Send this article to a friend:

March

23

2026

|

Send this article to a friend: March |

Renewables Aren’t the Problem—Market Design Is

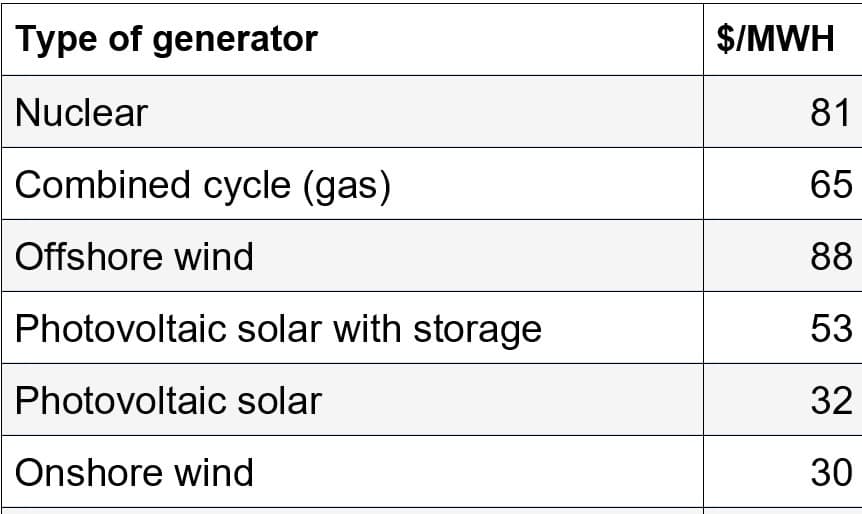

Now, let’s define the issues. First question: Are new renewable projects cheaper providers of electricity than 30-40 year old fossil plants? That’s like comparing the monthly charges on a new car to those on a 20-year-old jalopy with no monthly finance charges (all paid off) and low collision insurance (car has no resale value). Absolutely cheaper to keep the old car until it falls apart. But fuel constitutes at least half the cost of those fossil-fueled units, and some renewable power is cheaper than the fuel costs. So, the answer is “sometimes”. Next, we’re not getting into quasi-religious disputes about the need to reach a 100% green power goal in order to save the world. Shooting for 100% rankles traditionalists, generates opposition and may reduce grid flexibility and raise costs. So why make it an issue? If renewables are as good as their proponents say, they will eventually drive out most of the fossil units, anyway. Patience is a virtue. Unfortunately, the jalopy analogy becomes less and less relevant because the electricity industry has to build new power plants to meet increasing demand, so the next question is: are new renewable plants more economical to own and operate than nuclear or fossil-fueled units? Let’s look at the estimates from two standard sources. The Energy Information Administration (EIA) produced its latest projections in 2025 and published them under the aegis of the Trump administration, so either the Trump people did not notice or they represent a cautious view of the prospects for renewables. The EIA predicts “levelized cost”, meaning the average cost per MWH generated (operating, fuel, and capital costs) over the lives of the plants. Here are the base case projections for selected means of generation coming into service in the next few years: EIA PROJECTIONS

