Send this article to a friend:

January

11

2024

|

Send this article to a friend: January |

|

Gold isn’t responding to shifts in US interest rate like it used to

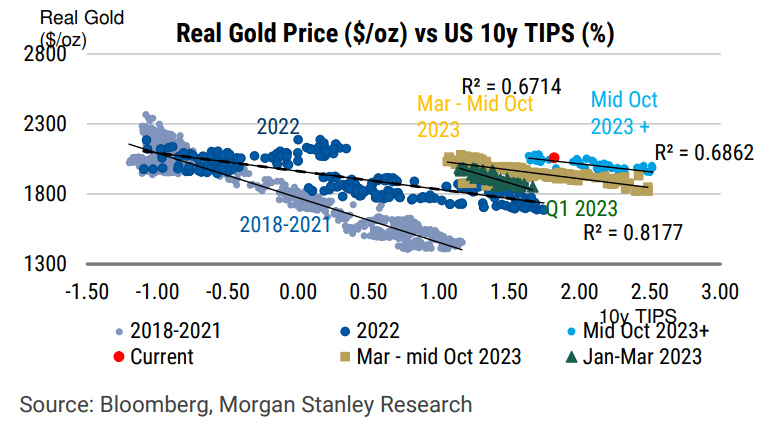

Gold’s inverse relationship with US inflation-adjusted 10-year bond yields weakened late last year as geopolitical tensions ramped up, according to Morgan Stanley analysts, delivering less upside from the sharp fall in US real yields than what would have typically occurred in the past. “Gold's relationship with real yields evolved rather than broke down in 2023, ending the year with a weaker sensitivity to yields but a growing safe haven premium,” analysts at the investment bank said in a note.

Source: Morgan Stanley They estimate that rather than the 5% increase in gold prices following the 100 basis point collapse in real yields late last year (which are calculated by taking the nominal yield on benchmark 10-year US Treasury notes and subtracting it against the yield on Treasury inflation protected securities for the same duration), bullion prices would have risen far more if the correlation was as strong as that seen between 2018 to 2021. Rather than the relationship breaking down, they believe the more appropriate description is evolving, potentially reflecting safe haven buying following an increase in geopolitical tensions in the Middle East. Morgan Stanley says risks for gold prices are higher As for what that means for the outlook, Morgan Stanley suggests the bias for prices remains higher. “If gold's safe haven premium holds, the risk-reward is probably more skewed to the upside,” they wrote. Our economists expect four Fed cuts this year, starting in June, and 200 bp in 2025. Looking back to 1990, gold has been on average 6% higher 30 days after the first rate cut.” Even with the weaker relationship to real yields, they estimate another 100 basis point drop in real yields currently implies around a further 5% upside for prices, even before large-scale central bank purchases are taken into consideration. Gold consolidating above $2000 on the charts On the charts, gold remains comfortably above $2000 per ounce, attracting bids just below the figure in mid-December despite its comprehensive rejection after soaring to fresh highs above $2100 earlier in the month. Trading in triangle pattern, convention suggests prices are more likely to break to the upside than downside having entered from below, especially if the Fed moves to begin cutting rates in March as is currently favoured by traders. Nearer-term, gold is finding buyers on dips below $2030, just above uptrend support. Those considering longs could use this zone to establish positions, although some may prefer to wait to see what comes of the US consumer price inflation report released on Thursday. A stop below $2020 or $2008 would offer protection, depending on your end target. On the topside, sellers may be located around $2058, close to where downtrend resistance is located. Above, gold was rejected just shy of $2090 in late December.

-- Written by David Scutt Follow David on Twitter @scutty

|

Send this article to a friend:

|

|

|