Send this article to a friend:

February

11

2023

|

Send this article to a friend: February |

|

American Families Are Getting Increasingly Desperate

Usually, during times like these only the poor and lower-middle classes take the brunt of the economic impacts. But quite a bit has changed, especially since the first two quarters of negative GDP growth last year. Now, even those fortunate enough to earn a six-figure income are struggling:

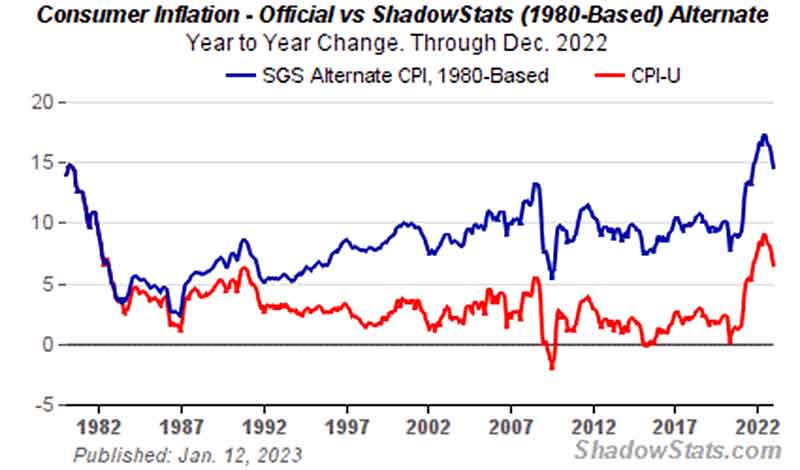

The “New Reality Check” study also revealed another interesting tidbit. Of the 73% of Americans living paycheck-to-paycheck who face difficulty just paying their bills “cite inflation as the reason they expect a worse financial situation in the next year.” Of course, for anyone paying close attention to their bank balance instead of the media spin, those are not surprising findings. You probably don’t need a reminder, but just in case, let’s look at inflation over the last two years. The red line, the official consumer price index for all urban consumers from the Bureau of Labor Statistics (BLS), has been tweaked over time to what analyst Wolf Richter calls the “lowest lowball inflation measure.” (It’s in the government’s best interests to keep official inflation reports low – because that’s how Social Security cost-of-living adjustments (COLAs) are calculated.) Officially, inflation cost us 6.5% of our spending power over the last year. However, if we use the more realistic, less “managed” method of measuring our rising costs as we did back in the 1980s, it looks like we lost nearly 15% of our spending power over the last twelve months.

via John Williams at ShadowStats.com What about pay? Well, average worker pay rose 4.4% in the last twelve months. So most of us working for a living are losing ground – at either 2.1% or over 10% depending on how you run the numbers. In my own personal experience, the 10% number reflects reality more accurately. (A friend of mine on the East Coast shared this story recently – you now need three full-time minimum wage jobs to afford a one-bedroom Boston apartment.) And that’s for those of us in the workforce! The “six-figure income,” which for decades represented a solid, upper-middle-class lifestyle, just isn’t cutting it anymore. Over half of the workers who’ve struggled for years to finally add another digit to their annual pay are still living paycheck to paycheck! That’s astonishing. What’s even more astonishing, though, is what they’re doing to pay the bills… Skyrocketing mortgage refinancing, credit cards filling the gap There’s a phrase that was thrown around a lot in the years leading up to the Great Financial Crisis – “using homes as ATMs.” That’s how media described the process of refinancing a mortgage to convert home equity into ready cash. Usually that’s also associated with locking in a lower rate on the mortgage. (Otherwise, it’s a losing strategy – right?) According to Wolf Richter, a growing number of people are so desperate for cash they’re using their homes as ATMs, even though that means a higher mortgage rate:

You don’t have to have an economics degree to understand that this type of behavior is extremely risky. Now, I don’t think these folks are necessarily foolish – rather I think they’re desperate, and are willing to make this costly bargain in the hope that their situation will improve in the long run. I hope they’re right. What about people who don’t have a mortgage to tap for equity? Well, they’re paying their bills with credit cards:

Yikes! What about those of us who aren’t struggling to pay the bills? Well, inflation is costing us, too… Kevin O’Leary reminds us that, right now, “cash is trash” Those fortunate Americans who have some spare cash lying around might think it’s a good idea to save it for the proverbial rainy day. Traditionally, that means putting cash aside in a savings account. Shark Tank’s Mr. Wonderful, Kevin O’Leary, wants to make sure you know this:

That’s what we mean when we say “inflation robs you of your wealth, permanently.” I hope you aren’t struggling with your bills. I hope you’re not tapping home equity or credit cards to make ends meet. And if you aren’t, here’s why stories like this matter to you, too…

I’ll leave aside the White House responses in times like these, but remember, increases in government spending are highly inflationary. Regardless of your current level of financial security, it makes sense to look for inflation-resistant investments especially for your long-term retirement savings. Plan for your retirement in tomorrow’s dollars Inflation is known as the “tax that no one votes for” because it robs you of your wealth – permanently – without an act of Congress or a President’s signature. Most people pay more attention to the number of dollars they have than what those dollars can buy them. The best way to make sure you’re prepared for an uncertain future is to diversify your hard-earned savings with inflation-resistant investments. They help preserve today’s buying power over the long haul. Physical precious metals, especially gold and silver, are two inflation-resistant investments that have the longest track record as safe-haven stores of value. Many Birch Gold customers call us because they’re worried about the long-term preservation of their savings. They’re tired of the stock market roller coaster and want to get off. I can’t blame them! If diversifying your long-term savings with physical precious metals sounds like a good idea to you, it’s easy to take a few minutes and learn more here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)