Send this article to a friend:

June

07

2023

|

Send this article to a friend: June |

|

The Trouble with Printing Money

Now, let’s talk Throw Back Tuesday. This series will delve into the rich archives of Peak Prosperity, dusting off historical pieces that resonate with our current times, demonstrating that the lessons of the past still hold immense value in the present. This venture reflects the nature of the daily discourse within our community, where we never shy away from revisiting older insights to guide our future direction. To our cherished long-time members, we invite you to join us in this journey of reflection. If you have a favorite piece of content from our archives, we urge you to share it with us – feel free to send us a direct message or simply comment below. After all, this is a collective endeavor, and your input is invaluable. For a while now, I have been expecting a coordinated, global central bank action that would seek to print more money out of thin air, or “QE” (quantitative easing), as it is now called. Now we have two of the most important central banks, that of the U.S. (the Federal Reserve) and in Europe (the ECB) having committed to open-ended, limitless QE. In Part I of this report, we analyze the actions themselves, and then in Part II. we discuss the implications to individuals and those with responsibilities to manage money. The most recent announcement came from the Fed, and it had these features:

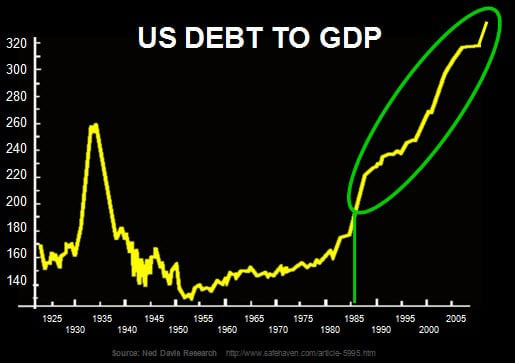

That laundry list can be summarized as ‘we will do whatever it takes.’ If anyone was still wondering if the Fed would ‘allow’ deflation to happen on its watch under Bernanke, perhaps the above points in combination with QE 1 and QE 2 will settle their minds. But will it work? Well, that all depends on what your definition of ‘work’ is. Without context, I really don’t know how to explain the importance of these recent actions. In order to address the implications of this historic move – remember, now is the time to keep a journal, as your future relatives will want to know all about what happened ‘back then’ – I’m going to rewind this story back a few years. Part I. Review of How We Got Here Since the very beginning of my public writings, I have leaned heavily towards the path of inflation, by which I mean money printing or its electronic equivalent, because even a cursory review of history will show that leaders have always chosen a little money printing today and the possibility of inflation tomorrow over the immediate pain of having to live within their means or with the consequences of their poor decisions. That was just a fancy way of saying ‘humans will be humans,’ and while our technology has advanced tremendously over the past few decades, our DNA blueprints are virtually identical to those found in people living 50,000 years ago. History can tell us much. Our current predicament has its roots way back in the early 1980s, when something changed in our collective psyches that allowed us to abandon thrift and savings in favor of spending and borrowing. This first chart, which references the U.S. (but in reality could apply equally well to most developed countries) show how borrowing has outpaced income (debt vs. GDP).

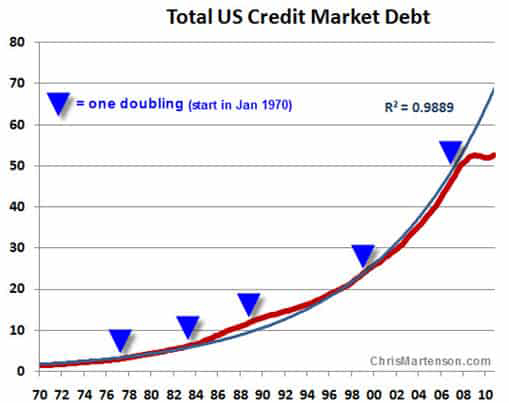

In order to believe that the Fed or any other central bank can get us back to ‘normal,’ you have to believe that it is normal for borrowing to exceed income and (here’s the kicker) that it can do so forever. Many people cling to the thin hope that somehow the Fed and its related entities across the globe can get us safely back on the yellow line in the above chart, angling forever upwards at 45 degrees. Well, if it’s not possible for you, personally, to forever borrow more than you earn without someday getting into financial difficulty, it is not possible for two or ten or 310 million of you to do so. The math does not change simply because a nation is involved instead of an individual. To really drive home the point that what our leaders have accepted as ‘normal’ and are endeavoring to resurrect is anything but normal, I find it useful to present this chart, which shows how the total credit market debt (that’s everything) in the U.S. has doubled and then doubled again and again and again over the past four decades:

