Send this article to a friend:

January

19

2024

|

Send this article to a friend: January |

|

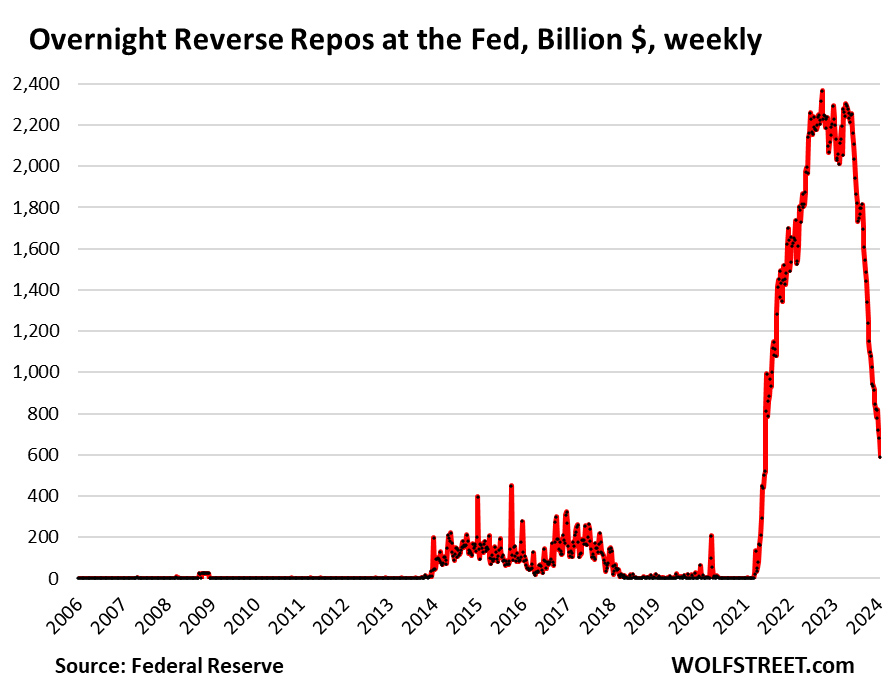

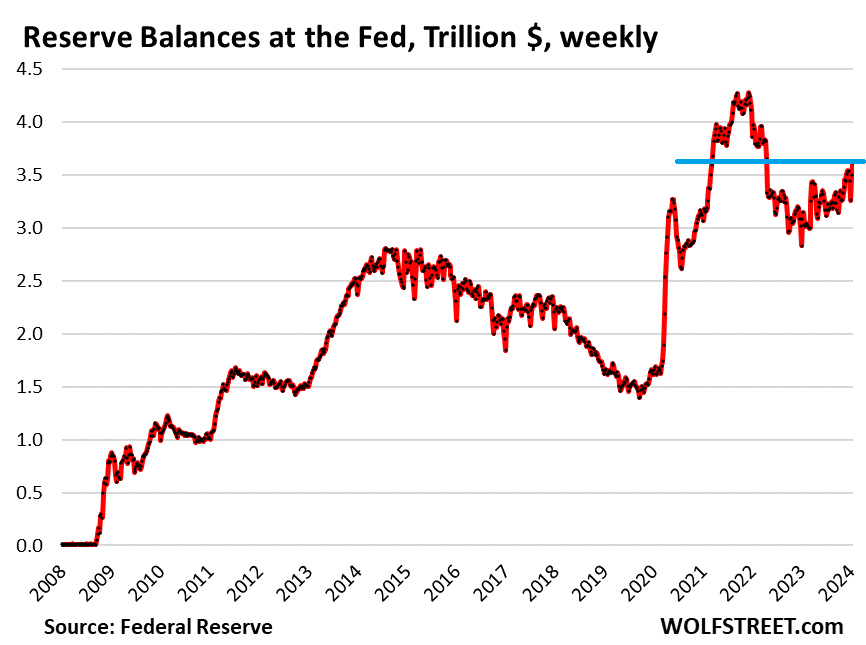

Fed’s Balance Sheet QT, Liabilities: RRPs -$1.78 trillion from Peak, to $590 Billion, but Reserves Rise to $3.6 Trillion as Liquidity Drains and Shifts

As the Fed’s Quantitative Tightening hums along on autopilot, its assets have fallen by nearly $1.3 trillion as of its weekly balance sheet released on Thursday, and its liabilities have fallen in equal amounts. The dropping liabilities are a result of QT. Here we’ll discuss two of the Fed’s big four liabilities: ON RRPs and Reserves. “Overnight Reverse Repos” (ON RRPs), where money market funds park their extra cash to earn 5.3%, have plunged by $1.78 trillion from the peak in September 2022, to just $590 billion, as QT is draining liquidity from the system. Most of the plunge has occurred since June 2023. As the chart shows, ON RRPs are normally near $0 or at $0. Now they’re going back to their normal non-QE condition. But Wall Street gurus are having a cow about it, and some predicted that all kinds of mayhem would break out if it fell below $750 billion or whatever, which it did without breaking a sweat:

