Where We Are in the Big Cycle: On the Brink of a Period of Great Disorder

Ray Dalio

A year and a half ago, when I put out my book Principles for Dealing with the Changing World Order and an animated video of it, I described the five big forces that have driven and are driving just about everything: 1) the credit/debt/market/economic cycle, 2) the internal peace/conflict cycle that shapes the domestic order, 3) the external peace/conflict cycle that shapes the international order, 4) acts of nature (e.g., droughts, floods, and pandemics), and 5) human inventiveness/technology. I explained how these interact together to drive just about everything in what I called the “Big Cycle” and how lessons I learned from studying history led me to believe that we are on a path toward a period of great disorder that includes financial turbulences and great conflicts within and between countries. A year and a half ago, when I put out my book Principles for Dealing with the Changing World Order and an animated video of it, I described the five big forces that have driven and are driving just about everything: 1) the credit/debt/market/economic cycle, 2) the internal peace/conflict cycle that shapes the domestic order, 3) the external peace/conflict cycle that shapes the international order, 4) acts of nature (e.g., droughts, floods, and pandemics), and 5) human inventiveness/technology. I explained how these interact together to drive just about everything in what I called the “Big Cycle” and how lessons I learned from studying history led me to believe that we are on a path toward a period of great disorder that includes financial turbulences and great conflicts within and between countries.

I recently gave a nine-minute speech that provided a quick summary of the Big Cycle and where I believe we are in it. Many people told me it was a good quick overview, so I’m sharing a slightly updated and expanded version of the speech with you here. Over the next few weeks, I will follow this brief overview post with two more postsprovide more in-depth examinations of how the credit/debt/market/economic cycle and the great power conflict force (focusing on the US-China conflict) are unfolding.

Summary of the Big Cycle

Over the last several years, I observed a number of big forces happening in magnitudes that never existed in my lifetime but that had existed in these magnitudes during the 1930-45 period. This drove me to study the rises and declines of reserve currencies and the countries behind them over the last 500 years and the rises and declines of China’s dynasties over the last 2,000 years, which led me to see that the same things happen over and over again for pretty much the same reasons and to make a model of these changes. Based on a) my model for how the “machine” works, b) my measures of where things now stand, and c) the momentum behind these measures, the existing world order is on the brink of three to five painful seismic shifts that, if they happen, will disrupt domestic and world orders in ways that we have never seen in our lifetimes but have happened many times before in history.

The five big forces that have intensified to reach levels that are consistent with past big changes in the world order and are driving just about everything are:

- The creation of enormous amounts of debt bought by central banks via their printing of money and buying the debt (i.e., monetizing debt)—in other words, the government financing itself in a big way by both borrowing a lot and printing a lot of money.

- Big conflicts within countries (now most importantly the US) prompted by the largest wealth and values gaps in our lifetimes, which are leading to the emergence of populists of the left and the right who are fighting with each other.

- Big conflicts between countries arising from the rise of countries (now most importantly China) that are becoming roughly powerful enough to be able to challenge the existing world powers (most importantly the US) and the world order (most importantly the American world order).

- Acts of nature (droughts, floods, and pandemics)—i.e., climate change.

- Technology changes—e.g., the First and Second Industrial Revolution, computing and the internet, AI.

Each force, and most importantly, the combination of them, is now occurring at the largest magnitude since the 1930-45 period and at levels of magnitude similar to those that existed just before prior breakdowns and seismic shifts in domestic and world orders. If you want more detail on how they work and interact with each other, you can find it in my book or animated video.

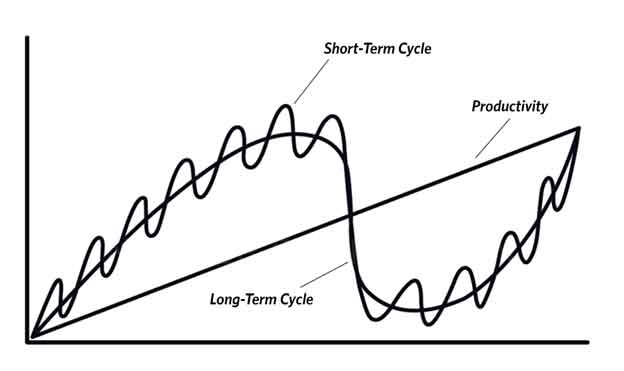

Now, I will review the Big Cycle in brief, show where I believe we are in it, and squint into the future. To me the way the world works looks like this:

The upward sloping line represents the evolutionary advances in knowledge and technologies. Due to these advances, productivity and living standards have improved a lot over time. This is shown in most stats such as real per capita incomes, life expectancies, and levels of nutrition and healthcare. While I showed this evolutionary uptrend as a steady upward sloping line, the rate of learning and advancement varies. As for what is now happening, it is obvious to me and most people who follow such things that the world is at the brink of one of the greatest changes ever, primarily due to advances in AI. Such changes have always had and will certainly have big consequences that are very difficult to accurately anticipate. If managed well, they can yield great productivity advances, and if not managed well, they can add to the turbulence.

