Send this article to a friend:

March

11

2024

|

Send this article to a friend: March |

|

| Gold - Catch it if you can

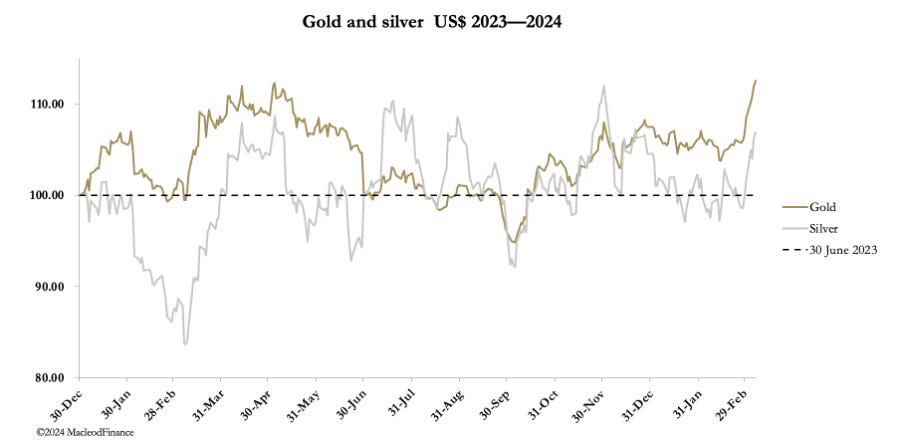

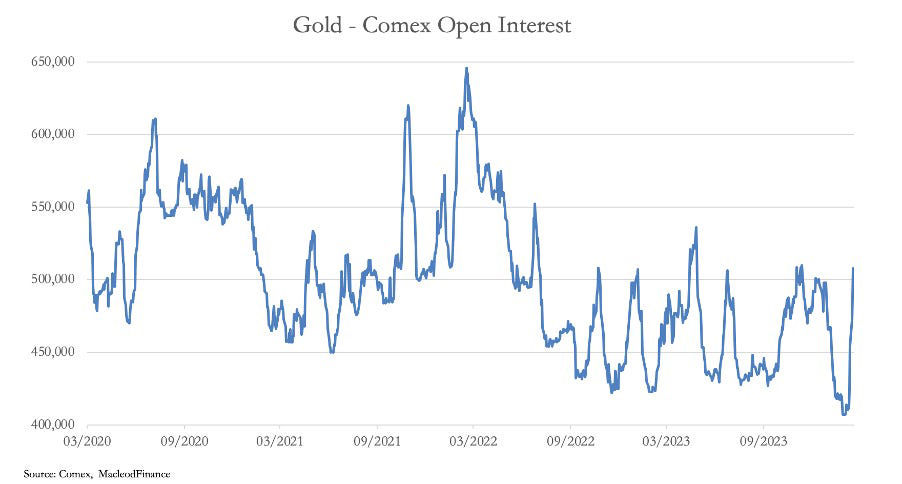

In European trade this morning, gold was $2167, a new record and up $85 from last Friday’s close, while silver at $24.49 was up $1.18. Comex volumes in both contracts were heavy, but the startling increase was in gold’s Open Interest, which has surged by 100,000 contracts since 20 February:

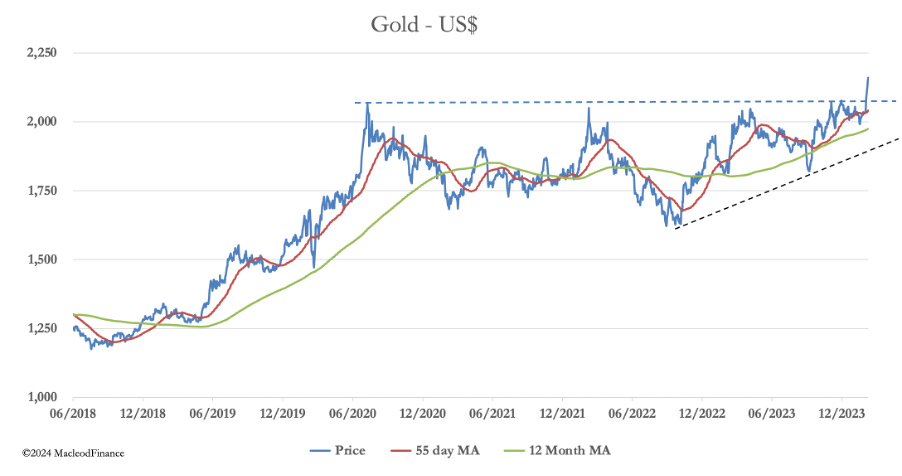

Comex deliveries have also soared. In the four days of this week so far, 1,056 gold contracts have stood for delivery, making the total this year 28,159 contracts (87.58 tonnes). But the more remarkable increase has been in silver contracts: 1,628 this week so far representing 8,140,000 ounces or 253 tonnes. The total for this year to date is 1,122 tonnes. Admittedly, this would take fleets of security vans working 24/7 to handle these quantities if on being stood for delivery this bullion was actually delivered out of the vaults. Instead, it represents change of ownership rather than actual deliveries, but it is an indication of the stress on bullion bank liquidity which must be being badly squeezed, not just on Comex but in London as well. The bullion establishment in western capital markets has been caught badly short. The squeeze is global, which is why when the charts say “buy gold” as they now do the effect has been dramatic. After a 43-month consolidation, breaking into new high ground was bound to be a major event. The next chart shows the technical position.