The spike of the ON RRPs resulted from mega-QE liquidity that overwhelmed money market funds (MMFs), which then temporarily lent the cash to the Fed via ON RRPs to earn some interest. But starting in 2023, money market funds redirected this cash into buying T-bills, which paid more interest (around 5.5% currently at the short end) than the Fed’s RRPs (5.3%); and they engaged in the regular repo market, effectively lending cash to counterparties, especially via “term repos” such as two weeks or longer that earned more interest than the Fed’s 5.3%. MMFs are now absorbing much of the huge flood of T-bills, and they’re lending to the regular repo market, and that’s what MMFs are supposed to do. The ON RRPs at the Fed were just an outlet for this QE tsunami of liquidity. “Reserve balances,” where banks park their extra cash to earn 5.4%, have dropped by $664 billion from the peak in December 2021, to $3.61 trillion. But they’d dropped a lot more in 2022. Then in 2023 and so far in 2024, they’ve re-risen, as huge amounts of excess liquidity started shifting around the financial system, including a portion of the liquidity that got drained out of RRPs. That reserves would rise during QT – as they have in 2023 and so far this year – has been one of the big surprises to the financial world, which expected reserve balances to drop in parallel with RRPs.

Since November, reserves have been rising for an additional reason: Banks started gaming the Fed’s new bailout facility, the Bank Term Funding Program (BTFP), that had been conceived in all haste over a weekend in March 2023 and was announced on Sunday, after SVB had collapsed on Friday. When Treasury yields of one year and longer began to plunge in November, the cost of borrowing at the BTFP dropped to around 4.8% by late December, and banks could then deposit this cash (borrowed from the Fed at 4.8%) in their reserve accounts at the Fed and earn 5.4% from the Fed on it. This roughly 60 basis point spread is risk-free income for the banks. The BTFP will expire on March 11. We’ve been discussing this BTFP arbitrage for a while, including here with a chart. Since the plunge in yields made that arbitrage profitable in early November, BTFP balances have jumped by $40 billion to $161 billion; this additional $40 billion since November never left the Fed. It seems, however, that the Fed is looking askance at this trade, or else JP Morgan might be doing it with $1 trillion. Ample reserves. Reserve balances cannot go to zero, unlike RPPs. Reserves are cash that banks put on deposit at the Fed. They’re essential liquidity for the banks that they have in reserve, so to speak. Banks can collapse if they don’t have enough liquidity to meet cash outflows, as we have seen in the spring of 2023. When the Fed undertook QT last time, and reserves dropped below $1.5 trillion in the fall of 2019, banks stopped lending to the repo market, and repo market yields blew out, triggering fears of contagion, and the Fed stepped in and lent to the repo market to calm the turmoil. As a result of the experience, the Fed defined its new concept of “ample reserves.” It would make sure that reserves in the banking system are “ample,” and at the time that meant somewhere around $1.6 trillion. Today that floor would be somewhat higher. And QT will end when the Fed thinks reserves are somewhere near that floor of ample reserves. Where that floor may be will be subject to speeches by Fed governors, and Powell will get hammered at the press conference over it, and discussions will crop up in the minutes, and it will lead to wild and woolly speculations and grotesque distortions, as all this stuff does. Rebirth of the Standing Repo Facility. In July 2021, before the Fed even announced QT, it re-implemented its Standing Repo Facility (SRF). “This is back to the future. The Fed had an SRF that it used for decades as part of its monetary policy tools and to provide instant liquidity to the market when the big S hit the fan, such as during 9/11 and during the early parts of the Financial Crisis – instead of QE. This facility nearly always carried a balance, but of varying amounts, and most of the time, fairly small amounts,” we wrote at the time. The Fed, under Bernanke, had killed the old SRF in 2009 because it was no longer needed as QE was washing over the land. When QT removed some of the liquidity in 2018 and 2019, and then problems cropped up, the Fed didn’t have an SRF anymore and had to improvise a repo facility. This SRF can supply liquidity to the market and to the banking system with repos, and when those repos mature, they’re paid back and don’t stick on the balance sheet like QE bond purchases. “But this looks to me like an effort to get back to a situation where not every run-of-the mill crisis triggers more knee-jerk QE, one bout bigger than the previous one. And it looks to me like some form of preparation to make “balance sheet normalization” work out better next time than last time, which ended in the repo market blowout,” we wrote at the time in July 2021. That’s our story and we’re sticking to it. Now “balance sheet normalization” has progressed by $1.3 trillion on auto pilot, the SFR is ready to resolve issues the way the Fed used to resolve issues before QE, including after 9/11 when markets froze up. There was no QE after 9/11, there were a few weeks of heavy repos, and then markets went back to functioning, the repos matured and came off the balance sheet, and the Dotcom Bust continued. Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|