Send this article to a friend:

May

02

2024

|

Send this article to a friend: May |

|

American Families Are Running Out of Time

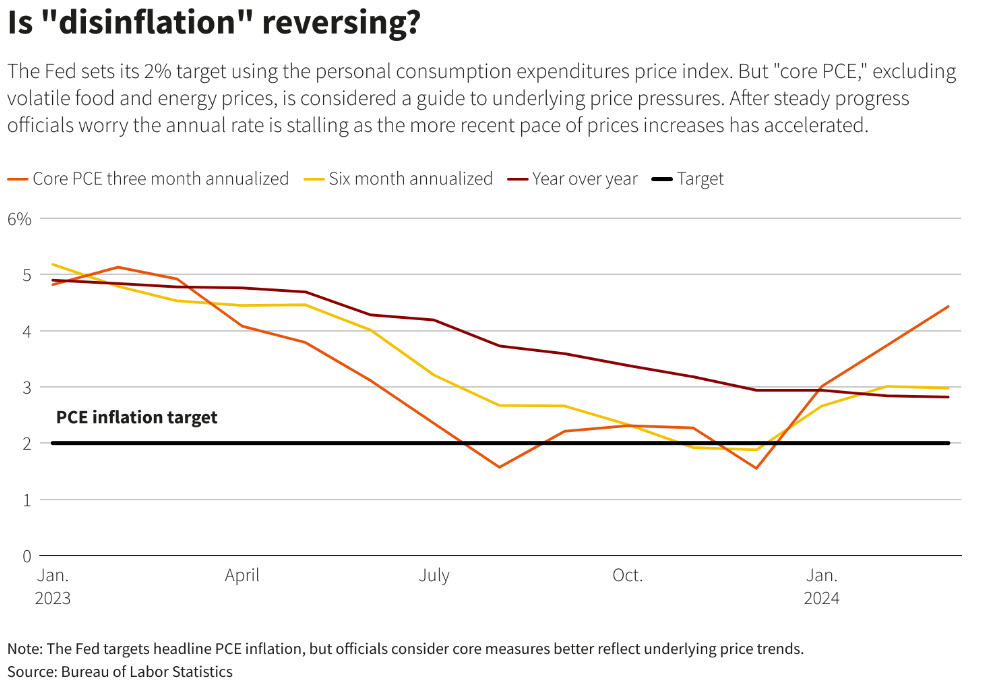

Here’s the short version: The overall inflation rate is heating up again (officially 3.5%), which is almost double the Fed’s target rate of 2%. On top of that, personal budgets are getting tapped out (including credit cards), which could mean consumers won’t be able to keep up with increasing prices for much longer. That means a major recession could still be lurking just around the corner, which is something that mainstream analysts appear to have a hard time coming to grips with. Let’s take a deeper look at the latest information… Even the Fed’s favorite inflation gauge is heading in the wrong direction Fairly recently, it appears like any mainstream coverage of inflation has devolved into reporting the “core PCE” rate, which excludes both food and energy prices. Of course, it’s pretty silly to exclude the things that consumers need to buy on a daily basis from the calculation for inflation. John Williams from ShadowStats.com explained one possible reason why the “fantasy” inflation calculation is even used:

But let’s leave all of that aside for a moment. It appears that even the PCE inflation rate is heating up again:  That’s right – prices are moving in the wrong direction. Again. Even according to the Fed’s favorite inflation gauge… (At least they aren’t trying to play any Krugflation games with us.) This is a problem for American families already struggling to pay the bills. A lot of them are already on the ropes… Households falling farther and farther behind A recent report summarized the tension between rising consumer spending and the soaring cost of living:

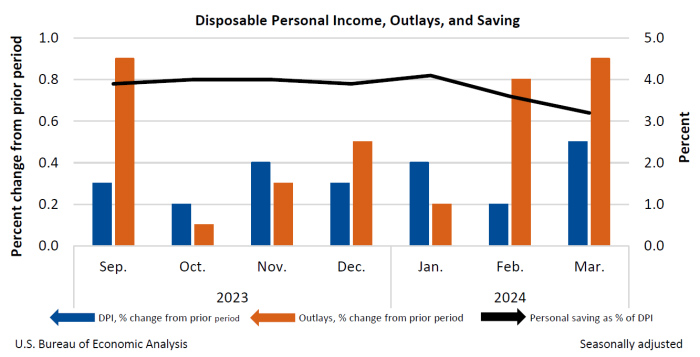

This is what a “precarious scenario” looks like to an economist:

Disposable income (blue bars) is falling short of of cash outlays (orange bars). And it’s been that way for a while now… And as you’d expect, the nation’s personal savings rate has also been dropping. Right now, Americans are saving, on average, 3.2% (most retirement advice you’ll see recommends saving a minimum of 10-15% if you ever want to retire). Americans haven’t had this much trouble making ends meet since the throes of the Great Financial Crisis back in April 2008. Credit card balances are maxed and it looks like there’s a crisis on the horizon:

Well, when prices on, you know, things like food, gasoline and housing rise 30% in three years – what are people supposed to do? Stop eating? So credit card balances rise along with cost of living. To the point where banks are getting nervous. We’re running out of time. Where’s our soft landing? The Federal Reserve has tried to raise rates to cool off the rate of inflation, and since July 2022, you might have thought it was working. Unfortunately, with inflation heating up again, it doesn’t appear to be working as well as Chairman Powell thought. The Fed is under pressure from two sides.

Higher interest rates might crush inflation – but not only inflation. Chairman Powell is too afraid of another round of bank collapses. Banks can’t cope with interest rates at this level (exhibit A), let alone higher rates. That’s why we aren’t seeing any hints of inflation-crushing interest rate hikes:

Just three months ago, the investment industry forecast six cuts in interest rates this year! Wishful thinking. What happened to the so-called “soft landing” anyway? The Fed can’t even see the airport yet – but the plane is descending nevertheless. And we’re all buckled in… Remember what the flight attendant says? In the unlikely event of an emergency, save yourself first. Buckle up for the unplanned landing ahead Everybody has an opinion. The White House says we’re lucky enough to be on the fastest, smoothest flight in American history – we’ll all make our connecting flights! Mainstream analysts are slightly less optimistic, forecasting a 70% chance of a smooth, easy landing that won’t disrupt anyone’s future plans. Jamie Dimon, CEO of America’s largest bank, has a vested interest in a booming economy. When the nation does well, the nation’s banks do well, too. You’d expect Dimon to talk his book… Instead, he’s more of a realist. He believes the odds of a soft landing are around 35%. That’s right, folks – Dimon probably has the most to gain from gaslighting us. Instead of shoveling nonsense about rainbows and unicorns, what does he say? We have a TWO IN THREE chance of a crash landing. Looks like even the cabin crew is panicking now… Listen: Just like on the airplane, when the mask drops from the overhead compartment, it’s time to focus on saving yourself first. In a financial sense, that means right now is the best time to examine your savings. Should you consider diversifying with “crash-resistant” assets? Taking a few minutes to learn about inflation-resistant investments like gold and silver could be a good starting point. And if you do decide that diversifying your savings with gold and silver is a wise decision, you can learn how to purchase physical precious metals right here.

|

Send this article to a friend:

|

|

|