What Happens When Soaring Prices Collide With Tapped-Out Consumers?

John Rubino

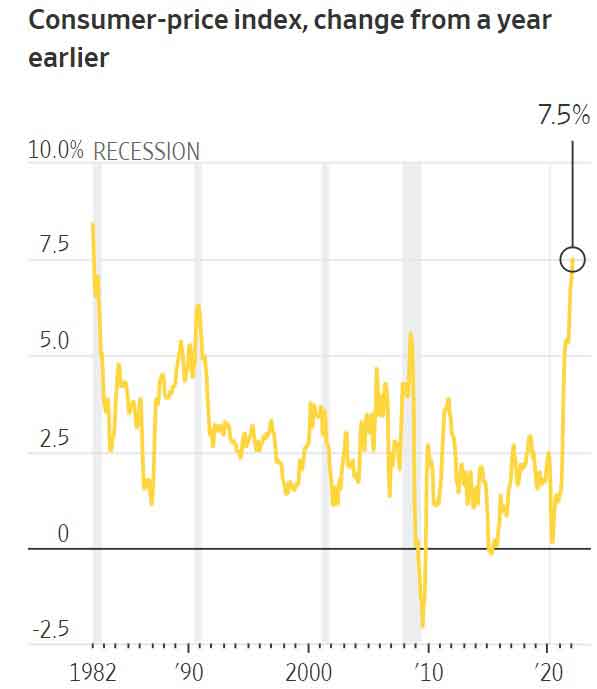

Today’s inflation report was, by any measure, horrific. 7% in a country where 2% was, until recently, the upper end of the government’s target range, pretty much guarantees some kind of aggressive response from the Fed (or the bond or currency markets or all of the above). Today’s inflation report was, by any measure, horrific. 7% in a country where 2% was, until recently, the upper end of the government’s target range, pretty much guarantees some kind of aggressive response from the Fed (or the bond or currency markets or all of the above).

Here’s the Wall Street Journal’s take on the situation. See if you can spot the flaw in its reasoning:

Kathy Bostjancic, chief U.S. financial economist at Oxford Economics, said what started as pandemic-specific inflation has now “broadened out across many, many categories both on the goods side of the economy and on the services side.”

“It reflects supply constraints both in the goods market and the labor market but it also is a function of still strong demand, particularly from U.S. consumers,” she added.

On a monthly basis, the CPI increased a seasonally adjusted 0.6% last month, holding steady at the same pace as in December.

Used-car prices continued to drive overall inflation, rising 40.5% in January from a year ago. However, prices for used cars moderated on a month-to-month basis, a possible sign that a major source of inflationary pressure over the past year could be easing.

Food prices surged 7%, the sharpest rise since 1981. Restaurant prices rose by the most since the early 1980s, pushed up by an 8% jump in fast-food prices from a year earlier. Grocery prices increased 7.4%, as meat and egg prices continued to climb at double-digit rates.

Energy prices rose 27%, easing from November’s peak of 33.3%, but a jump in electricity costs was particularly sharp when compared with historical trends.

Higher prices are putting pressure on consumers, with inflation adding as much as $250 a month to living expenses, and businesses, which are scrambling to keep up with rising materials and labor costs.

Here’s the flaw:

“… it also is a function of still strong demand, particularly from U.S. consumers.”

If this economy depends on robust consumer spending, then the growth inflection point has already passed. From MarketWatch:

Consumer borrowing rose at a 5.4% annual rate in December, down from a revised 10.7% gain in the prior month, which was the largest gain since July 2011.

Key data: Revolving credit, like credit cards, rose at a 2.4% rate in December after a 22.8% gain in the prior month. The November gain was the largest since April 1998.

Nonrevolving credit, typically auto and student loans, rose 6% after a 7% growth rate in November. This category of credit is much less volatile.

The data does not include mortgage loans, which is the largest category of household debt.

Big picture: After paying down debt in 2020, consumers resumed borrowing last year, with credit rising by 5.9% to $4.4 trillion. That’s the largest increase in five years.

The upshot: Inflation is definitely raging. But US consumers have burned through their stimmy checks and are now furiously maxxing out their credit cards to pay for all those suddenly-way-more-expensive necessities. A life financed with credit cards is inherently a short-term affair, and the end is rapidly approaching.

So it’s entirely possible that by mid-year the big story will be not soaring inflation, but crashing consumer spending. And the Fed will be reacting not with “shock and awe” interest rate hikes but equally dramatic cuts.

DollarCollapse.com is managed by John Rubino, co-author, with James Turk, of The Money Bubble (DollarCollapse Press, 2014) andÊThe Collapse of the Dollar and How to Profit From It (Doubleday, 2007), and author of Clean Money: Picking Winners in the Green-Tech Boom (Wiley, 2008), How to Profit from the Coming Real Estate Bust (Rodale, 2003) and Main Street, Not Wall Street (Morrow, 1998). After earning a Finance MBA from New York University, he spent the 1980s on Wall Street, as a Eurodollar trader, equity analyst and junk bond analyst. During the 1990s he was a featured columnist with TheStreet.com and a frequent contributor to Individual Investor, Online Investor, and Consumers Digest, among many other publications. He currently writes for CFA Magazine.

dollarcollapse.com

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)