What ‘getting back to normal’ requires is that we find a way to continue expanding debt exponentially with a doubling time of around 8 years. That’s what the last forty years have seen, and that’s the period during which every single leader at the Fed and in DC grew up and developed their views around ‘how the world works.’ Unfortunately that’s not how the world actually works. In the real world your income and expenditures have to eventually balance, and the only question is whether this is accomplished through diligence or catastrophe. The prior forty years were an admirably sustained departure from reality, but like all teenage road trips fueled with a pilfered credit card, the practices of those times were unsustainable and destined to end. Hopefully by widening up our lens a little bit, we can more easily appreciate that instead of being ‘normal’, the vast expansion of debt was actually quite abnormal, and therefore attempts to resuscitate its prior trajectory are (1) certain to fail and (2) going to make the final crunch a lot more painful and damaging than it otherwise needs to be. And oh, by the way – world oil is trading at $114 per barrel. Recoveries are tricky business at half that price. QE Will Lift Stocks and CommoditiesWhile left out of the official FOMC (Federal Open Market Committee) policy statements, but not Wall Street Journal editorial pages, is that a primary goal of the Fed is to boost stock prices. The stated reason is that the so-called wealth effect will lead households to view their rising portfolio statements and go out and spend more money. An underlying reason has to also be the fact that pensions, endowments, and other long-running actuarial pools of money are being destroyed by too-low rates of interest on bond holdings and desperately need stock-market gains to cover some of the shortfall. QE and its distant cousin Operation Twist both serve to lift stock prices. QE does this in two ways – first by dumping money into the financial system, which then has to go somewhere and do something, so some of it ends up in the stock market, and second by driving down interest rates, which has the tendency to push money into stocks. Operation Twist, which is balance-sheet-neutral for the Fed (short-dated securities are traded for long-dated securities – it’s a swap) only serves to drive down interest rates on the long end of the curve. No new money is created. As we can see, stocks respond well to both types of stimulus:

As we might also note, when the stimulus ends, stocks respond unfavorably. It would seem that the Fed is now trapped and that if it ever pulls away from the market there will be a rout of historic proportions. Commodities really only respond to new money, which makes sense. Lower interest rates on the long end of the curve do not change the preference for commodities much, and so Twist might be expected to do little, if anything, for commodities. That’s exactly what we see in the data:

