Send this article to a friend:

December

02

2023

|

Send this article to a friend: December |

|

Drumbeats of Recession

It’s been a long time since global wars and recession have joined hands. Yet, with two major wars that each have the potential of becoming world wars, we also hear the drumbeats of recession growing very close now. Today’s economic reports were full of recession. We have also never faced so many bubbles blown up to such enormous sizes that are deflating together, which is where the potential lies for a deep recession. Some real investment advice

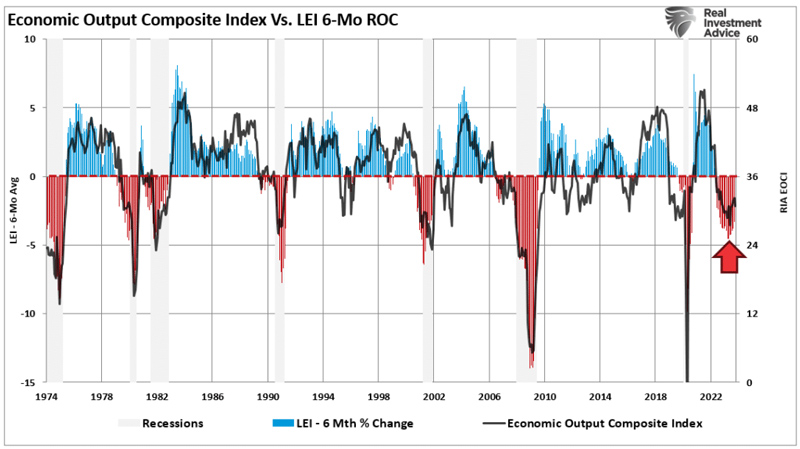

First up: an article from Lance Roberts of Real Investment Advice, whom I find to be a neutral voice generally on which way the market or economy is heading — meaning one who just goes by the charts and numbers with no tendency to lean bearish or bullish beyond what the numbers show. Today he writes,

He goes over a couple of his primary indicators and comes up with the following:

Just as I said the yield curve would be slow in arriving to the party by inverting in 2022, and then it arrived after we started into the technical recession of 2022, I’ve also said it will be slow in leaving the party — last one out the door — probably reverting right as the deeper part of this recession gets underway. The reasons for that are simple: The Fed has so messed up the yield curve by manipulating it with massive bond purchases for years and now massive bond rolloffs, that the Feds massive manipulation in both buying and dumping has to get out of the way before the yield curve can show natural market truth.

Roberts also notes,

Except, I think it won’t be as long as he thinks until we know. In terms of the lag effect for Fed actions that have already taken place, he says,

I think we are seeing a lot of that now, as I’ve pointed out in recent articles, and will provide additional evidence for in this article. The Fed knows all about the lag time and is counting on further slowing to continue through the end of 2024. It has said as much many times; so it is ludicrous for investors to think the Fed would lower rates when this continued decline due to its own lag effect is exactly what the Fed keeps saying it wants to see and believes it will see. Therefore, the Fed will not pivot as the market believes unless things break so badly that the breakdown, itself, causes the market to fall off a huge cliff, which is hardly a reason for the market to be rising now due to belief in a “Fed pivot.” That merely raises the height of the cliff it is going to fall from. Lance concludes,

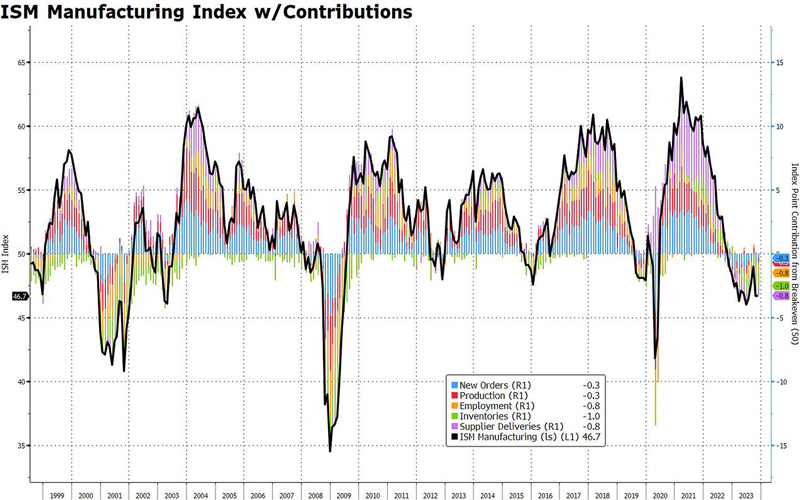

Manufacturing a recession Another lousy manufacturing survey came in today, pounding the same beat other surveys have been hammering. As a solitary counter-beat, we did get a survey out of Chicago this week that was the equivalent of a bumper crop. I’m calling it anomalous, though, because all other surveys of its kind have shown metrics that say their own regions are fully in recession already. Today we got more backup to those other surveys from S&P Global's US Manufacturing PMI, which dropped to 49.4 (recessionary) from 50.0 (neutral) in October. Likewise,

