Send this article to a friend:

June

01

2024

|

Send this article to a friend: June |

|

Interest Rates: What Are They and What Do They Actually Do?

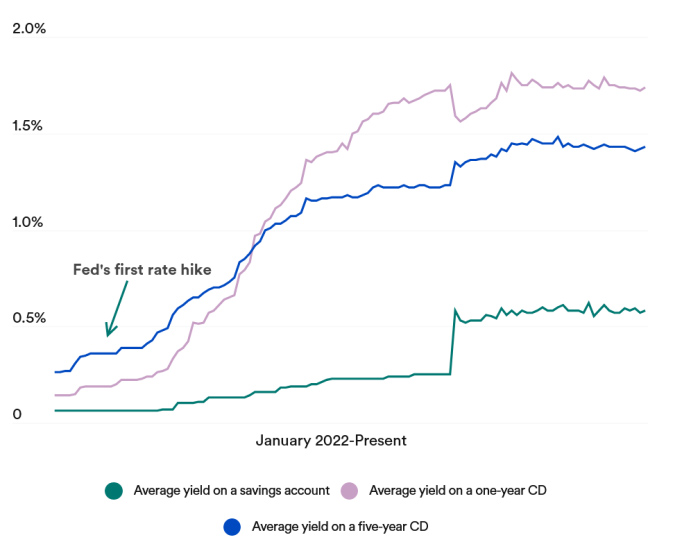

Interest rates are an embedded part of the economy at both the global and the household level – but what impact does the Effective Federal Funds Rate (EFFR) actually have on the economy, and why? In simple terms, the EFFR is the target rate set by the Federal Open Market Committee of the U.S. Federal Reserve (also known as the Fed), which meets eight times a year to determine it. So when you hear about "The Fed" setting or changing interest rates, people are referring to the EFFR. Other countries have interest rates too, but many follow suit with what the United States does or have interest rates appropriate for their local currency and economy. Commercial banks use the EFFR as the benchmark when borrowing and lending money to one another to cover any reserve shortfalls. How does the Fed know what interest rate to set? The Fed sets the interest rate based on a number of economic factors – mainly paying attention to signs of inflation, deflation, or a recession. Some indicators used include the Core Inflation rate and the Durable Goods Report, with the former providing clues on the cost of goods and latter indicating how many goods are being produced. While there are certainly numbers involved, it can also be a bit of guesswork as the Fed attempts to achieve its monetary goals with the main tool it has available: adjusting interest rates. During times of inflation, the interest rate is set higher (going up as high as 20% in 1980 and peaking more recently at 6% in 2001 when the dot-com bubble burst). Periods of recession trigger the opposite response, as the Fed attempts to stimulate the economy by dropping the rate as low as possible. We saw that happen during the Great Recession in 2008 and then again during the Covid-19 pandemic in 2020 when the Fed dropped the rate to 0%. How do interest rates impact the economy?Once the Fed has set the EFFR and banks adjust their prime lending rates accordingly, consumers are impacted by a change in short-term lending rates for loans and credit cards. Consequently, receiving a low interest rate can lead to house improvements, automobiles, and early Christmas shopping. Getting a higher rate – assuming a bank is even willing to lend to you at all – could mean putting off everything but emergencies. Pinning down the actual financial impact to consumers of the rate going up or down has proven difficult to estimate due to the number of factors in play, but some have attempted it. A paper from 2004 from the Center for American Progress estimates that when the interest rate goes up by 1%, it represents a change in a household’s annual costs of between $635 and $736 (converted to today’s dollar value). It's not entirely black and white, of course, as there are benefits when the Fed sets the rate high. Most notably, banks increase the yield for savings accounts as they strive to attract new deposits – meaning those with savings accounts will see significantly more gains than they would when the rate is low. As an example, the Fed started increasing the interest rate in May 2022. Through March 2024, the average yield for savings accounts has increased by a factor of ten, rising from 0.06% to 0.58% (represented by the green line below).

Source: Bankrate Consumers aren’t the only ones to feel the effect of a rate change, of course. Across the board, having a higher interest rate translates to a higher cost of goods and services, which in turn can cause businesses to shrink their workforces and put off expansion. By contrast, setting the interest rate lower can cause the economy to grow as businesses look to explore different avenues of services and take on new employees. The Global Effect of Interest Rates The effect goes well beyond U.S. borders. The reason comes, in part, due to the close relationship between the EFFR and the yield from U.S. Treasury Bonds. When the interest rate is set high and yields are accordingly also set high, investors from other countries are more compelled to maintain their holdings of U.S. Treasury Bonds – which in turn can lower employment and growth in other countries. Other countries may face higher exchange rates and export less to the U.S. as a result. At the same time, commodities priced on the U.S. dollar – including oil, gold, and cotton – will go up in cost, limiting the ability of other countries to import them. Since the U.S. dollar is the world's global reserve currency, the interest rates set by the Fed play a big part in international trade. The EFFR, in short, is tremendously impactful to the U.S. economy – which, in turn, sets the tone for the global economy. There’s a reason the Fed has been called the most powerful economic institution in the world. What will happen with interest rates in the future?Putting all of that together, can we expect interest rates to go up or down in the near future? With the threat of inflation receding, the Fed has made the prediction that it will reduce the EFFR to 4.6% by the end of 2024. That could change, of course, if the Fed determines that inflation is still a risk. Inflation is still very high, and the increased interest rates might be the only thing fighting that currently. Is it enough, though? It's of course impossible to predict what the Fed will do, but higher interest rates have been ongoing for a while now. So a cut is likely due, but without inflation under control, lowering interest rates could send inflation skyrocketing once again.

|

Send this article to a friend:

|

|

|