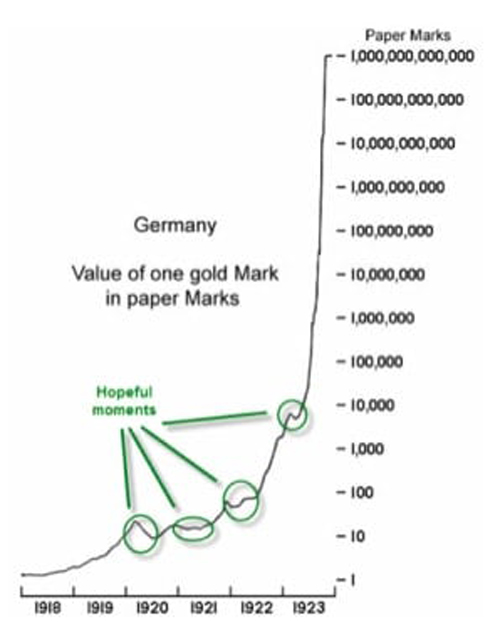

While the Fed may not be too pleased with rising commodity prices (with all that’s going on in the world with unrest, drought, and $114 Brent crude), it seems quite likely that rising commodity prices stand a good chance of being a feature of QEternity, or whatever this new program will finally be branded. The Trouble with Printing MoneyIt is against the larger backdrop of borrowing and spending well beyond our means that we need to interpret this most recent effort by the Fed to print our way back to prosperity. One way to look at the $40 billion per month in new printing is to compare it to individuals and households. Remember, money only comes into your life through effort, and that’s why it has value and can function as a store of value. Once upon a time you could make the choice as to whether to work to find money (by mining gold or silver) or work to earn money by farming or practicing a trade, craft, or service. Note that work was always involved. What does it mean that the Fed can just up and print $40 billion per month indefinitely without performing any work whatsoever? Well, let’s put that in context. If an individual earns $50,000 per year, then each month the Fed is effectively printing up the yearly output of 800,000 such individuals. Said another way, if you earn $50k, then you’d have to work for 800,000 years to earn the same amount of money the Fed prints each month. Given that the median household income is ~$50k, this means that after one year of MBS purchases, the Fed will have printed up as much money as 9,600,000 households will have earned. Presto! Just like that, the Fed is effectively creating the exact same purchasing power as nearly 10 million US households, or 25 million people (I’m rounding a bit here). And nobody had to do anything except push a key on a computer a couple of times. While the Fed can wrap this magic act in all sorts of covering language about dual mandates, maximum employment, and price stability, the simple fact remains that money printed out of thin air cannot, has not, and will not ever lead to prosperity. How could it? It arises without any effort at all, no work performed, no goods transformed or lives improved, no land planted and tended well, no services rendered, and no capital formed. It is just conjured into existence. It is just new money tossed after bad debts, with both remaining to work their different insidious effects on the economy and our daily lives. If printed money could lead to prosperity, trust me – some culture would have worked it out long ago, because people every bit as clever and determined as those alive today (and with the same DNA software installed) have tried it again and again. If it could work, then we should just print every household up a nice $1,000,000 check each year and let everybody stay home, take vacations, and drive nice cars. It’s just an absurd notion, and this is why you should keep a journal – you live in absurd times. Part II. A Process, Not an Event Okay, the ECB and the Fed are now in the game with unlimited, open-ended commitments to print as much money as necessary to get back to the same rates of GDP growth we had in prior decades. I should note that the ECB actions, at least, will be fully sterilized, meaning that they won’t boost the money supply – at least that’s the plan right now. Soon enough, Japan is going to have to join the fray simply because it cannot afford a stronger yen here; it will have to print because it is first, second, and last an export economy. After that, it is anybody’s guess as to how long China will put up with its massive $3.2 trillion in foreign exchange reserves being debased willy-nilly, but my vote is ‘not long.’ These latest rounds of QE are certainly unnerving and may prompt many of you to want to accelerate your own private efforts at financial, emotional, and physical resilience. By all means, use these moments to focus your attention and efforts. But also be aware that we are experiencing what is certain to be a very long process rather than some dramatic event. For reference, note that one of the most dramatic and rapid inflationary processes of the last century took six years to unfold. How long would it have taken if every country and every currency surrounding the Weimar republic was engaged in the same dynamic of overprinting? And what if the Weimar also happened to be the world’s reserve currency? I don’t know, but I am certain it would have taken longer than six years. Without a frame of reference, it can be really hard to get one’s bearings, particularly in this case with competing currencies found right over the borders.

My point here is that as dramatic as these recent QE announcements have been – and they are historic – the effects are going to take many months and years to play out. It is my view that we are much closer to the beginning of this crisis than the end. In fact, unless something magically changes and we can get back to cheap oil somehow – and I truly believe magic would have to be involved, for that to be possible – we are never going back to ‘how things were.’ It is a new world, and our most pressing predicament happens to be that we have a money system based on debt, which requires perpetual exponential expansion to function well. It is not functioning well right now, and that should be completely obvious. The mystery is that so many continue to divine the Fed tea leaves as though the right combination of interest rates, liquidity, and thin-air money could somehow, in isolation, overcome the steady erosion in the quality of oil, mineral ores, fisheries, soil, and aquifers. They cannot, and the longer we overlook this most basic of concepts, the worse the eventual disappointments will be. Get yourself mentally prepared for a very long and bumpy ride. What’s Really Going On Here? Another possibility is that the Fed and the ECB have plenty of intelligent people inside their walls who perfectly well understand that things are seriously off the rails. Here’s how Bob Janjuah of Nomura Securities put it (emphasis mine):

