Send this article to a friend:

January

28

2023

|

Send this article to a friend: January |

|

Nearly Everyone Fails This Basic Diversification Test

Side note: The S&P 500 is an index formed of about 500 of the largest public companies listed on U.S. stock exchanges, representing the vast majority (70-80%) of the total domestic stock market cap. An index fund owns shares of those companies – so buying any of the many S&P 500 indexes offers a stake in all 500 publicly-traded companies the index tracks. Now, this “diversify with an S&P 500 index fund” advice is everywhere. For example, the “60” in the frequently-recommend 60/40 investing strategy refers to a 60% allocation to the S&P 500 index. Even Warren Buffet has advised passive indexing stocks in this manner:

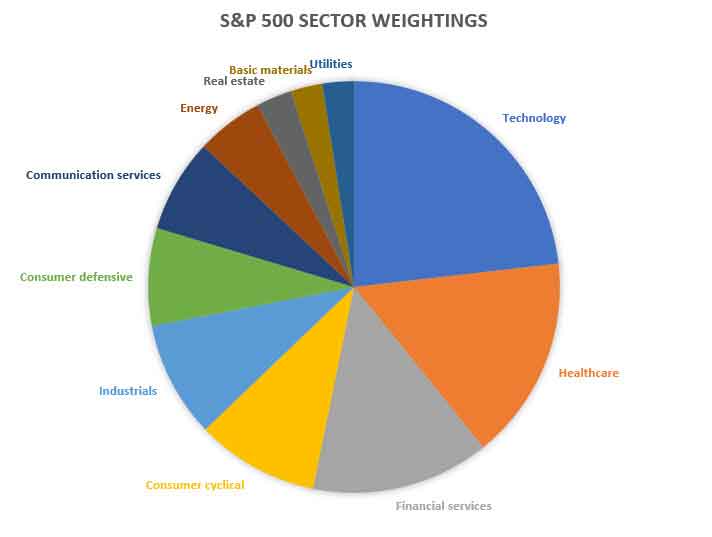

Seems like the whole world (even Warren Buffett!) thinks this “probably good enough for most investors.” It’s understandable why many people followed this rule-of-thumb advice. After all, most of us already have plenty of demands on our time and attention: career, family, self-improvement, community involvement… A simple approach to saving and investing for the future has a lot of appeal! Then things changed. Over the last two years, we’ve spoken to many people who didn’t understand why they were losing money. They thought their stock market investments were well-diversified because they followed the conservative 60/40 strategy, owned an S&P 500 index fund and a bond index. But 2022 was the worst year for this investing strategy in over a century – even worse than 1929, the beginning of the Great Depression. What went so wrong? Let’s take a closer look… The S&P 500 isn’t as diversified as you might think You may be wondering, Why is it important to diversify my portfolio, even if it includes the S&P 500? I’m going to show you. Remember, the whole point of diversification: “Don’t put all your eggs into one basket.” Owning bits and pieces of 500 different companies sounds like diversification, doesn’t it? It sounds like you have a basket with 500 different eggs in it. That’s true! But it’s also misleading, because the S&P 500 is a “weighted index.” Analysts divide companies into eleven different sectors, based on the goods and services they provide. The S&P 500 includes companies from all eleven sectors. Let’s take a look at how they’re represented:

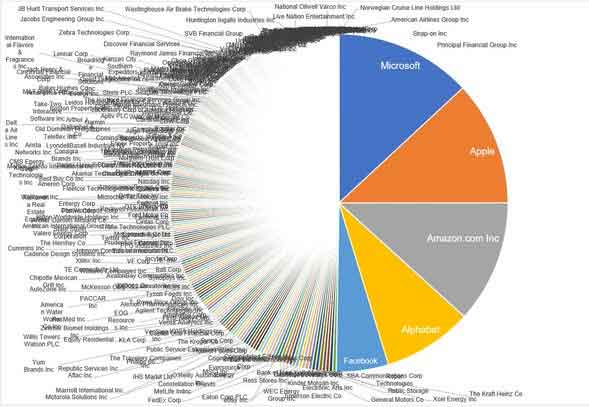

That’s right – nearly a quarter of this “diversified” index is tech companies. These are typically very economically sensitive, volatile, and frequently incredibly expensive. (Remember the sky-high price/earnings ratios of the dot-com stock bubble?) Furthermore, only three of the eleven sectors make up over half the index! Technology, healthcare and financial services – is the S&P 500 starting to look a little less diversified to you? Here’s another angle: remember, the index includes about 500 different stocks (oddly, at the moment, it’s 503 but I guess they didn’t want to rebrand). But they’re “weighted.” Instead of holding the same dollar value of each stock, larger companies are over-represented in the index. That leads to an obvious issue, best explained with another picture:

This isn’t current data but it makes a timeless point: But the problem is, only 1% of the companies on the list make up more than 1/4 of the total assets! Okay, so we have two very obvious problems of concentration here: by sector and by company. And on top of that, there’s another problem that virtually all index funds share… Index funds buy high and sell low The stocks included in the S&P 500 index are market-cap weighted, as we just discussed, using a complex mathematical model. Here’s the problem: When a stock price goes up, an index fund has to buy more of that stock When a stock price goes down, the fund has to sell that stock Do you see how this sort of behavior might not be conducive to long-term profitability? Who in their right mind buys after prices have already gone up and sells after they’ve already gone down? Performance-chasing is bad enough, but always lagging behind the market like this seems like a long-term losing strategy to me. Granted, most index funds don’t rebalance daily. Even so, quarterly rebalancing to meet their index targets guarantees they’re buying more of the expensive stocks and selling those that have lost value. When you go to the grocery store, do you buy the products as soon as the sale is over and they’re back at full price? Of course not! So why do we think this is such a good idea with stocks? If nothing else, I hope this brief discussion has convinced you that simply owning an S&P 500 index fund is not “diversification.” So what should we do instead? Diversification beyond index funds If you’re looking for answers to these problems, you’ll probably want to look beyond simple index funds. Portfolio diversification “done right” has proven itself to be one “key for long-term investment success,” according to experts. Remember Nobel Prize-winning economist Harry Markowitz’s observation:

With that in mind, perhaps now is a good time to consider going broader, like the experts at Sarwa suggest:

Diversification is a big topic! And there’s a massive financial services industry (15% of the S&P 500, in fact) desperate to repackage their products and sell them to you. I strongly recommend you do thorough due diligence before spending a single dollar on anything – even advice! And personally, I don’t invest my money in anything I don’t understand… There are some suggestions for alternatives to the 60/40 portfolio here. When you’re looking for diversification options, ask a few questions: Are these assets correlated? Do they tend to move in the same direction? If you aren’t sure, you can compare correlations of different asset classes here for free. How much overlap is there? For example, the Dow Jones index holds 30 stocks, which are also included in the S&P 500 index. Is there a better way to lower my risk? When done right, diversification can lower volatility (aka risk) without sacrificing much, if any, return. If you want to diversify your savings so you can sleep better at night, it’s worth your time to learn more about diversifying with physical precious metals. Gold and silver can offer a level diversification you’d be hard-pressed to find anywhere else. Gold and silver have historically been safe havens during periods of economic turmoil and crisis. And during the good times, both have served as inflation-resistant stores of value for your hard-earned dollar.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)