January

5

2013

5

2013

|

January 5 2013 |

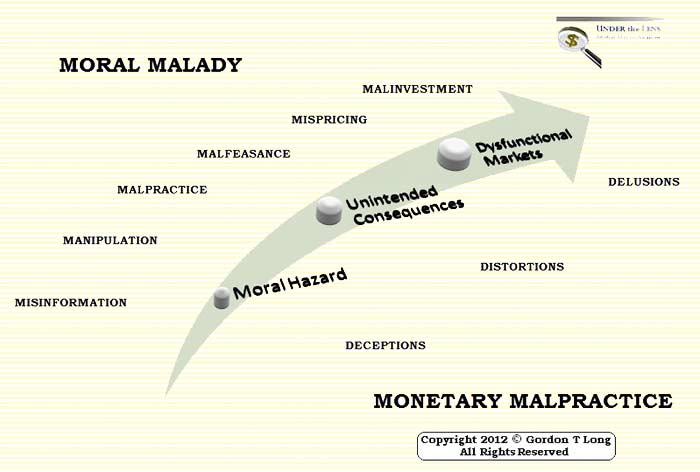

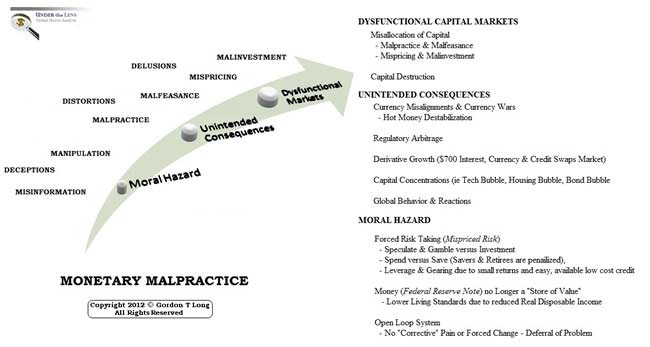

Monetary Malpratice

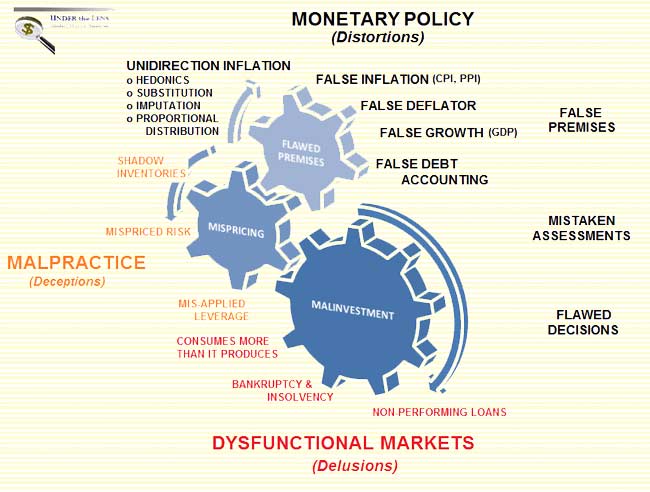

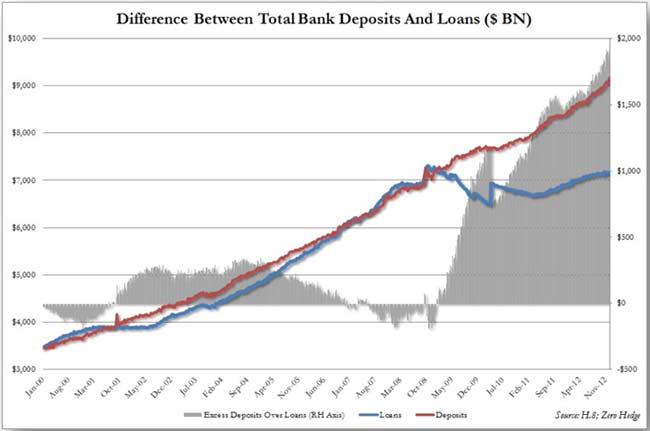

Dysfunctional Markets One of the first axioms of analysis is: "Garbage In, Garbage Out"! If your data is flawed, everything you do with it and the decisions stemming from it are flawed and dangerous to your financial health. Experienced analysts will often be found relentlessly checking, rechecking and validating their inputs and assumptions. If economic practitioners were held to higher standards of accountability, they simply wouldn't accept the raft of fundamental data points that are the pillars of most economic assessment. I am talking specifically about government inflation numbers such as CPI and PPI, the Deflator and GDP growth statistics and true debt levels using sound GAAP accounting principles and reflecting off balance sheet special purpose entities, contingent liabilities and financial guarantees. The list of government reporting irregularities is pervasive and for unknown reasons, simply accepted. It is incredulous that we can just accept, without challenging, the statistical hyperbole of Hedonics, Substitution, Imputation and Proportional Distribution, justifying inflation numbers that don't even pass the common sense of an