I share Mr. Janjuah’s view that the calm words of the monetary authorities are belied by their actions (remember, lying is one of their stated tools) and fear, if not panic, is driving them. They may not have the views on energy and the environment that we do, but they know that something is desperately wrong with everything they thought they knew about how the world works. I’m sure it is deeply troubling to them that their trillions have not yet really fixed anything, and they are increasingly concerned. If the only tool left is a permanently open monetary spigot, then we can all just settle down and wait while the dollars/euros/yens/etc. glide paths eventually intercept with zero. In the meantime, we need to prepare and control our risks as best as we can. For now, I am relatively certain that there’s a sizable gap between what we are being told and what the authorities are saying. As we move along, that gap is certain to grow. Because let’s face the facts here; the incredibly intertwined predicaments of demographics, national insolvency, debt, falling net energy, and increasing environmental pressures cannot possibly be addressed by a few Fed officials sitting around a mahogany table every six weeks deciding how much thin air money to inject into the economy. It’s Binary – There Are Only Two Outcomes What it comes down to is two outcomes – either the Fed’s plan works, or it fails. There’s not a lot of middle ground on this one. The major problem is that neither outcome is favorable. Here they are:

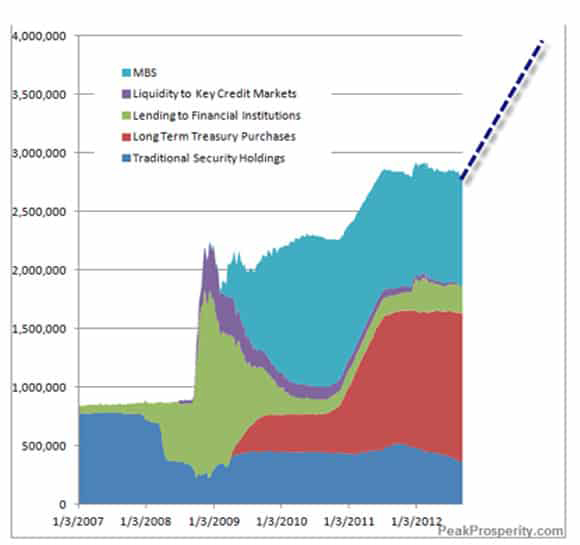

Let’s start with the second one first. The way this would play out is that despite tossing hundreds of billions of dollars, and then trillions, into ‘the economy,’ the Fed’s efforts fail. And the next thing you know, selling begets more selling, a liquidity event seizes the markets, counterparties begin to fail in domino fashion, governments get squeezed, taxes are hiked, the economy plunges, and it just gets worse from there. Eventually all the trillions of dollars of excessive debt built up over generations will be washed away, but the process will look and feel exactly like a gigantic catastrophe for everyone. Dreams will be dashed, institutions broken, careers ruined, and our collective sense of what’s possible will take an enormous blow that will not recover for generations. I certainly understand the very sincere desire by the Fed to avoid this path. However, the other path involves printing enough to prevent Path #2 from being our destiny. In doing so, the Fed would slowly become the entire market, the purchaser of last resort, the place ‘investors’ look first for their clues on where to place their bets. There will come a point after which the Fed cannot possibly unwind its balance sheet because to do so would crash the markets and initiate a quick hop over onto Path #2. Maybe we’ve already passed that point of no return? Looking at this chart of the Fed’s current and projected balance sheet, keep in mind that the $800 billion level it started from back in 2008 was built up over 90+ years of operation. Four years later, it has tripled, and it’s on its way to quadrupling by the end of 2013.

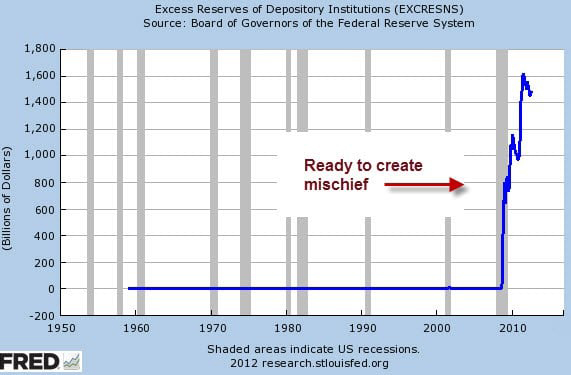

When the Fed does this, one of the effects is that vast gobs of excess reserves are created within the banking system, which will someday come roaring out seeking something, anything to do besides remain parked at the Fed earning 0.25%.

