Send this article to a friend:

May

16

2024

|

Send this article to a friend: May |

|

Will High Inflation Ease Up Soon? You Won't Like the Answer

If you were hoping that the official inflation rate would ease, especially on the necessary goods and services you need to buy, then you might have to be patient. Even Federal Reserve Chairman Jerome Powell thinks so, while highlighting the crucial fact that rates won’t be coming down anytime soon, either:

Obviously, weary Americans aren’t likely to welcome the idea that they will have to be patient. Especially after they’ve already suffered through nearly four years of Bidenflation. According to a recent report, American households are still spending despite higher prices, but how much longer can they keep up?

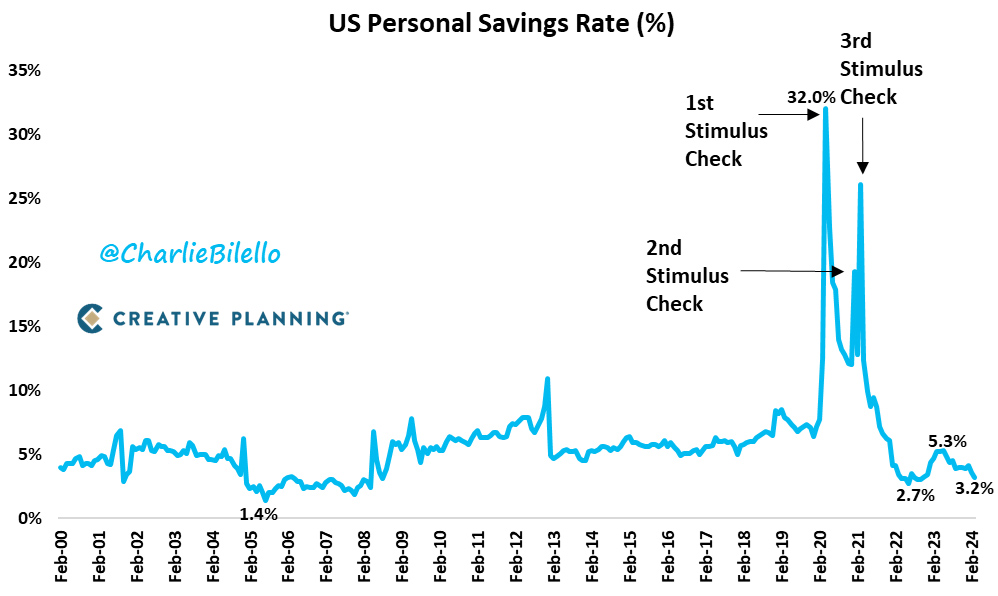

The real reason households are still spending is because they still have to purchase necessities (like food, fuel and energy). Even so, they’re still paying much higher prices thanks to persistent inflation. If that weren’t bad enough, as you can see on the graph below, consumers’ savings accounts have been running dry since February 2022:

