Send this article to a friend:

July

13

2021

|

Send this article to a friend: July |

|

Consumers Expect Red-Hot Inflation to Crush Their Earnings: Fed’s Survey

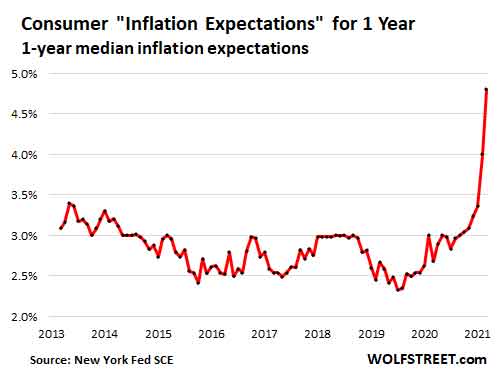

When the Fed discusses inflation, and the extent to which it would be allowed to exist, it always mentions “inflation expectations” and that they are and should be “well anchored” because persistent consumer price inflation is in part a psychological phenomenon, where consumers are willing to pay higher prices because they expect higher prices. Companies are getting away with charging higher prices, and because they expect to charge higher prices, they’re raising their wages, but not as much as they raise prices. These inflation expectations contribute to a cascade of higher prices leading to higher prices. And consumers’ inflation expectations are now blowing out. The inflation expectations for one year from now jumped to 4.8% in June, the highest in the survey going back to June 2013, according to the New York Fed’s Survey of Consumer Expectations today.

The under-40 crowd expects inflation to hit 3.8% a year from now. The 40-60-year-olds expect inflation of 4.7%. The over-60 crowd expects inflation to hit 5.7%. It’s that over-60 crowd that experienced as adults the high-inflation era of the 1970s and early 1980s. The younger ones have only heard about it. These inflation expectations tracked by the New York Fed roughly match the inflation expectations tracked by the University of Michigan’s Survey of Consumers, whose latest reading jumped to 4.6%. The inflation expectation whoppers. According to the New York Fed’s survey, consumers expect to face these price increases over the next 12 months.

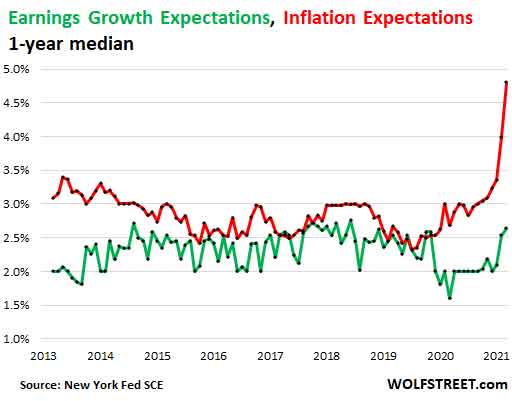

Adding up housing costs, food, gasoline, and healthcare, which for many consumers make up nearly all of their spending and which are expected to rise between 6.2% and 9.7%, it’s hard to come up with an overall inflation expectations figure of only 4.8%. But OK, we’ll cut our consumers some slack here. Consumers expect inflation to outrun their earnings. Consumers expect their earnings to grow by only 2.6%, and their total household income by 3.0% over the next 12 months, even as they expect prices overall to increase by 4.8%. This chart shows to what extent one-year inflation expectations (red) are outrunning one-year earnings growth expectations (green). If this continues to play out like this, it’s going to get tough for these consumers:

Three-year expectations have jumped, but not as much. For now, the widely hyped messages from the Fed and the government, echoed by the major news outlets, that this bout of inflation is just “temporary” or “transitory” are resonating with consumers to some extent. Inflation expectations for three years from now have jumped, but not as high, reaching nearly 3.57% in May and 3.55% in June. The green line reflects inflation expectations over the next three years, against the inflation expectations over the next 12 months (red line):

It’s these longer-term inflation expectations that the Fed is now hanging its hat on, including in the minutes from its last FOMC meeting. But the Committee is split. On one side, “a number of participants noted that, despite increases earlier this year, measures of longer-term inflation expectations had remained in ranges that were broadly consistent with the Committee’s longer-run inflation goal.” On the other side, “several participants expressed concern that longer-term inflation expectations might rise to inappropriate levels if elevated inflation readings persisted.” All of them are behind the curve already. The FOMC meeting minutes also spell out the Fed’s goals: “to achieve inflation that averages 2 percent over time (per core PCE now = 3.6%) and longer-term inflation expectations that are well anchored at 2 percent (now = 3.5%).” Inflation expectations are among the factors that build persistent inflation. Spikes in commodities and other goods, due to unique circumstances, fire up temporary inflation. But enough of those spikes and enough of that temporary inflation trigger rises in inflation expectations as the whole inflationary mindset changes, and the cascade of higher prices leading to higher prices begins. Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)