unemployed high school dropout. I don't mean to disparage the high school dropout, but I do point the figure at the 'six figure' analysts who accept this tripe as gospel, and from whose analysis fiduciary investment decisions are made with the unsuspecting public's hard earned savings. This problem has been going on long enough that flawed data has resulted in broad based asset mispricing and malinvestment. Data points have become so distorted, as to be delusional, and have left the markets dysfunctional. How else do you explain $2 trillion excess investor savings over loans now sitting at US banks? How else do you explain Capital Investment (CAPEX) falling faster than Felix Baumgartner from 128,100 feet? This is the third in a trilogy on Monetary Malpractice, so I will refer a lot of the discussion on the chart to the right, to those wishing to read MONETARY MALPRACTICE: Distortions, Deceptions and Delusions or MONETARY MALPRACTICE: Moral Malady. I would like instead to focus on the specific mechanism by which Monetary Malpractice has now delivered Dysfunctional Financial Markets. Before I drop you into the 'gearing' of it, let me show you the bottom line results. LINKAGES

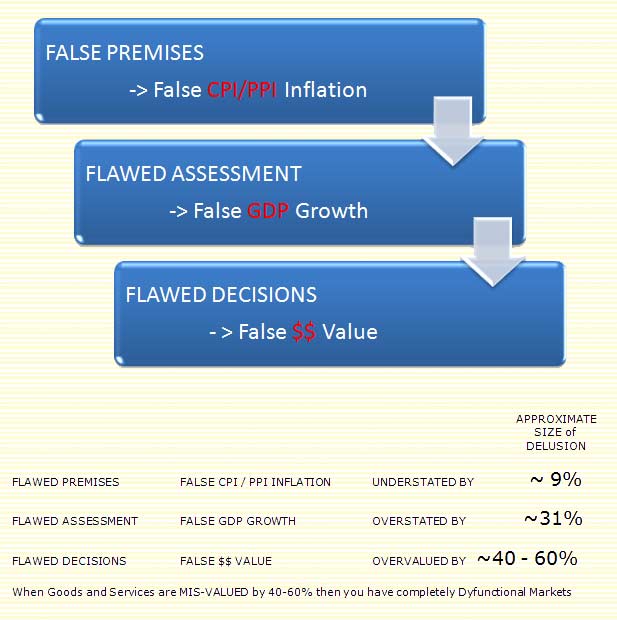

Dysfunctional Markets exist when normal and expected 'causes and effects' no longer occur. FALSE PREMISES

Let us therefore start with Inflation, remembering:

