Send this article to a friend:

March

06

2024

|

Send this article to a friend: March |

|

| Income Needed To Afford A Home In The US Has Soared By 80% Since 2020

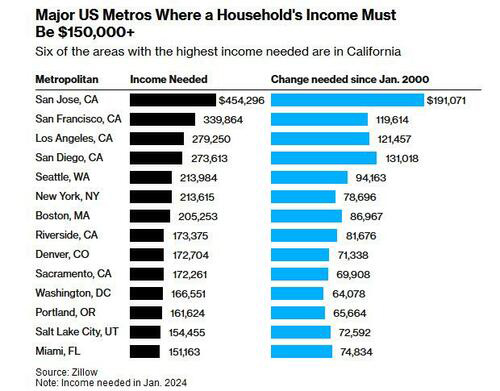

And yet, for all the seasonal adjustments, data rigging, propaganda and angry outbursts by the senile president, there may be a very simple reason why Biden will lose the Nov 2024 election not just on the catastrophic debacles that are immigration and foreign policy (Afghanistan, Ukraine, Israel), but also on the economy, and that has to do with the snuffing of what was once the American dream - namely, owning a house. According to Zillow, the income needed to comfortably afford a home in the US has leapt 80% since 2020, far exceeding what the BLS reports has been a 23% increase in median household income over the same period. The real estate website found home buyers today need to make more than $106,000 a year, up $47,000 from 2020, a change driven largely by higher prices and borrowing costs. "Housing costs have soared over the past four years as drastic hikes in home prices, mortgage rates and rent growth far outpaced wage gains," said Orphe Divounguy, a senior economist at Zillow. Some math: in 2020, a household earning $59,000 a year could comfortably afford the monthly mortgage on a typical US home, assuming the rule of thumb that a buyer can spend up to 30% of their income on housing and make a 10% down payment. That was less than the US median income of about $66,000 at the time, meaning more than half of American households had the financial means to afford homeownership. Fast forward just four years to today, when it takes roughly $106,500 in income to afford a typical home, and median earnings are about $81,000, putting a home purchase out of reach for most families. In 14 large housing markets, led by a handful of cities in California, Zillow estimated that household income must be $150,000 or more to comfortably afford a typical home. Among the 50 largest metropolitan areas studied, only Pittsburgh still had an income threshold for affordability below the $59,000 national average from 2020.

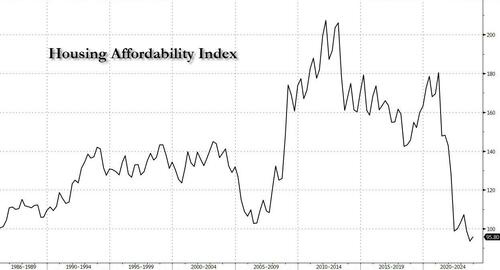

If that sounds vaguely similar to saying that US housing has never been more unaffordable, that's because it's the exact same thing: as the following index of Housing (un)affordability from the NAR shows, housing has never been more unaffordable.

If that wasn't enough, a model created by the Atlanta Fed shows that US homes fell below an affordability threshold in May 2021 and have remained there since. The Fed’s Home Ownership Affordability Monitor Index measures the ability of a median-income household to absorb the estimated annual costs of owning a median-priced home. The model, which incorporates nearly 20 years of data, found houses are in their longest stretch below the threshold since 2009. Going back to the Zillow study, if showed the monthly mortgage payment on a typical home has nearly doubled since January 2020, to $2,188 (assuming a 10% down payment). And while mortgage rates have eased ever so modestly in recent months as investors expected the Fed eserve to begin cutting their benchmark interest rate this year, they have since resumed their upward climb again pushing what littler housing was affordable for an instant, back into the stratosphere. And so for those wondering why Biden can't get a favorable vote for his handling of the economy even from democrats, the answer is simple: the administration successfully converted what was once the American dream into an American nightmare.

|

Send this article to a friend:

|

|

|

The Biden administration and its fawning PR industry, also known as the mainstream media, have over the past year been desperate to explain to ordinary deplorables Americans why the US economy is ackchyually doing "so much better" than most peasants give the 81-year-old's handlers credit for (see "

The Biden administration and its fawning PR industry, also known as the mainstream media, have over the past year been desperate to explain to ordinary deplorables Americans why the US economy is ackchyually doing "so much better" than most peasants give the 81-year-old's handlers credit for (see "