The two wavy lines on the chart that are moving around the evolutionary uptrend line represent the two most important cycles. The wavier line represents the short-term debt cycle that in the past has lasted about seven years on average give or take about three years, and the bigger one represents the long-term debt cycle that has lasted about 75 years on average give or take about 50 years. These financial/economic changes have been accompanied by political changes within countries and geopolitical changes between countries.

More specifically, the smaller, short-term cycle represented by the wavier line is primarily due to the short-term credit/debt/market/economic cycle (also known as the business cycle) and the political changes that accompany it. It is the cycle that consists of periods of 1) economic weakness and falling inflation that we call recessions that lead to 2) central banks stimulating credit growth and economic growth that eventually lead to 3) inflation that leads to 4) central banks tightening money and credit that causes 5) credit/debt/market/economic problems that lead to recessions. We are now in the tight money to fight inflation phase of this cycle, just before the economic contraction that is likely to make the next year or two difficult ones in the economy. The short-term political cycle moves loosely in sync with the short-term credit/debt/market/economic cycle. As for where these cycles are headed, the financial/economic one is likely headed into a period of weakness, and the political one is headed into election cycle years, most importantly 2024 in the United States and Taiwan, because these elections will likely be turbulent and defining ones.

Throughout history these short-term cycles have accumulated into big long-term cycles (lasting 75 years on average give or take 50 years) in which 1) debt assets and debt liabilities rose to amounts that were unsustainable, which necessitated big financial/economic restructurings and new financial orders, 2) wealth, values, and political gaps rose to levels that were unsustainable, which toppled domestic political orders, and 3) declines of older powerful countries and their orders relative to newer powerful countries and their orders take place. Together, these three forces led to big financial, political, and geopolitical seismic shifts in world orders.

Financially, the seismic shifts always took the form of too-large debts that couldn’t be paid with real money so there was a lot of printing of money and debt problems that led to big debt restructurings via writing down and monetizing debt. In the past, this has typically been accompanied by a broader restructuring of domestic and/or world orders and/or geopolitical shifts. At such times, great domestic political and international geopolitical shifts have also typically occurred as the economic problems, the domestic political problems, and the external geopolitical problems made the perfect storm that led to seismic shifts and restructurings of financial, domestic, and world orders. The Big Cycle line plunging in the chart represents the big collapse of the old order leading to the restructuring to create the new order.

Where We Are in the Big Cycle and Where We’re Headed

The last big seismic change in the world order took place in the 1930-45 period of depression and war. Soon after it ended, the new world monetary, political, and geopolitical orders began.

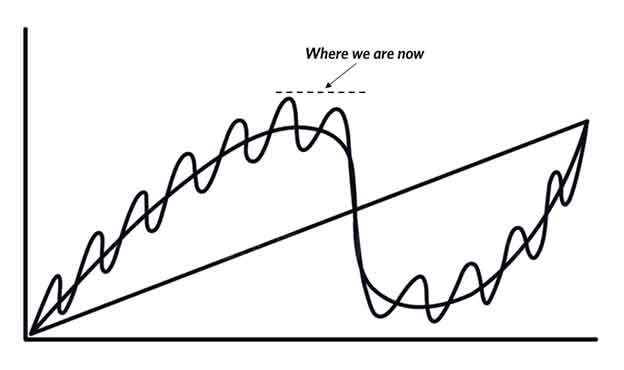

Since 1945 there have been 12 and a half credit/debt/market/economic cycles and associated political cyclical swings. We are now about halfway through the 13th short-term debt cycle. This is when the tightening to fight inflation is causing a cracking in the financial markets and just before there is the economic contraction part of the cycle. Looking at the long-term debt cycle, debt asset and debt liability levels have become unsustainably high via unsound finances, and debts are projected to increase so much that they will have to be bought by central banks (who themselves are close to having negative net worths because of the big losses they have on the debts they already bought). Given these conditions, it appears that interest rates that are high enough (and money and credit that is tight enough) to fight inflation and provide lender-creditors with adequate real returns will be unbearably high for borrower-debtors. This means the system is close to the point where big restructurings will be needed. Of course, which debtors and creditors are affected will vary. I will get into that in more detail in a subsequent post.