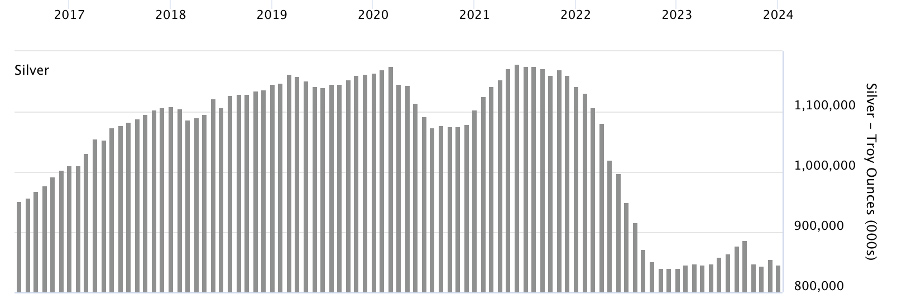

This is as powerful as it gets, capable of supporting a run of several hundred dollars higher. And Elliott Wave technicians will be positively drooling over the bullish potential. Silver supplies limited With a price ratio of 88 ounces to one of gold, silver appears to be particularly oversold. Industrial demand for it has soared in recent years, eating into the balance of stocks held as investment. The deterioration of the liquidity pool is illustrated by the decline in LMBA vaulted stocks since 2022.

And now there appears to be a run on Comex deliveries. So what is it all about? Long-time readers of this column will know it’s less about gold going up and more about currencies going down, a pattern established when the Bretton Woods Agreement was suspended in 1971. It now appears that the dollar is faltering as the following charts show. The first chart is of the dollar index, and the second is the yield on the 10-year Treasury Note.

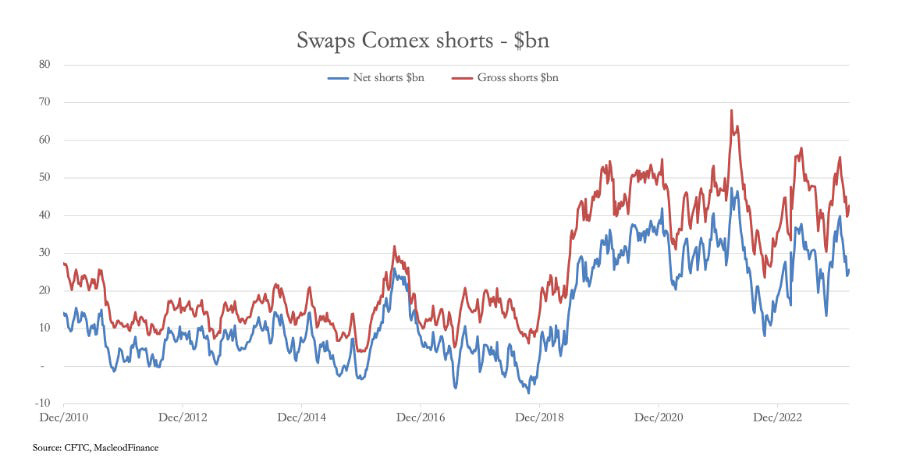

The TWI indicates that the tide has turned against the dollar measured against other currencies, and the declining T-note yield signals that markets expect a greater emphasis on funding the Treasury’s deficit than controlling inflation. Keynesian-trained traders believe that lower bond yields are good for gold and have been caught underweight, or even outright short of their pet rock. The next chart shows the position of Comex Swaps (aka bullion bank traders) on 27 February, adjusted for today’s gold price.

They have found it impossible to get their short positions down to the pre-2018 levels, because the miners are no longer hedging forward production. Since the last Commitment of Traders report, Open Interest has increased nearly 100,000 contracts, most of the short-side burden falling on their shoulders. Which brings us to systemic risk. The possibility of a bullion bank failure should not be dismissed lightly if the gold price continues to rise steeply. Unlike the last real squeeze on them in late-2000, this time the miners are not hedging their output and the squeeze is entirely on the financial establishment’s shorts. Subscribe to MacleodFinance SubstackHundreds of paid subscribers Dedicated to explaining why gold is money and the rest is credit. Dedicated to explaining economics relevant to the preservation of wealth. And dedicated to explaining geopolitical developments relevant to investors.

|

Send this article to a friend:

|

|

|