Send this article to a friend:

January

09

2024

|

Send this article to a friend: January |

|

Mission Accomplished: Yellen Says Fed's Battle is Over!

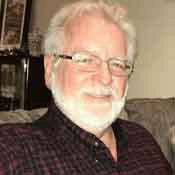

Janet Yellen coos that the Fed has landed so softly we didn’t even feel the wheels touch the tarmac. It’s “mission accomplished,” according to Jesse Felder’s take on Yellen’s praise for the Powell landing. Apparently inflation has been tamed now with no significant damage to labor and no recession. Time to stop worrying about the economy or inflation. Oh, and she probably added another, “There will never be another financial crisis in my lifetime” for good measure as she is want to do. Global freight, however, didn’t get Yellen’s memo, surging 60% last week with more freight-rate hikes to be delivered this week. So, likely more inflation coming down the road. And, while GDP supports Yammering Yellen, the Druckenmiller Recession Proxy keeps screaming recession:

Which is an odd place for stocks to be priced to perfection, but investors probably prefer to listen to Yellen than Druck. For a time with no recession, these days sure are turning in record business bankruptcies:

And that can actually increase inflation, too:

Now, you might think bankruptcies aren’t that far above normal so far, but most companies, especially if they are not publicly traded companies, are hiding their pain, so you don’t know how many more are coming until the arrive:

These kinds of measures are why I am not predicting a recession for 2024. I’m saying we are already in one! As Yellen smiles with glee over the sound shape we are in, she might consider that the commercial real-estate market is already a disaster, even if it is hasn’t taken down anymore banks.

Their plight has been made impossible by the Fed’s rate hikes, and the Fed has made clear there are no cuts on the near horizon.

And it is not like we’ve mostly weathered through this now. Even if the Fed were to start lowering rates this summer, the lag time for the economy to feel the benefit from that loosening of credit is another year or more beyond that point. So, how many of these landlords can survive that long?

So, we have a lot more dead wood to burn up in bankruptcies for many months ahead. It might be a little soon and cavalier for the glee team to be singing about soft landings. If the battle is behind us, and the landing has been stuck—softly stuck—why are so many banks back to running to the Fed’s latest bailout program for funding?

Looks like trouble beneath the surface to me. When I see a lot of smoke curling out from under a door, I assume trouble. Could just be, of course, Janet and Jerome are in their smoking Cubans. Let’s just hope it’s not due to banks carrying a lot of commercial real-estate loans or dealing with those business bankruptcies. Better hope it’s just J&J enjoying the soft landing up in the pilot’s airport lounge. Lots of time left, though, for the growing economic and financial strains to keep popping and cracking until the breaks become visible—sort of like a 737 that has had a depressurization light flickering on and off once in awhile for a few months, which no one could figure out, then suddenly it just blows a panel out the side of the plane. As Janet relaxes about inflation, I am maintaining my own prediction that inflation rises (and has already shown glints of that). Here is a little realization just in from the sudden “unexpected” rise in European year-on-year inflation that backs that prediction up:

This is something I’ve tried to point out several times – that we need to keep our eyes on month-on-month inflation where small rises have been seen because the base effect on year-on-year inflation is giving those long-term numbers a lot of help in continuing to decline due to months more than half a year ago when inflation was coming down quickly. The base effect will be disappearing about now, so we may start to see YoY inflation rise. Then the fantasy-chasing markets will have a lot of reconciliation to reality to do.

Yeah, those were out of line. So, expect realignment to reality, even if Janet and Jerome are smoking up a storm in the lounge as Janet congratulates him on a great fight. (Headlines today are free for everyone, and the quotes above come from the stories below that appear in boldface. Thank you to those who help make this writing possible.)

The Daily Doom is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

|

Send this article to a friend:

|

|

|