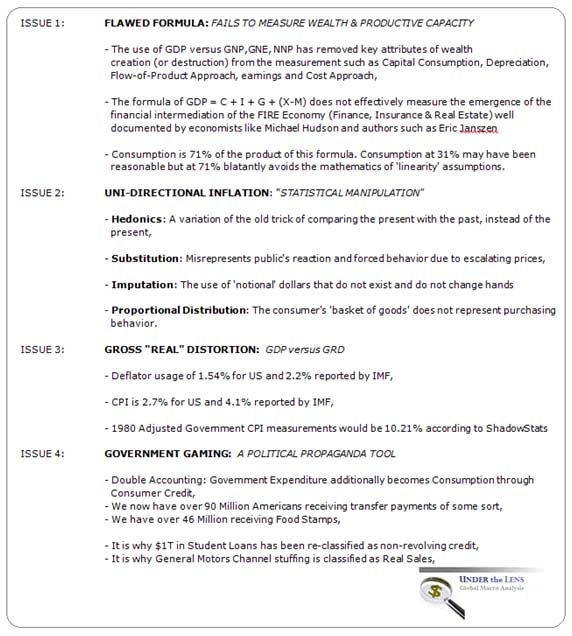

The manipulation and distortions presently occurring in the government's CPI & PPI inflation numbers are so significant that it requires an exhaustive discussion. An extensive number of presentations with leading analysts on this specific subject can be found in the Macro Analytics Library. I have compiled the following chart to best summarize the areas that must be covered in such a review.

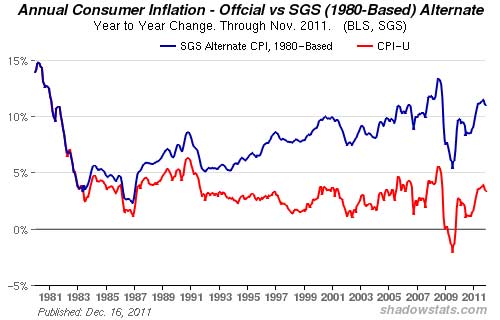

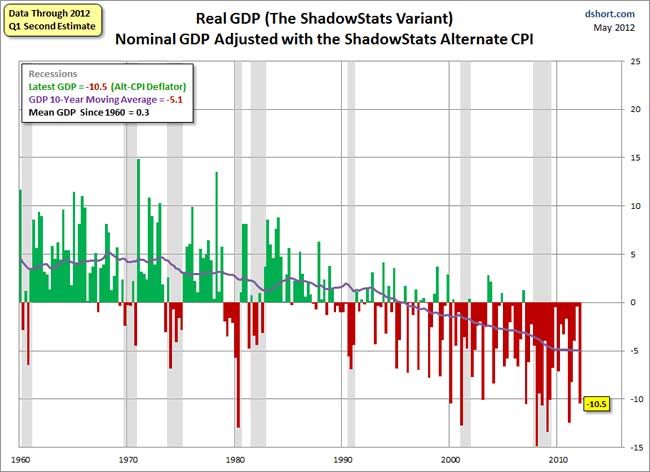

John Williams at ShadowStats.com has done meticulous and invaluabe service in tracking the insidious changes the government statistians have implemented to effectively achieve what I refer to as Uni-Directional Inflation. Nothing they do ever makes it larger, only smaller. This is so prevalent, that as the chart from ShadowStats illustrates below, the distortions now understate inflation by over 10%, if we assumed that in 1980 we knew what we were doing or even if we didn't, how we have inflation explode on a comparative basis. This has profound implications and cascades through to GDP Growth reporting and the Mispricing and Malinvestment decisons that subsequently result.

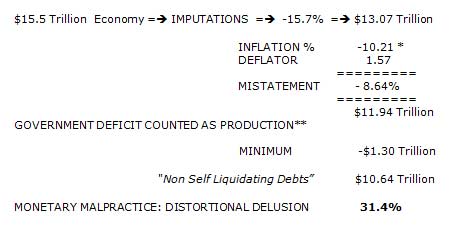

IMPUTATIONS Of all the inflation distorted items in the category of "Uni-Directional Inflation" in my chart above, the one that few undertand, and even fewer publically discuss, is the concept of "Imputations". Imputations are fundamentals about dollars that do not exist and dollars that do not even change hands. They are in some instances a replacement measurement of “notional value”. The following table summarizes the degree to which they are applied and the magnitude of their current distortions. (The details are discussed in: Economic Growth - Fake Numbers, Real Growth, Consequences of Lies.)