via Charlie Bilello

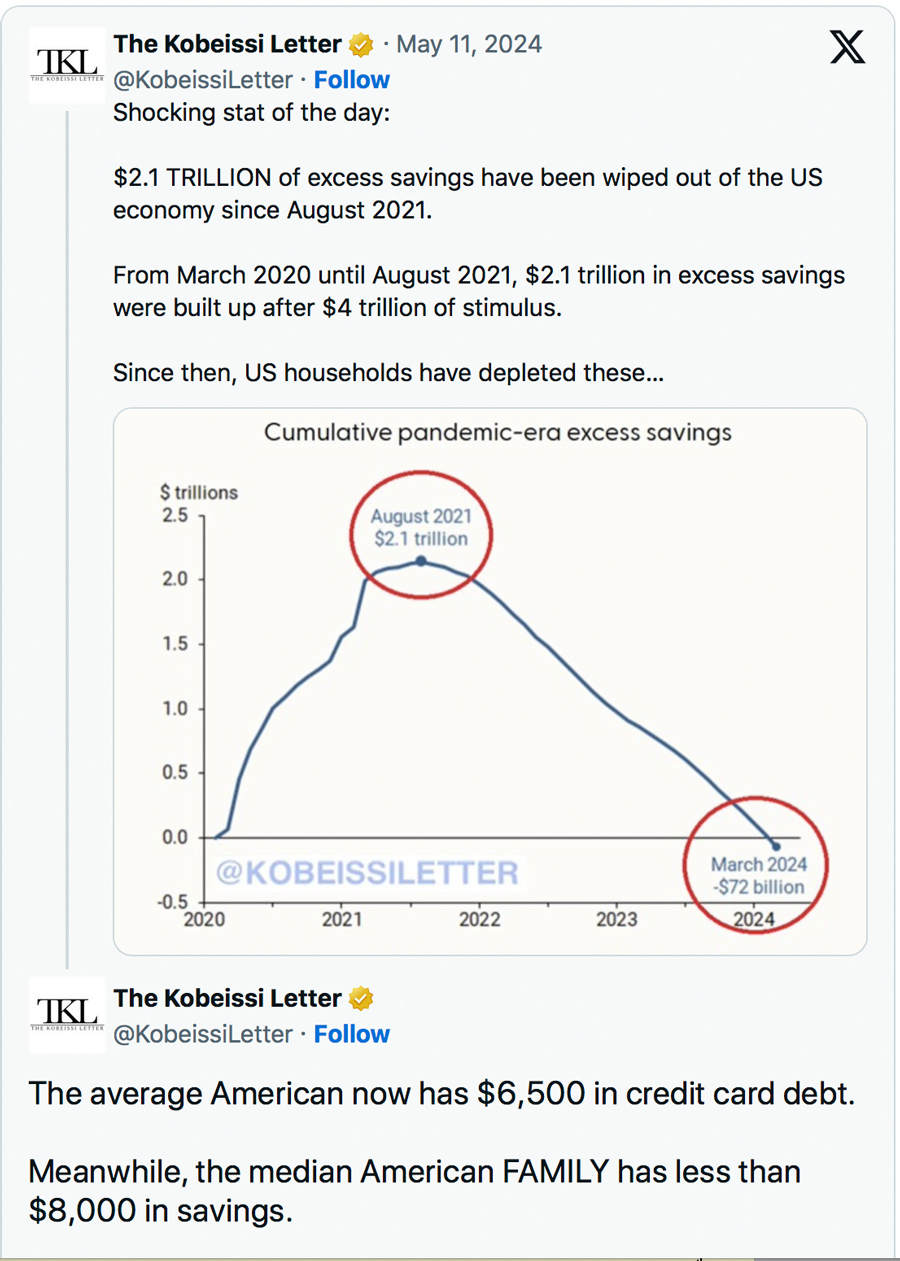

As you might expect, with savings running dry, consumer credit card debt is skyrocketing. Adam Kobeissi nicely summarized both the savings and credit card debt situations:

