Send this article to a friend:

December

18

2024

|

Send this article to a friend: December |

|

Will the New Tariff Coming to Town Put Stocks in the Stockade or Shoot up Inflation?

I won’t be that quick. One thing in common with all of the interviewees was that they believed the market still had a little time to accelerate its blow-off rise, such as, at least, a month. It’s possible, of course, the big event has started a bit ahead of their schedule. It’s also possible this is a little calm before the blow-off storm. I’ve avoided making any predictions on what the market will do this year (and last), myself, because insanity is not known for predictability. The present lull may be a foreshock to that crash. Bank of America today notes that America now appears to be all-in on stocks and says that is a typical place for a 2-3% decline to begin. That’s far from a crash, but the fact that there is very little cash sitting on the side. Fund managers have only an average of 3.9% of their portfolios sitting in cash. Put another way, they are a “net 14% underweight” in cash, which is down from a record high of “36% overweight.” That tends to indicate there is not a lot of cash left to move into stocks. Of course, corporations can still raise a lot of cash for buybacks, regardless of where managed portfolios are sitting.

Fund managers are split, however, on whether Trump’s first year will bring a bigger boom due to the rise in sentiment it has created and the regulation cuts or a crash due to tariffs crushing trade in a major trade war and killing consumers with higher inflation. There’s a new tariff in town To the contrary on tariffs, Trump’s nominated trade sheriff, Peter Navarro, makes what I consider a classic political dumb statement by claiming new tariffs won’t raise prices for American consumers. That kind of totally partisan reasoning reminds me of the decades of claims by Republicans that capital-gains tax cuts would trickle down from the rich to the rest, which they never did. Middle-income wealth, adjusted for inflation, all but froze, while the top ten percent soared to mountain peaks far above the clouds. Of course, tariffs will raise inflation. Anytime you add another 6% tariff to the cost of all goods coming into the country, everyone importing those items will raise their prices as much as they can to avoid eating the loss themselves. The promise Trump has repeatedly made that the people living in the nations whose goods are being tariffed will pay those taxes to the US is total fantasy talk. Sure, US importers will do all they can to get suppliers from other nations to reduce their prices by enough to offset the new tariffs in town, but those efforts always meet substantial resistance. They may get foreign manufacturers to eat some of the cost of the tariffs, but typically not much, especially with nations like China, already under tariffs, where that one-trick pony has already been ridden to death. Secondarily, when the price of imported goods does rise, Americans tend to shift to what were formerly more expensive domestic goods, and the reduction in foreign supply competition for American manufacturers from foreign suppliers, coupled with the increase in domestic demand, gives those American companies more latitude to raise their own prices. So, Navarro is blowing smoke up somewhere that doesn’t smell good. As his proof, he claims that Trump tariffs did not cause inflation during Trump’s first term:

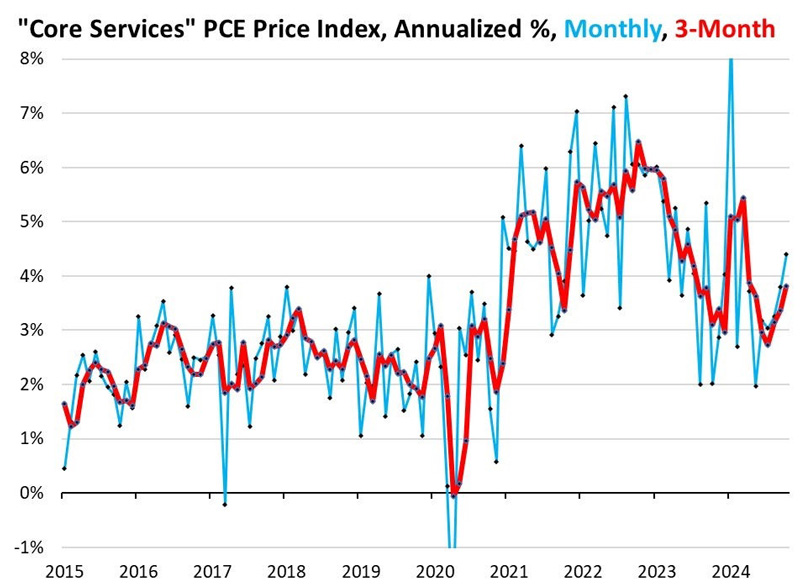

I would argue that those tariffs hit in the latter part of Trump’s term and badly damaged supply chains, as we heard corporations everywhere complain about endlessly. Those broken supply chains became a big part of the inflation that started shortly after his term ended. We simply needed some major money printing to prime the pump, because money printing’s is also key to inflation; and we got that under Trump and Biden during the Covidcrash. Once personal accounts were flowing with the new money, the combination of two much money chasing too few goods did exactly what I said back then it would do and blew prices through the roof for years to come. Don’t expect a man whose paycheck as tariff chief demands he sell you this bill of goods to tell you anything else. By the time we learn he’s wrong, however, the damage will be severe. Simply put, US companies will not be able to fully offset the cost of additional tariffs with price adjustments from their foreign suppliers, especially now that they’ve used that tactic on the current tariffs, leaving little margin among foreign manufacturers to do any more of that, and those US companies will do all they can to pass their increased costs on to consumers because that is what they always do. Consumers will shift to other brands or alternative-but-similar kinds of products, but that increased demand on those products will tend to raise their prices, too. This time is different The second major difference is that, last time tariffs were placed by Trump, it was during a period when the Fed could not seem to get inflation to rise, even when it tried its best for years. We had been trending for a decade below the Fed’s 2% inflation target. As John Rubino reminds us today, we are now trending above that target. The Fed’s most favored inflation gauge, he points out, looks like this:

So, this time around, additional tariffs will be established when the Fed can’t seem to get inflation back down and is actually seeing another stubborn rise like the big one we saw at the start of the year (both predicted here when most voices were claiming the opposite would happen). Tariffs won’t be starting with a stiff deflationary headwind this time like they did last time. They will be starting with a stiff inflationary tailwind already pushing prices upward. Speaking of false assurances, let’s look again at BidenomicsWe ave one follow-up matter today regarding things I’ve been saying here all year that are finally being proven. The Fed just reported today that that latest adjustments in job numbers bring the total creation of jobs for the entire year down to negative territory. All of those Biden-proclaimed job gains were phantom gains. The labor metrics were as shoddy as I said they would prove to be.

|

Send this article to a friend:

|

|

|

Ten days ago I published a

Ten days ago I published a