Send this article to a friend:

February

28

2024

|

Send this article to a friend: February |

|

Understanding the Difference Between Credit and Real Money

Most people probably think that credit evolved after money in the form of coin, but that is incorrect. Credit existed long before, defined in the value of deliverable goods. A thousand years before Rome’s Twelve Tables, the Phoenicians traded throughout the Mediterranean and even as far as Cornwall, where they procured valuable tin. The Phoenicians would have had the same problems faced by businesses today. In order to undertake their trading ventures, they required credit, because they faced expenses before they returned from their voyages many months later with vendible products. As Demosthenes, the Greek orator and statesman, contemporary of Philip of Macedonia and his son Alexander at the same time as Rome promulgated the Twelve Tables put it:

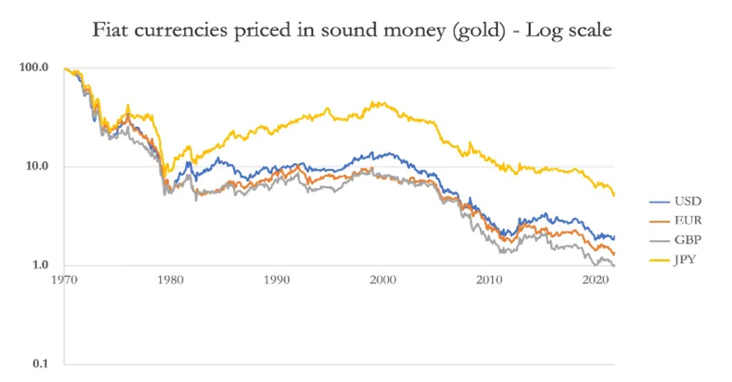

Perhaps even more so today, we rely on credit for every aspect of our lives. Legal money is hardly ever used — today never in the major advanced economies. But even in the past, it was subject to Gresham’s Law, hoarded and not spent. Credit is synonymous with debt. It’s not just that we have banknotes and token coins (representative credit), and bank accounts (credit whether you are a depositor or borrower). But when you employ a workman, you enter into an obligation to pay him, which is your debt for which he allows you a matching credit until you discharge the obligation with another credit, either in the form of banknotes or a transfer of your credit at a bank to a credit at his bank. Alternatively, you might buy an airline or rail ticket in advance. You pay with your credit at your bank and the airline or rail company credits you with an obligation to provide a service at a future date. If you promise your son that you will pay his university fees and give him an allowance, you are entering into an obligation, the promise of credits to cover his or her future debt obligations for as long as he attends the university. Every transaction, every promise, every guarantee, involves incorporeal credit with matching debt obligations. Demosthenes certainly had a point. The distinction between corporeal money and incorporeal credit is that the former exists physically (it has a corpus), and the latter is always created between consenting parties. The commentators who argue that bank credit should be banned appear to be unaware of the true extent of credit in the economy, and the inequity and futility of banning dealers in credit, which is the function of a commercial bank. Not only would nearly all trade cease, but a police state of the most draconian sort would be required to enforce it. And the monetarists who believe that money supply statistics define all the circulating media when they are just the tip of a far larger credit iceberg are also in error. But debt and credit must take its value from something. At one level, it takes its value from a promise to deliver something else — a corporeal, immaterial, or other incorporeal property. But that assumes the purchasing power of credit is anchored against something else. In history, the value-anchor was always a corporeal entity such as gold. Instead, today it is anchored to another incorporeal asset — central bank credit, or banknotes. In other words, the entire structure of national credit hinges on the government’s credibility as issuer of currency obligations.Furthermore, each jurisdiction has credit values which refer to different currencies, diverse incorporeal liabilities in the form of central bank banknotes. A common corporeal gold standard is replaced by potentially incorporeal chaos. While the potential for chaos in credit values now exists, credit based on government credibility can function for a considerable time. But we must recognise that the politicians have high demands placed upon them which inevitably leads them to debauch the currency as a means of surreptitiously transferring wealth from the citizenry to the government so that it can discharge its obligations. In the last eighty years, they have even made a virtue of it, claiming variously that the quantity of credit should be expanded to stimulate economic activity, to ensure prices rise at a two per cent rate to bring forward consumption, and to artificially cheapen borrowings at the expense of savers. Slowly but surely, the inflationists have descended into the economics of unreason. The effect on credit’s purchasing power relative to gold is illustrated in the chart below, which is of the major currencies’ purchasing power relative to gold, since the last vestiges of the link was abandoned by suspending the Bretton Woods agreement.

Since 1971, the dollar has lost 98% of its value relative to gold, and sterling has lost 99%. These currency debasements are measures of the loss of the value of subordinate credit so far under a fiat currency regime. Every transaction, every promise of a transaction, and every commitment to a future transaction has been devalued and will continue to be devalued so long as credit remains detached from corporeal money, which is gold.

|

Send this article to a friend:

|

|

|

Due to its abuse pariculaly by governments, it is credit which presents the greatest risk to our finances today. To appreciate why this is so requires an understanding of what credit represents, and how it differs from real money, which is physical gold without counterparty risk. Credit is always matched by debt: your financial asset is always someone else’s obligation. The collapse of credit’s value happens when a currency (which is also credit) is not attached by exchangeability to gold. That is the danger facing the entire dollar-based financial system today, now that we see the US dollar is ensnared in the US Government’s debt trap

Due to its abuse pariculaly by governments, it is credit which presents the greatest risk to our finances today. To appreciate why this is so requires an understanding of what credit represents, and how it differs from real money, which is physical gold without counterparty risk. Credit is always matched by debt: your financial asset is always someone else’s obligation. The collapse of credit’s value happens when a currency (which is also credit) is not attached by exchangeability to gold. That is the danger facing the entire dollar-based financial system today, now that we see the US dollar is ensnared in the US Government’s debt trap