Send this article to a friend:

January

12

2023

|

Send this article to a friend: January |

|

Dip in Mortgage Rates Not Slowing Housing Bust 2:

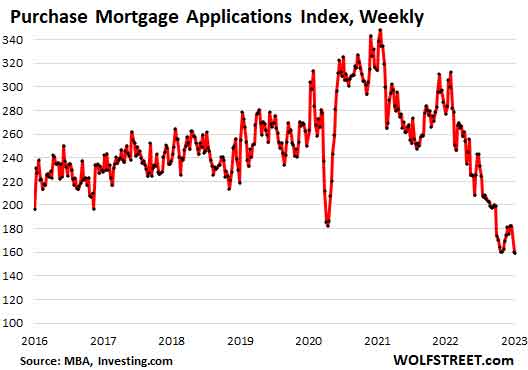

Mortgage applications to purchase a home are a forward-looking indicator of where home sales volume will be. Existing home sales that closed in November already plunged by 35% year-over-year, the 16th month in a row of year-over-year declines, making for a historic plunge. And mortgage applications went into the wrong direction from there, despite the dip in mortgage rates. Applications for mortgages to purchase a home fell to the lowest level since the Christmas week of 2014, and beyond the lows of 2014, we have to go back all the way to 1995, according to data from the Mortgage Bankers Association today. Compared to a year ago, purchase mortgage applications have plunged by 44%. Even during Housing Bust 1, mortgage applications didn’t plunge that much year over year.

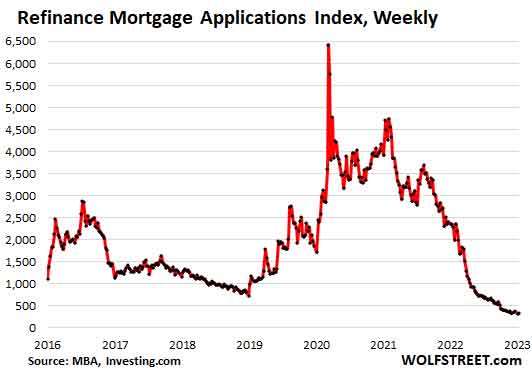

That little dip in mortgage rates had no impact. This drop in mortgage applications came despite the dip in mortgage rates that started in mid-November from the 7.1% range and hit a low point in mid-December at 6.28%. In the latest reporting week, the average 30-year fixed rate was at 6.42%, according to the Mortgage Bankers Association today. The drop in mortgage applications indicates that it doesn’t really matter to the volume of home purchases whether the 30-year fixed rate is 6.3% or 7.1%. The difference is just cosmetic. The current home prices – though they have come down in many markets, and have come down hard in some markets – are still simply way too high. Refinance mortgage volume has died: Applications to refinance a mortgage have collapsed by 86% from a year ago, despite the invisibly small uptick in the latest week. Since October, refinance applications have hovered at the lowest levels since the year 2000. And this makes sense because hardly anyone would be refinancing a 3% or 4% mortgage with a 6% or 7% mortgage, except when under duress to extract cash.

Mortgage lender woes. Mortgage lenders, whose revenues have collapsed as mortgage applications volume has collapsed, have spent the last 12 months laying off people and shutting down divisions. Some smaller operations have shut down entirely. Wells Fargo, once the largest overall mortgage lender and then the largest bank mortgage lender, is the latest to make the news with its additional efforts to step back from the mortgage market, on top of the steps it had taken in 2022. CNBC reported yesterday that it had “learned” that the bank will now re-focus its mortgage business only on its existing bank and wealth-management customers, and borrowers in minority communities; that it is shutting down its business that buys mortgages that had been originated by third-party lenders; and that it is “significantly” reducing its mortgage-servicing portfolio through asset sales. All this will entail a new round of layoffs, on top of the layoffs in its mortgage business that started in April last year. Wells Fargo only had about 18,000 mortgages in its retail origination pipeline in the early weeks of the fourth quarter, which was down by as much as 90% from a year earlier, according to CNBC, citing people with knowledge of the company’s figures. Wells Fargo shares are down 29% from their recent high in February 2022, and down 36% from their all-time high in January 2018. The mortgage lenders that surpassed Wells Fargo a few years ago are non-banks – they were aggressive in getting the mortgage business during the Easy Money era, then got crushed, and in 2022 made it into my pantheon of Imploded Stocks. They have all shed large numbers of workers, and some have shut down entire units in order to survive. Their stocks have collapsed from their highs:

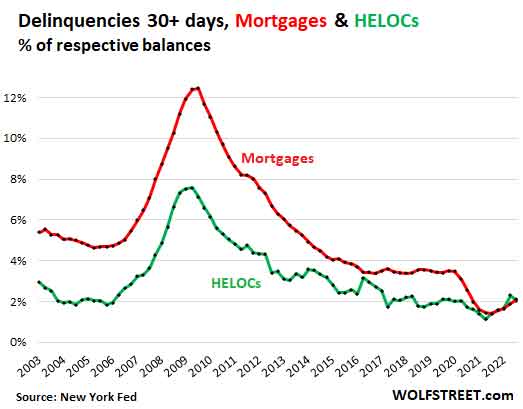

But mortgage delinquencies and foreclosures are still near record lows. What the real estate and mortgage industries are lamenting is the plunge in volume of home purchases and the plunge in volume of mortgage originations, which have caused their revenues to collapse. The issue is not the credit quality of the existing mortgages. At least not yet; that phase may come later if and when unemployment reaches high levels, which is just not happening yet despite the layoffs in tech, social media, and finance. Mortgage and HELOC delinquencies, though they have ticked up from the record lows during the pandemic, remain very low. The HELOC 30-day-plus delinquency rate ticked down to 2.0% in Q3, 2022, in line with the lows during the Good Times, according to data from the NY Fed (green line). The mortgage 30-day-plus delinquency rate ticked up to 2.1% (red line), still far lower than before the pandemic.

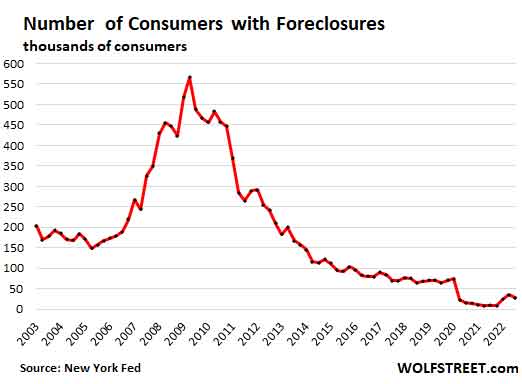

Foreclosures ticked down again in Q3 to just 28,500 mortgages with foreclosures, and remain well below the number during the Good Times before the pandemic, when there were about 70,000 mortgages with foreclosures:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)