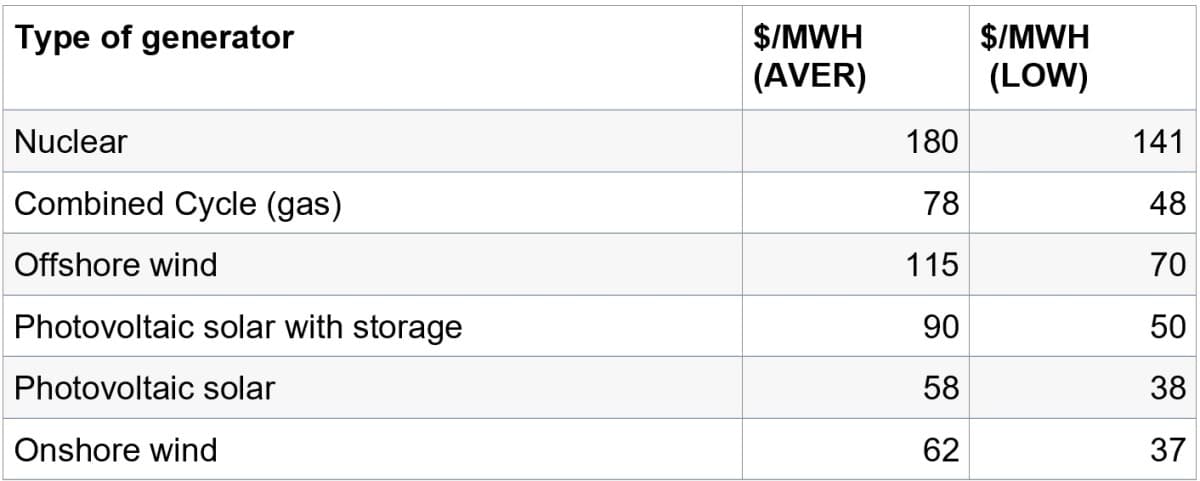

Source: EIA, Levelized Cost of New Generation Resources in the Annual Energy Outlook 2025. Now, you might rightly be skeptical, considering the uncertainty of long-term projections, but consider that much of the equipment for plants that go into operation over the next few years has been ordered, so we should have a reasonable idea about capital costs, which do not change over the life of the plant. But we have a shaky handle on fuel costs over a 30-year lifetime. If gas costs rose 50% over the estimate, that gas-fired generator would produce electricity as expensive as the nuclear plant. If gas costs fell to half of the estimate, the gas generator would be barely competitive with photovoltaic solar with storage and still way above photovoltaic solar and onshore wind. The legendary banking house, Lazard, makes a detailed annual analysis, too. In its 2025 report, it unambiguously stated, “On an unsubsidized … basis, renewable energy remains the most cost-competitive form of generation.” Lazard produces estimate ranges and its methodology differs from the EIA, so pay more attention to the order of ranking than the absolute numbers when comparing to EIA numbers. We show the average estimate and the low end of the range, which we suspect reflects projects most likely to succeed to completion.

Source: Lazard, Levelized Cost of Energy June 2025. Either way, except for offshore wind, renewables are competitive in cost. The competitiveness of gas units depends on the price of gas. Nuclear is so expensive it’s out of the ballpark altogether. Interestingly, Lazard also calculates the cost of community/industrial solar (local solar on rooftops), which at the low end of its range comes surprisingly close to being competitive with utility-scale power. That should scare the legacy utilities. Now for the problem, neither the grid nor its managers have prepared for the new age. Place- specific renewables require a transmission link to consumers. What have the transmission owners and operators been preparing for over the past decades? For more competitive markets and allocation of capacity via financial instruments? Certainly not for an avalanche of renewables and burgeoning demand. As for price to users, the principal markets in the UK and the USA employ an auction that sets the market price based on the price required to bring online the last unit required to fill the demand quota. That unit is, invariably, fueled by natural gas. Meaning that the price of gas sets the price offered to all generators, even if gas generation makes up only a small part of the total. Under those circumstances, the renewable (or nuclear) generators can pocket a big profit thanks to the high price paid to the last gas generator, and the customer gets no benefit from lower renewable costs. Gas sets the price of renewable energy. That market mechanism was designed before renewables amounted to anything. In the UK, where gas fuels much of the generation, the country has put off construction of sufficient gas storage facilities, so gas price and supply are at risk from foreign events, such as a war in the Persian Gulf. In short, don’t fix the affordability problem by getting rid of the cheapest generation options. Focus on market structure and the grid, instead. And, no, we don’t know why Bill Gates plans to build a nuclear power plant in Wyoming. Maybe he has money to spare. By Leonard Hyman and William Tilles for Oilprice.com

Leonard S. Hyman is an economist and financial analyst specializing in the energy sector. He headed utility equity research at a major brokerage house and has provided advice on industry organization, regulation, privatization, risk management and finance to investment bankers, governments and private firms, including one effort to place nuclear fusion reactors on the moon. He is a Chartered Financial Analyst and author, co-author or editor of six books including America’s Electric Utilities: Past, Present and Future and Energy Risk Management: A Primer for the Utility Industry.

William I. Tilles is a senior industry advisor and speaker on energy and finance. After starting his career at a bond rating agency, he turned to equities and headed utility equity research at two major brokerage houses and then became a portfolio manager investing in long/short global utility equities. For a time he ran the largest long/short utilities equity book in the world. Before going into finance, Mr. Tilles taught political science .

oilprice.com |

Send this article to a friend:

|

|

|