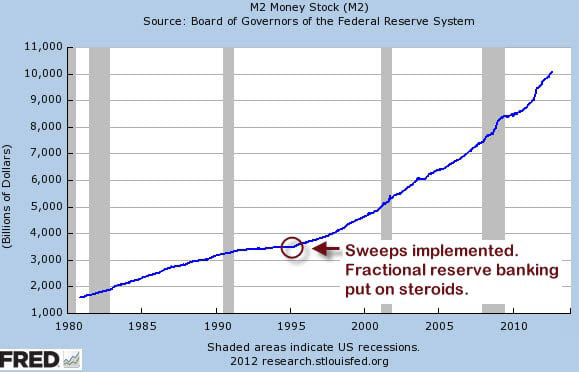

Another function of the modern Fed is to keep the money supply growing – no matter what. I think they’ve done an admirable job here, because the Great Recession cannot really be detected on this next chart except by the rapid upwards bump it takes in that last gray bar to the right.

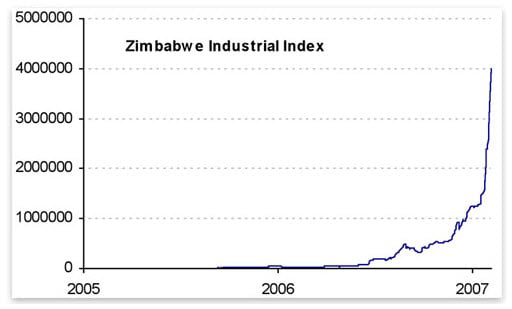

Also of note in this chart is the inflection point circled in red, which coincides with an important moment in the current crisis, the time when Greenspan’s Fed implemented the infamous “sweep program” allowing banks to effectively dodge the 10% reserve requirement almost entirely. Without such a ‘hindrance,’ there was no effective limit on how much credit a bank could issue, and therefore no effective limit on how much money could be created within the banking system. Briefly, if you have a demand account (either checking or savings) at a bank, you are part of the sweep program. What happens is that each night at 12:00, each bank must take a snapshot of all of the money its depositors have with the bank and prove that they have 10% of that amount set aside in reserve. However, the sweep program allows banks to set up dummy non-demand accounts for each demand account it holds, sweep the demand money into that account at 11:59, take their reserve snapshot (hey, there’s nothing there!), and then sweep the money back into the demand accounts. Without having to keep 10% in reserve, the banks are free to hold absolutely nothing in reserve, which effectively explodes the lending opportunities for banks. If banks that are required to hold 10% in reserve can suddenly reduce that to just 1%, then the amount that can be lent goes up by a factor of eleven. [Math Note: $100 in deposits can be turned into $900 of loans under a 10% reserve requirement, but can support $9,900 of loans under a 1% requirement] The reason we go into all of this detail here is to note that the combination of enormous excess reserves held by banks and a non-existent reserve requirement means that the tinder has been carefully laid, gasoline spread all about, and onlookers anxiously awaiting the spark. Should that spark be struck, then the theory is that the Fed will simply reverse its balance-sheet holdings, take back all of that excess cash, and that will be that. In reality, by the time the Fed gets in gear, those excess reserves will be supporting an extraordinary amount of new borrowing, meaning it won’t be so simple to claw it back. (Heck, I’ll be right in there borrowing money as fast as possible to buy things with, myself.) Where We Go from Here If we accept the proposition that we are now four years into this financial and economic crisis and that all of the trillions spent to date have forestalled but not prevented the inevitable conclusion (which involves massive losses and tightened belts at a minimum), and we have convinced ourselves that the central banks will simply keep printing because that’s all they have left, then what we expect to happen next is really pretty straightforward. Unless the course is radically altered, the end game here is the destruction of the involved currencies and enormous fiscal crises for the afflicted countries. Between here and there exist a lot of time and territory, and we still need to know what to do with our wealth and our efforts in the here-and-now. Here’s how I see things at the moment. StocksThe stock market loves fresh money and low interest rates. They should go higher, especially in those countries that manage to engineer their currencies to go the lowest. A case in point is the Zimbabwe stock index, which expanded exponentially in 2006 and 2007 for no other reason than that the currency was collapsing.

