Send this article to a friend:

June

29

2024

|

Send this article to a friend: June |

|

What Happens When Rate Cuts Come Too Soon

Keep in mind that Federal Reserve Chairman Powell kept downplaying inflation as “transitory” in 2021, but also ended up wildly wrong (almost negligent). On the other hand, we actually live in the real world with real people. So back in 2021, we thought inflation might accelerate to 10% officially, before backing off. The result? The official inflation rate accelerated to a 9% peak in June 2022 before FINALLY starting to slow down a little. Which brings us to the present, and a critical question to ponder: When will the rate of price increases finally cool below the Fed’s target of 2%? Keep that question in mind as we continue… Inflation’s too high (and so are interest rates) As recently as March of this year, the Fed had been prepared to begin cutting the Federal funding rate. According to a Barron’s column, they “held” to a forecast of three rate cuts by the end of this year:

Unfortunately, that forecast was obliterated by a persistent inflation rate that is still hovering over 3% for one of the longest periods in economic history (since May 2021). A recent report by CBS News revealed that Fed rate-cut forecast has dropped to one, perhaps by the end of this year:

"The fact that the Fed scaled back the number of rate cuts from three to one is going to disappoint those who were hoping for a summer rate drop," said Bright MLS chief economist Lisa Sturtevant in an email quote captured in the same piece. But what if a rate cut at the end of 2024 is still too soon? As you’ll see, one country has already run that experiment… Here’s what happens when you surrender before the fight is over Just a few weeks ago, Governor Tiff Macklem celebrated as Canada’s central bank cut its primary funding rate by 25 basis points (0.25%), according to Reuters:

Economists could barely contain their excitement for another rate cut in July, according to the same Reuters report:

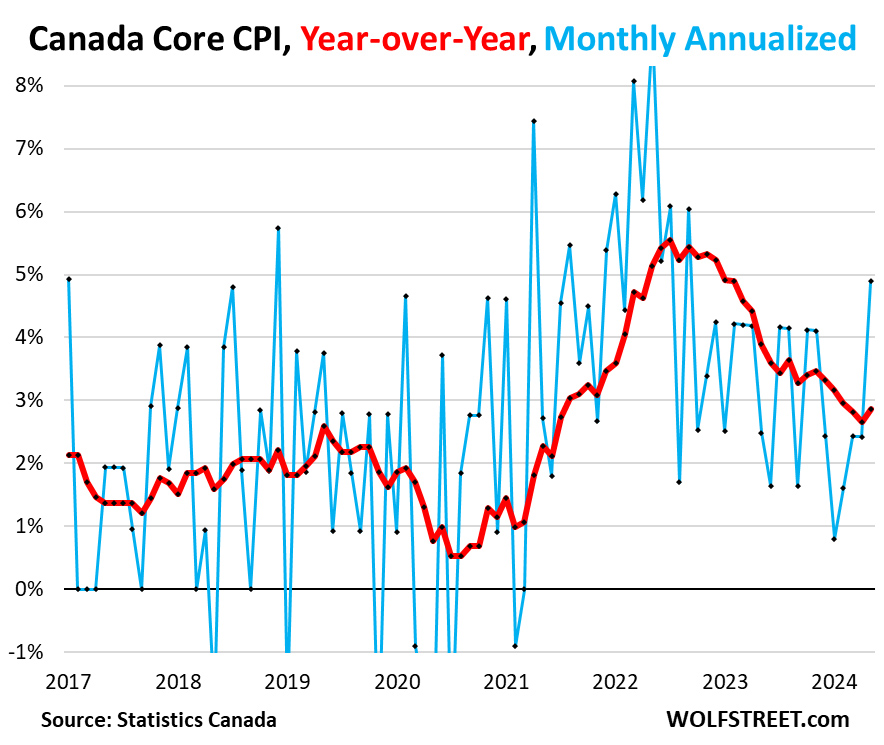

Unfortunately, reality appears to be throwing sand in the gears, because inflation isn’t going away quietly up north, according to Wolf Richter:

