| The End of Safe Banking: What You Need to Know Now

Peter Reagan

After several major bank failures that ended the first quarter of last year, regulators are supposedly seeking to minimize the odds of another banking crisis. After several major bank failures that ended the first quarter of last year, regulators are supposedly seeking to minimize the odds of another banking crisis.

(Hint: They weren’t very successful preventing what happened last year, the Fed’s cure ended up being worse than the disease.)

Their proposal currently goes by the name of Basel III, and it aims to force banks to set aside enough cash to handle major losses:

U.S. regulators are expected to significantly reduce the extra capital banks must hold under a proposed rule that has drawn aggressive pushback from Wall Street, said eight industry executives in regular contact with the agencies and regulatory officials.

Bank regulators led by the Federal Reserve in July unveiled the “Basel III” proposal to overhaul how banks with more than $100 billion in assets calculate the cash they must set aside to absorb potential losses.

But according to some bank executives, banks don’t want to comply with the Basel III regulations, because they say they can’t afford it:

Banks have loudly complained about the proposal, which overhauls how banks gauge their risk and require them to set aside more capital. Industry executives said the draft rules would force them to raise costs and potentially curb lending.

Michael Barr, the Fed’s vice chair for supervision, attempted to rebut those views with what turned out to be a disturbing comment: “If the proposal is adopted, the average loan would only see a cost increase of 0.03%, assuming banks passed all the new lending costs on to the borrower.”

Now, 0.03% is not very much! Even if banks passed along 100% of the costs to customers, that makes a $10,000 transaction cost $3 more.

So what’s the big deal?

Amazingly, this Basel III proposal highlights 3 much more urgent issues with the U.S. banking system. They legitimately might not be able to afford an extra $3…

#1: A brief overview of bank reserves reveals a BIG problem

Trying to thoroughly explain bank reserves without writing an 800-page textbook can be a complicated situation.

With that in mind, let’s try a simplified overview from 30,000 feet. There are two basic components to bank reserves:

- The reserves which are liquid, like cash or cash equivalents.

- The capital which includes all assets that could be turned into cash. Everything from buildings to the photocopier in the CEO’s office (and everything in between).

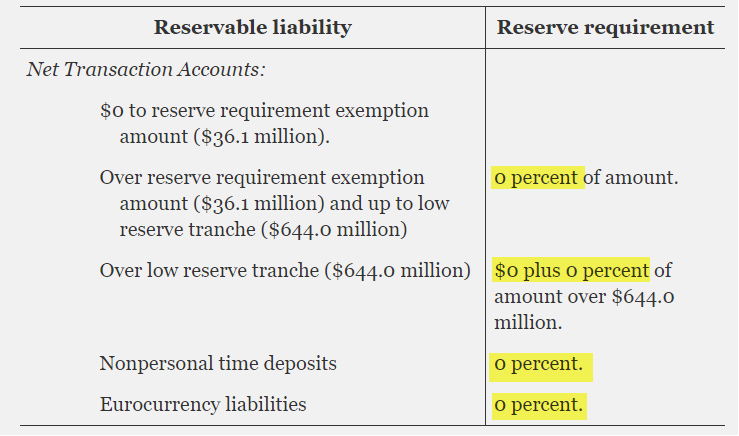

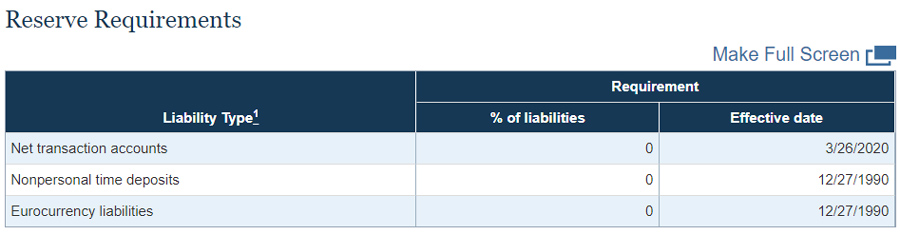

You might be surprised to learn that U.S. banks are not currently required to have liquid cash reserves at all. You can see this reflected on the table below (source):

That’s a bit unexpected, isn’t it?

Here’s a quote from the Federal Register that confirms banks do not have to keep liquid cash reserves on hand:

…a zero percent reserve requirement ratio shall apply at each depository institution to total reservable liabilities that do not exceed a certain amount, known as the reserve requirement exemption amount.

That’s right, ZERO!

According to the “stress test” section of the Fed website, DO need to have some 7-8% capital reserves:

- a minimum CET1 capital ratio requirement of 5 percent, which is the same for each bank;

- the stress capital buffer (SCB) requirement, which is determined from the supervisory stress test results and is at least 2.5 percent; and

- if applicable, a capital surcharge for global systemically important banks (G-SIBs), which is at least 1.0 percent.

(Don’t worry about the complex language being used to describe each requirement, the important part is that the total capitalization requirement adds up to 8%.)

What does this mean?

On net:

- Banks need liquid reserves of $0 for every $1 they lend

- Banks can lend about $12.50 in credit for every $1 in assets they own

This arrangement means banks are offering huge amounts of credit based on their assets. During good times, that means they’re able to make a lot of profit.