(Source) It’s worth pointing out here that Zimbabwe’s industrial producing and its overall economy were collapsing at this point, indicating that one can certainly have rising asset prices and collapsing activity at the same time. It is also worth noting that even as Zimbabwe was experiencing capacity utilization rates that had declined to just 10% and unemployment of 80%, inflation was raging. Some point to idle capacity in workers and industry as a reason that inflation cannot really take off, but Zimbabwe proves otherwise. In a world of stable money, it is unthinkable to have a smashed economy, high unemployment, and a rising stock market. However, in a world of debased money, such an outcome is not only possible, but likely. With that said, I am not in a position to want to buy stocks hand-over-fist just yet. I remain unconvinced that $40 billion per month is sufficient to overcome all the other forces at play, and I will wait to see just how serious the Fed and ECB are. I think the markets are waiting, too. I expected more of a pop with follow through than we got, meaning that the markets had already pretty well priced in the QEternity announcement. Still, stocks, especially those positioned with strong balance sheets, good cash flows, and selling essentials (rather than purely discretionary) should do better than average during the next few years. BondsIn the near term, the Fed has the firepower to continue to drive long-term interest rates lower in the U.S. I am less convinced that the ECB has the political mandate to keep the Portuguese, Spanish, and Italian bond markets under control, but we’ll see. In for a penny; in for a pound. It really wouldn’t make much sense for the ECB to do anything less than everything necessary, but time will tell. Over the longer term, I would not be caught dead holding bonds in a regime of currency debasement. Might as well directly burn your money for warmth or donate it to your favorite charity while it still has some use. Back in the 1970s, when the world was going through a similarly difficult period of financial and monetary recklessness, bonds were known as ‘certificates of confiscation’ meaning your eventual return would be swamped by inflation. As painful as it might be for certain pensions, endowments, and other long-horizon funds, I would forgo the meager returns offered by longer-dated government paper here and stick to the short end. The percent or two difference in yields is just not worth the risk. CommoditiesHere the story is clear enough for food and fuel, two things that sustain a fairly constant demand regardless of circumstances. Combined with reduced output for grains (due to what appears to be an increasingly unstable weather system) and steadily higher costs to produce marginal new oil (with Iraq being something of a lone exception here), the new QE efforts have a very good chance of igniting truly outstanding price hikes in food and fuel over the coming years. I am less bullish on iron, copper, cotton, and other items for which the demand can vary enormously depending on economic conditions. Harking back to Zimbabwe again, the demand for such items fell as food and fuel consumed ever-greater proportions of disposable income. LandI remain a huge fan of productive land (both farm and woodland), but if and only if adequate water is part of the equation. Without some form of water, preferably adequate surface water, perhaps captured in the farm pond method mentioned by Joel Salatin, the value of land will be defined by rainfall, an increasingly dodgy prospect. If you are thinking of moving to a non-traditional IRA and buying land with the holdings (as I am), then now is a good time to get that process rolling, because I would plan on a full year to get the vehicle in place and find land to buy. GoldWell, at the risk of being a broken record, gold is my favorite and preferred way to protect your wealth during a period of active currency debasement and/or the unwinding of too much leverage (debt). It is the only monetary asset that is not simultaneously your holding and somebody else’s liability – a very important attribute during times when control fraud runs rampant and unquantifiable counterparty risk exists. Be sure that your core position in physical gold is safely secured, and then think about your answer to this question: How much of my wealth do I want to be absolutely sure will not go to zero because of a systemic crash? Your response should first be allocated to your homestead and the remaining balance to gold and to a lesser extent silver. My expectation is for gold to go a lot higher from these levels. Will it go lower by next month? I really don’t know. But I have very few doubts over the mid to long term because every single fiscal and monetary step being taken right now is increasing the odds of an eventual fiscal and/or monetary crisis in the US. We’ve not yet even remotely reached the blow-off phase for gold, because most people I talk to in the U.S. still look at me funny when I mention gold, many offering such pearls as you can’t eat it, you know as if that were some sort of useful retort born of insight. To counter, I will sometimes ask them to eat a dollar bill for me, even offering to sweeten that up to a ten spot if they balk, but so far I’ve had no takers. Lurking in the realm of possibility is the idea that gold may be remonetized in response to some form of global currency crisis. If this happens, then gold will going a lot higher than any of us can currently imagine, both in current dollar terms and especially in whatever future debased terms will exist in that moment of crisis. SilverSilver has been on a very good run of late, ever since breaking up out of its year-long wedge pattern. From a 10-20 year standpoint, I am as bullish on silver as anything you could name, mainly because all known ore bodies of commercial value will have been depleted by the end of that period. And then what? Industrially silver is irreplaceable for certain