, there is bound to be substantial foreign liquidation of US financial assets as losses mount on portfolios. Furthermore, it seems that with $6 trillion of the $32 trillion total sitting in bank deposits it is likely that a bear market driven by the receding prospects of falling interest rates, and the prospect of commercial bank credit contracting as well, will undermine the dollar’s exchange rate. Bank credit is contracting Bank credit in the US has begun to contract as the FRED chart below shows.

Bearing in mind that the interest cost has increased for borrowers, they are facing mounting liquidity problems particularly for those whose sales growth is stagnating. A combination of higher input costs, persistent supply chain issues, and higher borrowing costs are set to worsen the outlook for bank credit expansion even more, with bankers becoming increasingly concerned over their risk exposure. The situation in the Eurozone is worse, as the next screenshot from a ZeroHedge article this week demonstrates.

In its bank lending survey, the ECB admitted that “The cumulated net tightening since the beginning of 2022 has been substantial, and the bank lending survey results have provided early indications about the significant weakening in lending dynamics observed since last autumn.[ii]” However, by attributing the decline in bank lending to falling demand for loans is a common error of interpretation. At a time of economic stagnation — the current situation in Germany particularly refers — businesses do not stop borrowing. Instead, their demand for credit increases. The correct interpretation is that banks are withdrawing their supply of credit, with entirely different connotations. But then an official understanding of the cycle of bank credit was always wanting. The situation in the UK is similarly alarming, as the Bank of England’s chart below shows.

In the US, Eurozone, and UK, high levels of bank balance sheet leverage and a deteriorating economic and financial outlook seem assured to lead to further contraction of bank credit. But these are also the conditions which lead to increasing credit demand to offset cash flow difficulties for borrowers. Inevitably, interest rates will rise for the minority of businesses that can present exceptionally good cases to their banks for extending credit facilities. Otherwise, they must seek funding from other sources, such as private equity houses, selling assets, or downsizing to reduce costs. Over the rest of this year, we will see businesses that fail to convince their banks to extend loan facilities begin to go to the wall. Furthermore, the implications for employment, tax revenues, and welfare commitments will increase government budget deficits above current expectations. And funding these increasing budget deficits will require credit expansion by the central banks, offsetting the credit contraction of the commercial banks. Commercial bank credit, which imparts value to both loans and deposits, with a small theoretical discount for counterparty risk is firmly tied to the value of central bank credit, evidenced in bank notes and commercial bank reserves on the central bank’s balance sheet. The difference between these two forms of bank credit is that other than cyclical variations, changes in purchasing power come entirely from central bank credit. Inevitably, if central banks are forced into expanding the quantity of their credit for whatever reason, then they will almost certainly undermine the purchasing power of their currencies. Foreign valuations of currencies In maintaining the purchasing power of the dollar, the US authorities appear to have an insuperable problem. The prospects for the economy are worsening because of the outlook for bank credit. The budget deficit is likely to increase significantly above official expectations. And with the misunderstanding of what interest rates actually represent, being the expected future value of the currency by those who presently hold it, the inflationary implications of funding the US Government’s deficit will require foreign holders not to liquidate their exposure. For foreigners selling dollars, the alternatives of the euro, yen, or sterling appear equally unattractive, their only positive being that the dollar is over-owned by foreigners, but the others are not. The euro has the additional problem that the entire system of the ECB and its national central bank shareholders are technically bankrupt due to hidden losses on the bonds carried on their balance sheets. And recapitalising the entire system at a time of a gathering bank credit crisis due to contracting credit leading to higher interest rates is virtually impossible. Sterling can be likened to a poor man’s dollar, with a lack of savings and budget deficits similarly set to expand due to the impending recession. And the yen only offers negative interest rates, plus a central bank that also needs recapitalising. There are two alternative homes for foreign capital flows leaving these currencies. The obvious one is physical gold as an escape from increasingly risky credit tied to fiat currency. But perhaps that argument will have greater force when the new BRICS trade settlement currency being backed by gold is confirmed in the upcoming summit in Johannesburg. The less obvious option is to buy into China’s renminbi. The case for the renminbi is that China has substantial investment plans in Asia, Africa, and Latin America. In partnership with Russia, the two hegemons are determined to protect themselves and their interests from US disruption. Not to put too fine a point on it, this is a battle which the US may have already lost. We will know more following the BRICS summit, but with the priority being to neutralise the weaponised fiat dollar, China and Russia are likely to consolidate their position as ringmasters for an enlarged group of nations. That being the case, while the economies of the western alliance which owes its allegiance to America are sinking into oblivion, the prospects for the combined BRICS+ and Shanghai Cooperation Organisation are improving. Unlike the time when President Trump managed to disrupt inward investment flows through the Shanghai-Hong Kong Connect, this time President Biden can only ban US funds from investing in China. In anticipation of demand for inward investment, China expanded the scheme in December last year to widen the range of equities available on the Shanghai Stock Exchange. Doubtless, there will be further tweaks to this facility. The consequences for gold A resurgence of consumer price inflation during a recession has not happened for a considerable time. It is during recessions that government deficits rise. This time, the US Government’s starting point is deficits of over £1.5 trillion. And as demonstrated in this article, it is the expansion of central bank credit, not commercial bank credit, which undermines currency values on a non-cyclical basis. At a minimum, the stagflationary conditions of the 1970s appear to be returning, which drove the gold price to rise from $35 to $850 in less than ten years, even though the Fed Funds rate rose from 5% to a peak 19%. The problems for the dollar are shared by others, notably sterling and the euro. But the dollar is also over-owned by foreigners and almost certainly will be dumped by them, in some cases for gold. There could be an additional problem for the dollar arising from a new gold-backed trade settlement currency, mooted to be discussed at the BRICS summit in August. While there are some signs that it will not be universally popular with the attendees, it is notable that Sergei Lavrov, Russia’s Foreign Minister is on record as stating that Russia has accumulated billions of useless Indian rupees as payment for oil sales. The tolerance of Russia, Saudi Arabia, Iran, and other net exporters for payment in illiquid minor currencies is strictly limited, so payment changes in a more secure currency are bound to be forced through. Consequently, dollar reserves at central banks representing over forty nations will be exchanged for gold — a trend which has already been evident for the last eighteen months. The gold price is therefore likely to rise materially due to economic factors set to destabilise the economies of America and her western allies. And foreign influences will shift capital away from them into gold, commodities perhaps, and the investment opportunities offered by the two Asian hegemons. Assuming the new gold backed trade currency is introduced, it seems bound to accelerate a move by Russia and China towards backing their own currencies with gold. Others are bound to follow. Only then will the full benefit of a widespread industrial revolution for most emerging economies be available to them. But the fiat system based on the dollar will be destroyed. [i] See https://www.goldmoney.com/research/the-real-determinants-of-currency-value [ii] See https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/pdf/ecb.blssurvey2023q2~6d340c8db6.en.pdf

|

Send this article to a friend:

|

|

|

It is an error to expect inflation to continue to fall in America. All financial market values in the US and elsewhere are predicated on this hope.

It is an error to expect inflation to continue to fall in America. All financial market values in the US and elsewhere are predicated on this hope.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)