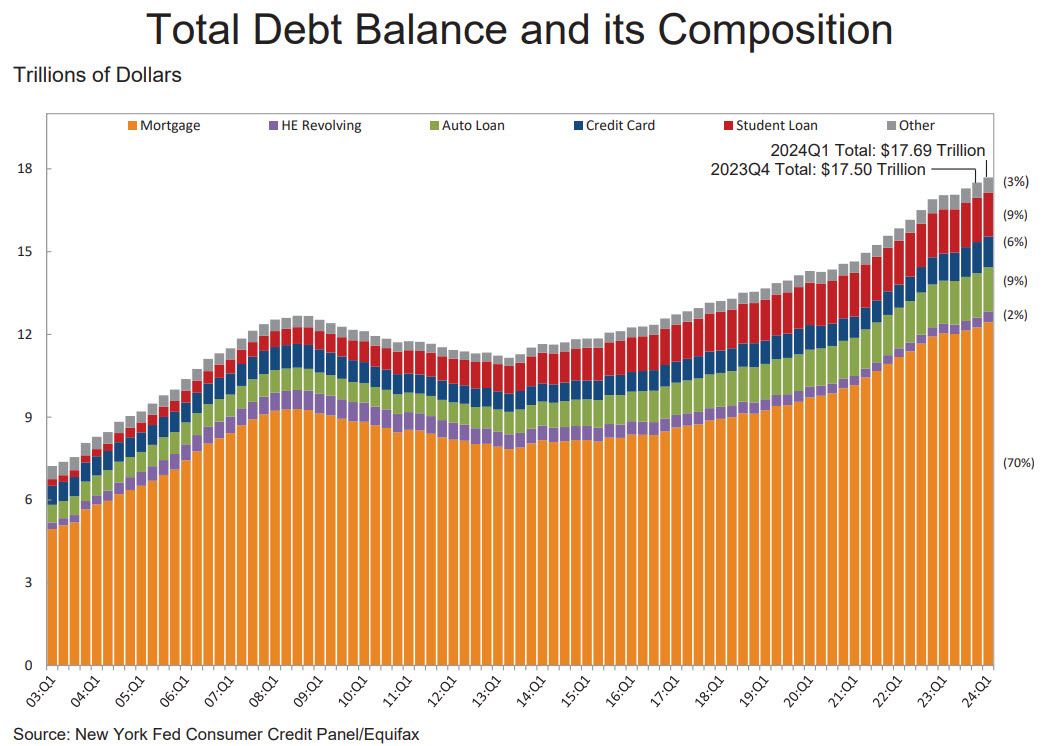

Keep in mind that the economic category of “credit card debt” does not factor the recent upswing in “buy now, pay later” and other forms of phantom debt (because those lenders don’t report their numbers). That means the total household debt figure referenced above is probably a bit misleading. There are also other types of loans to keep track of besides credit cards. LOTS of them…

For example: Since Biden took office, it looks as though an increasing number of homeowners could be resorting to home-equity line-of-credit (HELOC) loans, called “HE Revolving” in the chart above. They’re also doing so at the currently-higher interest rates, just to stay afloat…