applications in electronics and healthcare. How much is an industrially irreplaceable precious metal worth, when it will someday be depleted? More. A lot more. And if silver ever gets remonetized…again, who knows? It is time to start moving even more out of fiat money, especially U.S. dollars, euros, and yen. There’s no panic, no real urgency, so no need for quick, rash decisions. Instead, pretend as if someone has rung a bell and said, time for the next phase of this adventure to begin. All Aboard! (…the USS Risktanic) As for the final act of all this, which I truly believe ends in enormous fiscal crises for the U.S., Japan, and much of Europe, it will do what every great financial panic has always managed to do – destroy most of the wealth for most people. That’s what great bear markets do after things have gotten out of balance and need to be reset. In such an environment, he who loses least gains the most. In the great game of ‘risk on, risk off’ where big money managers shuffle, trot, and then stampede back and forth between risky asset (‘risk on’ = stocks, certain currencies except USD and JPY, and oil of late) and ‘risk off’ assets (VIX, government bonds from safe countries, USD, and JPY). However, with the Fed mispricing money itself and bonds, it has had the effect of piling everybody into increasingly risky asset stances even though those are ultimately no safer than the places that were just vacated. The Fed has openly stated that its goals are to get people back into the stock market and to drive up the price of financial assets because they favor the wealth effect that the Fed imagines will follow. Instead, what they are doing is buying temporary asset gains at the expense of forcing additional risk on portfolios. Progressing from the outside in, investors will leave the riskiest assets first, and then progressively work their way towards the center. The very center of this bubble machine, the core of the monetary particle accelerator, is the U.S. government bond market. If I read history correctly, the progression of the final act will be to herd everyone towards the center of an increasingly unstable nuclear reactor, where the most wealth of the most people can be vaporized. This is not Machiavellian; it is simply a truism that decades of excessive claims have to be abandoned and massive losses have to be taken. If not by a process of default and deflation, then it must happen via a process of creating additional claims that inflate away with the rest. You know where I stand on those probabilities (9:91). The tragedy here is that it is all so completely obvious and avoidable. There’s no law (yet) requiring anybody to keep their money in U.S. Treasury bonds vs. in gold or farmland or other tangible assets, the utility of which cannot be debased via the actions of Fed and ECB staffers. Yet I remain convinced that the fate of most will be to lose most of their wealth during this process by trusting that the majority cannot be wrong when that is exactly the most likely case. Conclusion Between the Fed’s QEternity program and the ECB’s OMT (Outright Monetary Transactions) program, it seems clear enough that whatever is spooking and bedeviling the central banks, it is sufficient to cause them to up the ante here. If these moves mark anything, it is that we are now in a new phase of the crisis. On one hand, it is a more boring part, because almost everybody has experienced dramatic baseline shift over the years and now yawns at news that would have caused them to run around like their hair was on fire just a few years ago. On the other hand, it also reveals that the crisis is far more serious than anybody in power really cares to admit or possibly even understands. This entire trajectory is perfectly and obviously unsustainable; therefore, every attempt to sustain it is a big waste of time, energy, and resources. Instead, we really should be having a very honest conversation about what we can and cannot afford, where we want to position our resources (yes, I am talking about setting national and even global priorities), and where we want to be in twenty years, and then applying ourselves towards those things. These attempts to sustain the unsustainable are getting more desperate and have perhaps slipped past the point of being absurd. Yet here we are. It is my contention that the future holds more and more money printing and that the central banks are very far from throwing in the towel and then standing by to observe a full deflationary breakdown sweep the land. I cannot say for sure, but the chance of experiencing a very disruptive future seems quite high and getting higher. If you live in South Africa, Libya, Afghanistan, Iraq, Iran, Syria, Spain, Portugal, Greece, China, Japan, or any of a dozen other places, perhaps you’ve already experienced the first waves of disruption. I worry that by treating symptoms and not causes, the Fed, et al., are delaying the arrival of something that only grows worse with time, so I question the wisdom of this path. You should use this most recent QE program as another gentle wake-up nudge to keep going with your plans and preparations. Resiliency and engagement are the operative words. We can use the comments area here on the site to address specific ideas, comments, and questions. I will be happy to do what I can to help address your questions and be part of the conversation. Someday I will be going “all in,” which means emptying my bank accounts of cash to apply towards other purposes, but that time is not quite upon us. I had thought this QE announcement might be bigger, and I think it eventually will be, but for now it’s not quite there yet. When I do go “all in,” I will, of course, send out an Alert.

CHRIS MARTENSON, PhD (Duke), MBA (Cornell), is a former Vice President at SAIC, worked for Pfizer, and created the viral video series, The Crash Course, which has been viewed by millions of people and translated into 4 languages

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)