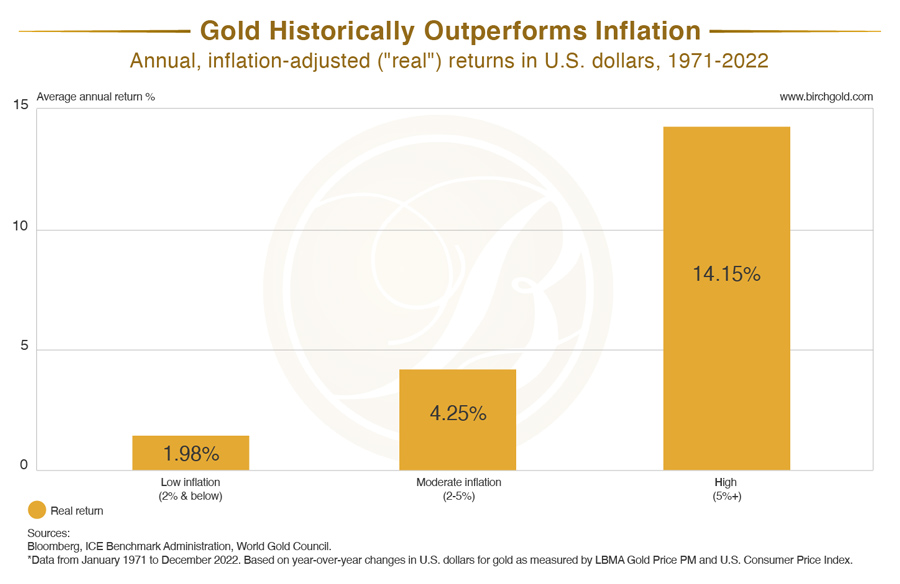

Wolf’s key insight above (bolded) is similar to the insight Jim Rickards offered a few years ago, when inflation was building momentum. That momentum appears to be regaining steam after Canada cut rates just a few weeks ago. You can see how the year-over-year Core CPI has ticked up, and the monthly annualized Core CPI has skyrocketed on Wolf’s graph below:  via WolfStreet Will the situation play out the same way if the Federal Reserve decides to issue a rate cut later this year? Using Canada as a potential case study, it would appear that Powell has to be very careful. Otherwise, capitulating to the “easy-money” crowd could prove to be catastrophic. Your best option is to devote a few minutes now, towards something that will offer long-term benefits regardless of inflation... Brush up on inflation-resistant investmentsNo matter what happens in the near-future, one thing is certain: The Fed is trapped. High interest rates are intolerable to debtors (including the world’s biggest debtor, the federal government). Bad for the housing market. And bad for the millions of American families who are using credit cards to pay for groceries. Low interest rates expand the credit supply – making debt cheaper, while at the same time devaluing the dollar’s purchasing power. We call that “inflation.” The Fed’s hoping to thread the needle between crushing the economy and stoking yet another inflationary speculative bubble. History tells us they don’t have a good track record of this – the last five rate hiking cycles ended in recessions. So the Fed’s score is 0 for 5 so far. Not very promising! That means it’s a good idea for you to consider educating yourself about the diversification benefits of inflation-resistant investments. One of those inflation-resistant investments (and arguably the best of them) is physical gold. That’s because physical gold consistently outperforms inflation, and has done so since 1971. When inflation is high, gold rises even higher:

Of course, you don’t want to forget about the other precious metals, either. By making the right moves now, you have an opportunity to put yourself in a potentially better financial position for the future through proper diversification of your retirement dollars. When you’ve diversified your savings thoroughly, you’ll be poised to weather any sort of economic storm, with the confidence that, no matter what the Fed does next week or next year, your long-term financial security is not at risk.

|

Send this article to a friend:

|

|

|