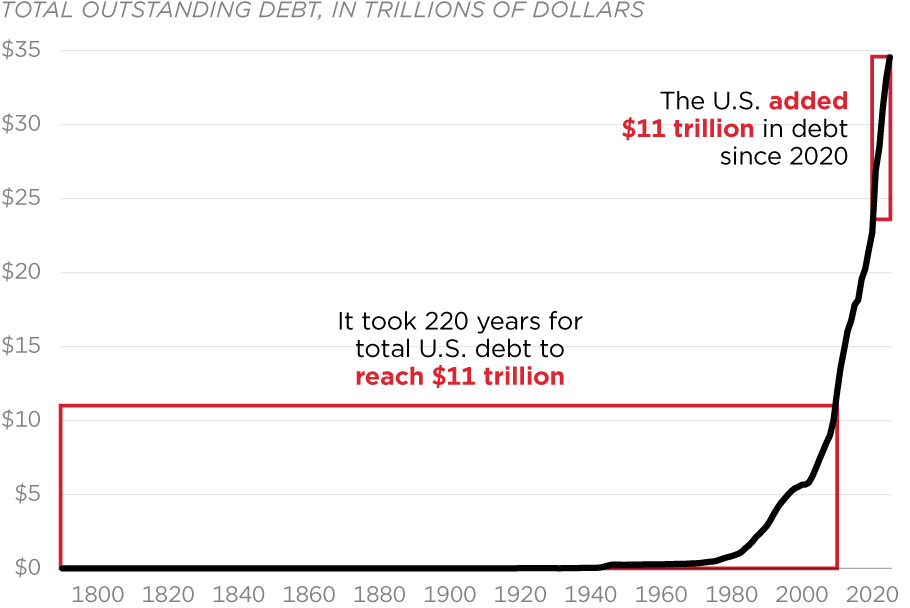

See, nobody wants to sell their old house and move into a new home when their mortgage rate would double or triple! So, once again, Americans are turning their homes into piggy banks. Despite today’s average rate of 9.31% – 12.16% on those loans! It’s still less than credit card companies are charging… You’d think, considering record levels of consumer debt, that spending would slow down. That’s not happening either. This matters because the Fed’s interest rate hikes are intended to slow consumption. If households just keep spending, the economy doesn’t “cool” and prices just keep going up. In a sense, the American family and the Federal Reserve are locked in an arm-wrestling match. That never ends well – but they aren’t the only parties at the table… Families vs. the Federal Reserve vs. the White HouseWe know that consumer spending is still on the rise, with the notable exception of a spending collapse between January 2020 and March 2021. With savings running out, and debt piling up, that could change dramatically. The Fed hopes so – because less demand for goods and services would lower the inflationary pressures in the economy. But the White House is still on a truly historic spending spree… A staggering $11 trillion has been added to the U.S. federal government debt since 2020. You can see that fact reflected on the line graph below:

Cooling off consumer spending isn’t enough! In order to truly get inflation under control, the Fed has to also curb the federal government’s debt addiction. So far, despite the fact that the federal government will spend over $1 trillion on debt service payments this year alone, federal spending isn’t slowing down. The Fed is locked in an armwrestling match not only with American families, but also with the White House. And the Fed has to be careful… If they pull too hard (raising interest rates higher), we’d see another wave of bank failures on par with last year’s. The government’s debt service payments would skyrocket. As far as I can tell, there are only three ways out of this mess:

What’s the best we can hope for? Honestly, it’s hard to say… Although our nation has been in somewhat similar circumstances before, which we endured, this time is different. The U.S. government is nearly $35 trillion in debt, and consumers are buried under $18 trillion in debt (over $1 trillion in credit card debt alone). Could the U.S. dust off the book of Leviticus and enact a debt jubilee, like Jim Rickards and Peter Schiff have predicted? That would solve the debt problem, but it would create a whole bundle of new problems… Who would ever take the dollar seriously as a store of value if your dollars could get zeroed out on a whim? The bottom line appears to be: It'll get much MUCH worse before it gets better, as Brandon Smith warned earlier this month. So what can we do about it? How can we create financial security in such a chaotic economic environment? Diversification beyond debtNot long ago, Ray Dalio, founder of the world’s most successful hedge fund, asked his millions of followers Do You Have Enough Non-Debt Money?

Dalio wants you to understand that, although you think of cash as an asset, it’s really a liability! Inflation is how government pays off outrageous debts. Inflation is the tax nobody voted for and everyone pays – and it’s how governments rob their citizens (and their lenders!) without changing the numbers in their bank accounts. If you don’t want to get robbed, what should you do? Dalio again:

Listen: Dalio is a smart guy. He’s not a permabear or a goldbug – he made the vast majority of his fortune speculating in the most obscure corners of financial markets. He’s not telling you “Sell everything! Buy gold!” It’s a more balanced approach:

Gold is a “good diversifier” because, when financial crisis strikes, gold usually surges in price. Everyone knows it’s a safe haven store of value. Everyone knows gold is the one asset you can trust when the world’s on fire. Physical precious metals like gold and silver have historically provided an inflation-resistant store of value, and they cannot be defaulted on. So you might consider diversifying your savings with the only financial asset that’s always had value for thousands of years. You don’t have to be on Bloomberg’s billionaires index (Dalio is #124) to diversify with real, physical gold and silver. Here at Birch Gold, we make it easy for every American family to diversify their savings with physical precious metals. I hope you’ll take a few minutes to learn more about the benefits of owning physical precious metals. But no matter what you choose to do, make your decision soon. The combination of record demand from central banks and private investors like you have already pushed gold’s price to record levels multiple times this year…

|

Send this article to a friend:

|

|

|