FALSE GROWTH

This level of distortion will quickly become fatal as corproations make investments based on expected economic growth. As we will show, corporations have been forced to stop believing government numbers. Their revenue and sales have shown reality is simply quite different from government distortions. The reason John Williams started tracking government statistical adjustments was because his corporate accounts couldn't rationalize the difference. This was years ago and has now grown into an independent business operating a government "ShadowStats" service. Using simply ShadowStats inflation adjusted numbers, GDP growth is overstated by minimally 10.5%.

HOW THE DISTORTIONS GROW

MISPRICING When an investment does not YIELD more than REAL inflation, plus a premium to REFLECT the additional risk of the underlying asset class, you have not only a poor invesment but an asset that is mispriced. An asset's value is based on this being achieved. Monetary Malpractice of unsound money will consistently lead to mispricing.

Mispricing will continue to occur and worsen due to:

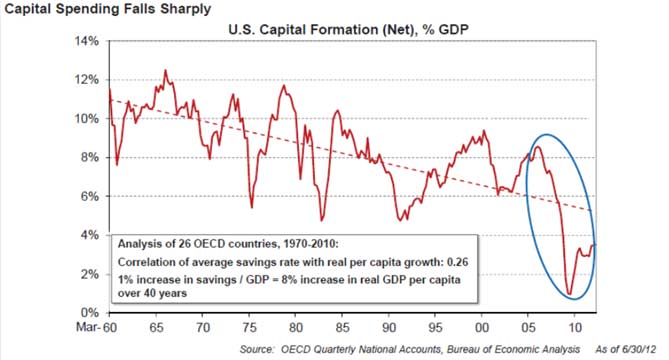

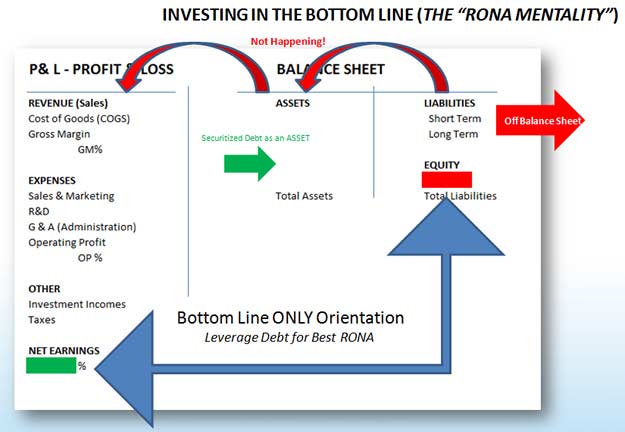

This list is only the tip of the iceberg since sustained Monetary Malpractice with its consequential Moral Hazard and Unintended (or INTENDED) Consequences has resulted in broad based mispricing and dysfunctional markets. MALINVESTMENT A malinvestment in its most basic terms is an investment that does not produce more than it costs in real terms. A Malinvestment in Austrian Economics terms is one that is OVERPRICED due to excessive leverage available whether it be credit availability or abundance of paper fiat money created out of thin air. FLAWED & OBSOLETE ACCOUNTING In the current Dysfunctional Markets, to an ever increasing degree, it can not be determined if an investment is a malinvestment, because the amount of debt, financial contingencies and financial guarantees are hidden from investors by offshore entities. Without visibility to this information no determination can be made. The entire global bond debt market, which approximates $200 Trillion, hinges on this blatant obvuscation. NON-PERFORMING LOANS If markets weren't dysfunctional and malinvestment running rampant, then the 'canary' of non-performing loans wouldn't be as prevalent as it is. Whether we are talking consumer debt from mortgages and HELOCS (Home Loans) to student loans, levels of delinquencies, forced refinancing, defaults and personal bankruptcies are at all time highs. If it wasn't for historic and unprecedently low interest rates, which allow commercial and government debt 'roll-overs', we would be witnessing bankruptcies on a massive scale. Malinvestments are presently being 'papered' over by the printing presses of the central bankers. CAPITAL EXPENDITURES When money is as cheap as it presently is, then it would be expected that opportunities should be endless to put money to work based on substantially lower hurdle rates. This is not the case because malinvestment is so pervasive, that CFO's cannot see satisfactory risk adjusted investments. Corporate takeovers are down substantially, IPO's are nearly non-existant and corporate capital expenditure is in near free fall as shown to the right. This is astounding when considering that REAL interest rates are negative.