Zero Hedge referred to these measures as “stagflationary recession” signals. That, of course, is exactly the kind of recession I’ve consistently said this will be. So, the data is coming in as expected here, except for that one-off from Chicago. ZH shows a graph that looks a lot like Lance’s Economic Output graph above, except that this graph follows up on the final segment of Lance’s graph, which showed an upturn, with with strong evidence the upturn didn’t hold:

Lance’s Economic Output graph showed the hint of a downturn after the upturn, but here we see a more severe one, heading right back down into deeper recession. While they are graphing different things, they are corollaries. Given how well they usually synch up with each other, I would expect the Economic Output graph to match down to this one. The survey also showed that manufacturers’ prices have started rising again. Survey espondents reported,

And the worst sounding response was …

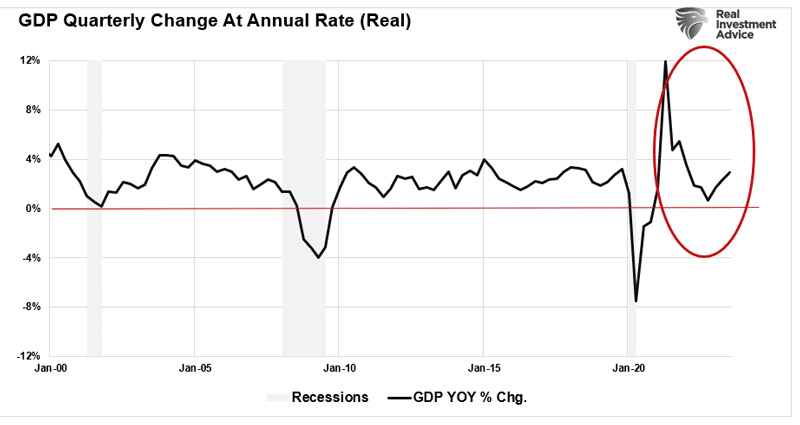

As to where this will likely put fourth quarter GDP growth:

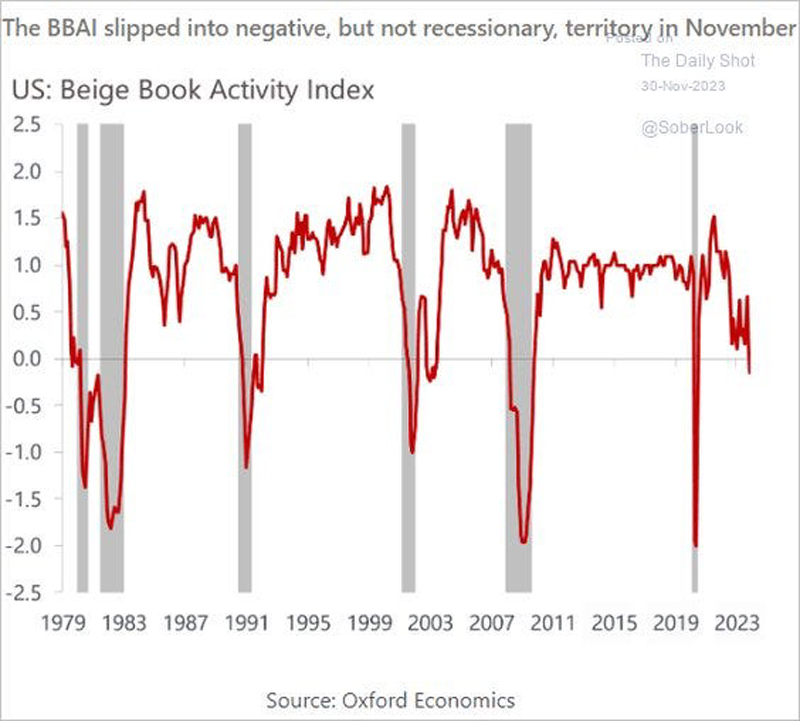

Recessionary. Even the Fed says recession Finally, the Fed’s famous and much-watched Beige Book put in a matching report today:

The Beige Book has gone into contraction for the first time since the short Covid Lockdown recession of 2020. It only goes down during recessions, and anything below 0.0 is actually recessionary. As you see, almost all recessions have been eventually declared to have started as soon as the Beige Book dipped below 0.0 So, it is recession all the way in the news today. Believe otherwise, if you want; I’m just going where I find the bulk of the evidence now points. Thank you for reading The Daily Doom. This post is public so feel free to share it. The Daily Doom is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)