Send this article to a friend:

June

16

2023

|

Send this article to a friend: June |

|

5 Factors that Make or Break Retirement Plans

How much should I have saved for retirement? As you’ll soon discover in this article, the answer to that question isn’t a simple one. The good news is, if you take the following five factors into consideration, you’ll be one step ahead of most Americans who are saving toward their retirement dreams. Let’s start with the first factor… #1 – Retirement saving rules aren’t set in stone If you’ve ever searched for retirement saving advice online, you’ll come across common “rules” offered by a number of different experts. For example, Fidelity has a general rule of thumb for retirement estimated savings:

If nothing else, it’s a starting point – but it tells us how much to save, rather than how to save. Typical suggestions for how much of your salary you should save, starting in your 20s, look like this:

Again, nothing wrong with that guidance either, so long as you can keep up the pace. For most people, reality enters the equation and they just can’t keep up. The consequences of insufficient savings are cumulative, just like inflation. The farther behind you are, the more catching up you have to do:

This is why there are no set-in-stone retirement saving guidelines. Everyone’s daily life is different, our challenges as unique as our hopes and dreams. Craft your plan according to your situation! And remember, plans need to be flexible… #2 – Your plan must adapt as your circumstances change

You must remember to be flexible when life happens:

Employment, health and income will likely change over the course of your life. Sometimes for the better, sometimes for the worse. Any big change in your circumstances should also be reflected in your retirement savings plan. But we shouldn’t limit our thinking to what’s happening right now. We must consider the future, too. The lifestyle you want during retirement must reflect reality as well as your desires. That usually means considering both expenses and discretionary spending:

Nobody wants a “below average lifestyle,” but what will it take today to get there someday? That’s the equation we have to solve, and not just once, but regularly… #3 – Revisit your plan and track your progressChange is the only constant. Life events, for better or for worse, make demands on our time and money. That’s why it’s a good idea to revisit your retirement plan frequently, track your progress against your goals, and make any necessary changes. That last part is crucial. It’s not enough to know you aren’t on track – you have to do something about it. If you’re not on track to meet your goals, here are some recent suggestions offered by experts:

Solving any budget shortfall boils down to two things:

(Are you reading this, Congress?) An article on Forbes reminds us not to neglect our emergency fund in our planning:

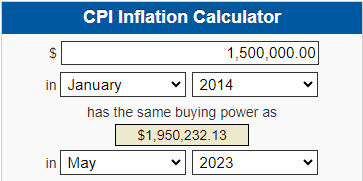

That’s smart – an emergency fund can make or break your financial planning when “life happens.” There are some things we just can’t plan for specifically, so we must plan for them generally. Things like emergencies. And the effects of inflation. #4 – Your spending power declines over timeWe talk about this a lot, and it’s important. Hopefully, if you’re doing everything right, the balances of your savings accounts will increase over time. Some of that growth will be offset by the declining purchasing power of the dollar. Imagine for a moment you made your retirement plan back in 2014 and predicted you’d need $1.5 million for the retirement of your dreams. Today?

Via BLS CPI inflation calculator That’s a 30% increase in the number of dollars you need for the same lifestyle you planned for. In less than a decade. That’s a major reason why it’s crucial to reevaluate your plan regularly – and more often than once every ten years or so. You can’t just think in terms of a certain “magic number” of dollars, after which your dream retirement will be guaranteed. Yesterday’s “plenty” is today’s “minimum” and, all too likely tomorrow’s “not enough.” In other words, it’s virtually impossible to plan for tomorrow’s expenses in today’s dollars. But don’t give up! Inflation will be a problem, but there are possible solutions. #5 – Diversification can help One strategy that is just as important as factoring in the changing value of assets into your retirement planning is having an effective diversification strategy. Effective diversification diminishes volatility due to economic conditions. Ideally, your savings include some economically-sensitive assets that grow during good times, and “countercyclical” assets that grow during bad times. That’s what makes physical precious metals a good asset to consider. Metals like gold and silver have had inherent value for thousands of years because they are tangible and finite resources. They aren’t controlled by any central bank or any government. They can’t be “printed” by the Fed. Gold especially tends to hold its value even in the worst economic circumstances. That alone makes it an invaluable asset for diversification purposes. Diversifying with physical precious metals, gold and silver alike, can also help you see beyond the numbers and focus on maintaining your buying power well into the future. Physical gold ownership isn’t just for the super-wealthy anymore – it’s for everyone. Are physical precious metals right for you? The good news is, you can get all the information about them for free right here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)