SAVINGS VERSUS LOAN LEVELS If investments weren't seen to be mostly malinvestments, than why is there $2 Trillion more in bank savings than in bank loans? These are bank deposits paying close to zero. The short answer is there is nothing worth investing in when considered on a real, risk adjusted valuation basis.

LEVERAGE REQUIRED AND DEBT HELD Many investments today are currently only profitable through the application of excessive, cheap leverage. Based on the 'greater fool' philosophy of investing, leveraged investors hope to 'flip' and be out before cheap leverage shifts against them. CONCLUSION DYSFUNCTIONAL MARKETS Markets have become so dysfunctional with so much cheap money chasing so few real opportunities, that collateral values within the rehypothecation process are now in jeopardy and exposed to collateral contagion. Real economic growth cannot return without real top line corporate growth. It simply isn't there as is seen by falling CAPEX and money going into savings.The financialization focus continues to be strictly on bottom line growth and specifically non operating income. This is the area where the financial engineers are employed today. This works for profits in the short term but strangles growth and profits in the long term.

"In America the smartest engineers are primarily engaged in creating financial ways to take money out of the pockets of others"

What would things look like if the Fed wasn't engaged in Monetary Malpractice?

Sign Up for our FREE 2013 Thesis Paper. To read more, go to GordonTLong.com

Mr. Long was a senior group executive with IBM and Motorola for over 20 years. Earlier in his career he was involved in Sales, Marketing & Service of computing and network communications solutions across an extensive array of industries. He subsequently held senior positions, which included: VP & General Manager, Four Phase (Canada); Vice President Operations, Motorola (MISL - Canada); Vice President Engineering & Officer, Motorola (Codex - USA). After a career with Fortune 500 corporations, he became a senior officer of Cambex, a highly successful high tech start-up and public company (Nasdaq: CBEX), where he spearheaded global expansion as Executive VP & General Manager. In 1995, he founded the LCM Groupe in Paris, France to specialize in the rapidly emerging Internet Venture Capital and Private Equity industry. A focus in the technology research field of Chaos Theory and Mandelbrot Generators lead in the early 2000's to the development of advanced Technical Analysis and Market Analytics platforms. The LCM Groupe is a recognized source for the most advanced technical analysis techniques employed in market trading pattern recognition. Mr. Long presently resides in Boston, Massachusetts, continuing the expansion of the LCM Groupe's International Private Equity opportunities in addition to their core financial market trading platforms expertise. GordonTLong.com is a wholly owned operating unit of the LCM Groupe. Gordon T. Long is a graduate Engineer, University of Waterloo (Canada) in Thermodynamics-Fluid Mechanics (Aerodynamics). On graduation from an intensive 5 year specialized Co-operative Engineering program he pursued graduate business studies at the prestigious Ivy Business School, University of Western Ontario (Canada) on a Northern & Central Gas Corporation Scholarship. He was subsequently selected to attend advanced one year training with the IBM Corporation in New York prior to starting his career with IBM. FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a 'fair use' of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond 'fair use', you must obtain permission from the copyright owner. DISCLOSURE Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. While he believes his statements to be true, they always depend on the reliability of his own credible sources. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments. COPYRIGHT © Copyright 2010-2011 Gordon T Long. The information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. Please note that Mr. Long may already have invested or may from time to time invest in securities that are recommended or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him. |

|

|

|

Gordon T. Long has been publically offering his financial and economic writing since 2010, following a career internationally in technology, senior management & investment finance. He brings a unique perspective to macroeconomic analysis because of his broad background, which is not typically found or available to the public.

Gordon T. Long has been publically offering his financial and economic writing since 2010, following a career internationally in technology, senior management & investment finance. He brings a unique perspective to macroeconomic analysis because of his broad background, which is not typically found or available to the public.