During less good times, this arrangement looks more like an elaborate suicide pact. For every dollar of bank assets, they have twelve debtors – if a single one doesn’t pay them back, they lose.

What’s even more shocking is how underwater many banks already are…

#2: Banks are already sitting on HUGE losses

What happens to a bank that makes $12.50 in loans on $1 in capital, then the value of their capital declines?

That’s called an “unrealized loss” (unrealized because the bank doesn’t have to tell anyone about it, so long as the $12.50 in loans gets paid back).

Which is very much the case right now, according to the FDIC:

That’s some $675 billion in unrealized losses.

Let’s do some math… If banks only loaned half as much as they’re legally allowed to, $6.25 for every dollar, those $675 billion in losses are the basis for $4.2 trillion in loans.

Well, in order to make up for that, banks need to attract assets – which is one of the main reasons savings account rates have been going up. Banks really need your money…

But according to that same FDIC report, they aren’t getting it:

Total deposits of $18.6 trillion fell by $90.4 billion (0.5 percent) from the previous quarter, on par with the decline reported in the second quarter. This was the sixth consecutive quarter that the industry reported a lower level of total deposits.

So it’s quite obvious that overall, banks are struggling. Their loans are undercapitalized and they aren’t luring in enough customer deposits to make up the difference (in fact, they’re steadily losing deposits). Those unrealized losses have to be accounted for, sooner or later.

Now, nobody’s going to say that out loud. Especially bank regulators, or the Federal Reserve.

Their job is to keep you from worrying about the health of the banking system.

As Bloomberg’s Matt Levine said a little over a year ago, one week after the failure of Silicon Valley Bank:

Banking is a confidence trick. You put money in the bank today because you are confident you can take it out tomorrow; to you, a dollar that you have deposited in the bank is just as good – just as much money – as a dollar bill in your wallet. If you show up at the ATM at any time of day or night, you expect it to give you your dollars. But the bank doesn’t just put your dollars in a box and wait for you to take them out; the bank uses its depositors’ money to make loans or buy bonds, and just keeps a little bit around for people who need cash. If everyone asked for their money back tomorrow, the bank wouldn’t have it. But everyone is confident that, if they ask for their money back tomorrow, the bank will have it. So they mostly don’t ask for it, so when they do, the bank does have it. The widespread belief that banks have the money is what makes it true.

This is obvious stuff. Also obvious, and famous, is that it is an unstable equilibrium. If people stop believing it, it stops being true. If everyone stops believing in a bank, they will all rush to get their money out, and the bank won’t have it, and their lack of belief will be retrospectively justified. Whereas if they had kept believing, their belief would also have been justified.

Isn’t this ridiculous?

“Ridiculous” is certainly one word for it…

And while the FDIC and bank regulators tell us, at every opportunity, that the banking system is sound (even though it isn’t) and our deposits are insured (which is usually true), what else are they doing?

Well, they’re quietly laying the ground work to ensure that, when the next bank collapse happens, we won’t have ANY warning…

#3: “Emergency? What emergency?”

If the banking system were in fact robust and stable, why would the Federal Reserve be pushing even healthy banks to borrow emergency funds?

I know what you’re thinking – “How does pushing healthy banks to take loans help out banks that actually need loans?”

It doesn’t. Not directly.

The REAL problem, apparently, is when we find out which banks need emergency funding. Here’s how they plan to keep us in the dark:

…regulators are now eyeing a yearly ‘fire drill’ in which banks would be forced to borrow from the discount window.

There’s a reason healthy banks don’t take emergency loans from the Fed! Tho Bishop explains why:

…taking loans directly from the Federal Reserve, [makes] it easier for distressed banks to do the same. The hesitancy from financial institutions to tap into this source of liquidity is justified. If the public believes a bank needs support from the Fed, it is rational for depositors to flee the bank. The Fed’s explicit aim is to provide cover for at-risk banks, trying to hold off bank runs that are an inherent risk in our modern fractional reserve banking system.

By strong-arming healthy banks to comply, the Fed is escalating moral hazard and leaving customers more vulnerable. They are deliberately trying to remove a signal of institutional risk.

You KNOW there’s trouble when, instead of trying to solve the problem, officials first deny there’s a problem – and THEN start building elaborate smokescreens…

The end result? We’ll have even less warning next time.

What to do when you can’t see a crisis coming

We’ve established that the U.S. banking system is not exactly the model of stability the Fed would have you believe. And that the next crisis will come as an even bigger surprise, thanks to the deliberate decision to create a smokescreen around the Fed’s emergency lending facility.

We already know how catastrophic a bank failure could be. In fact, about the only thing worse for the economy is multiple bank failures.

The main problem with the modern banking system is you never know where your money is… So you can add some certainty and stability to your savings with a tangible asset that’s always in your control: Physical precious metals.

You can start taking action right now to keep your retirement safe, and on a stable foundation. Here’s how…

Having a diversified portfolio with assets known for their protection during uncertain times is a strategic way to reduce risk and build stability into your retirement. Holding alternative assets such as physical gold and silver could add much needed resilience to your retirement savings when the “confidence game” of banking crumbles – whether it happens later this year or later this decade.

Peter Reagan is a financial market strategist at Birch Gold Group. As the Precious Metal IRA Specialists, Birch Gold helps Americans protect their retirement savings with physical gold and silver.

citizenwatchreport.com/

|