As far as the domestic political circumstances go, there has been growing populist extremism in most countries (most importantly the US) and a shrinking middle (that is still the majority). This, as it has been through history, is due to large gaps in wealth and values that are leading a significant percentage of the voting population to want political leaders who will fight and win for them and to reject those who will compromise. By most measures the US is clearly in the late Stage 5 (“When There Are Bad Financial Conditions and Intense Conflict”) part of the internal order cycle explained in pages 167-83 of Principles for Dealing with the Changing World Order, which comes just before some sort of uncontrolled fighting or some form of civil war.

As for what’s ahead, the US will be entering a big election year in which 33 Senate seats, the presidency, and control of the House will be fought over by a number of populist candidates and will probably take place when there are poor economic conditions, so the fights will be vicious. That will be risky. Following rules and compromising, which is required to make democracies work, will be tested. Because populists are so committed to winning at all costs and are unwilling to compromise, more-intense-than-expected battles are more likely. Each one of these forces is a part of the system. For example, the debt ceiling increase will not go as smoothly as most people expect and will likely become a big election issue that will split the country because both sides will fight for victories and will be less willing to compromise. Also, in this election year, aggressiveness with China will intensify because most everyone is anti-China, so those running will want to outdo each other with their China-bashing. Continuing engagement between US and Taiwanese leaders will likely still happen, which, together with the Gallagher House Select Committee on the Chinese Communist Party hearings, will push the US-China conflict closer to the brink (or over the brink). In my upcoming post on China based on what I learned in my recent travels there, I will delve more deeply into these issues.

As for acts of nature, while more of a wild card, they are more likely to be costly and damaging over the next five to ten years as the impacts of climate change intensify.

So four of these five big forces (i.e., the financial one, the internal conflict one, the external conflict one, and the acts of nature one) appear more likely to be painful disrupters to the world order. The fifth one—human inventiveness/technology—is likely to be a big disruptor, though it's difficult to say in what ways.

When these forces come together in the magnitudes that we are now seeing, history has shown that it is likely that we experience seismic shifts in financial orders, domestic orders, and world orders. For these reasons, it appears to me that we are here:

In other words, there is little doubt in my mind that the existing world order is changing rapidly in challenging ways and that people who are living on the assumption that things will work in the orderly ways that they have gotten used to will be shocked and hurt by these changes to come.

In summary, 1) the world is certainly changing and will certainly change dramatically and 2) how well this goes will depend on how well the changes are managed. If the people who have their hands on the levers of power rise above their tendencies to focus on fighting to maximize their own benefits and instead focus on working together to do what is best for the whole and divide the pie well, the financial/economic, domestic political, and international geopolitical orders can change in peaceful ways to create a better world order for most people. Presumably we want that, so we should be strongly against war and in favor of bipartisan pursuit of what is best for most people. However, some will argue that that perspective is too idealistic and that we should be more realistic about what is likely and plan accordingly. I agree that history has shown that the pursuit of self-interest has proven to be a more powerful force than the pursuit of collective interests and that there is a good chance that movement to higher-level thinking and better outcomes is unlikely, so we also should be prepared for the worst. If we are prepared for the worst, we will be fine.

Bridgewater Daily Observations is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, Bridgewater's actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on simulated, hypothetical, or illustrative information that have inherent limitations. Unlike an actual performance record simulated or hypothetical results do not represent actual trading or the actual costs of management and may have under or over compensated for the impact of certain market risk factors. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, Calderwood, CBRE, Inc., CEIC Data Company Ltd., Clarus Financial Technology, Conference Board of Canada, Consensus Economics Inc., Corelogic, Inc., Cornerstone Macro, Dealogic, DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Entis (Axioma Qontigo), EPFR Global, ESG Book, Eurasia Group, Evercore ISI, FactSet Research Systems, The Financial Times Limited, FINRA, GaveKal Research Ltd., Global Financial Data, Inc., Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), The Investment Funds Institute of Canada, ICE Data, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JSTA Advisors, MarketAxess, Medley Global Advisors, Metals Focus Ltd, Moody’s ESG Solutions, MSCI, Inc., National Bureau of Economic Research, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Refinitiv, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Sentix Gmbh, Shanghai Wind Information, Sustainalytics, Swaps Monitor, Totem Macro, Tradeweb, United Nations, US Department of Commerce, Verisk Maplecroft, Visible Alpha, Wells Bay, Wind Financial Information LLC, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability, or use would be contrary to applicable law or regulation, or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction. No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater® Associates, LP.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.

Raymond Thomas Dalio is an American billionaire investor and hedge fund manager, who has served as co-chief investment officer of the world's largest hedge fund, Bridgewater Associates, since 1985. He founded Bridgewater in 1975 in New York.

https://www.linkedin.com/ray-dalio/

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)