Send this article to a friend:

November

16

2024

|

Send this article to a friend: November |

|

The Anatomy of a Bubble

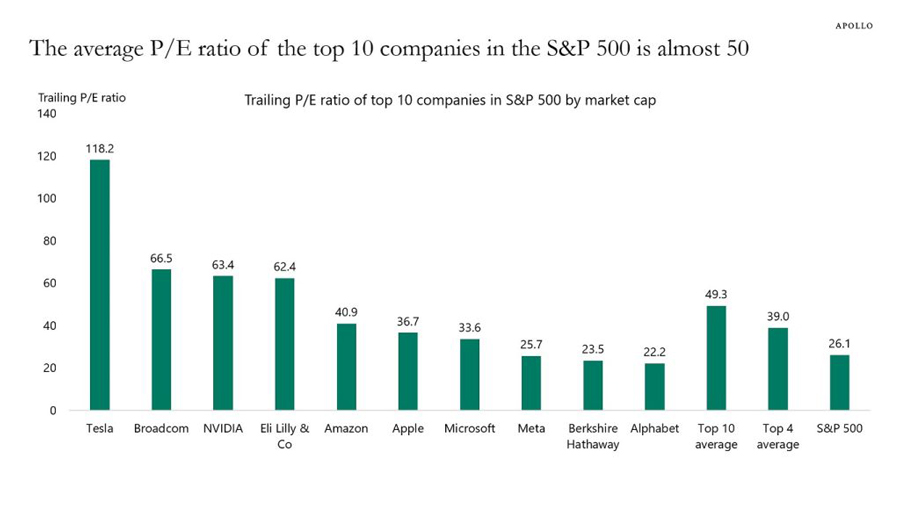

-John Templeton, legendary mutual fund manager In 2006, I asked a realtor friend if we were in a housing bubble. He assured me that everything was fine. Defaults were low – and this is my favorite – “housing prices always go up”. Back then, I didn’t know that the Federal Reserve had intentionally created the real estate bubble. As Paul Krugman wrote in 2002, “Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.” The Fed did just that, lowering interest rates to record lows, and spurring a huge increase in home prices. Over the next few years, the home lending market was “financialized” to an incredible degree. Credit default swaps, mortgage-backed securities, and subprime loans all flourished. The end result was a gigantic mess that almost took down the largest banks in the U.S. But in the midst of it, almost everybody loves a bubble. It’s an exhilarating experience. Governments also love speculative manias. They create a windfall of tax revenue, and make it a heck of a lot easier for politicians to get re-elected (until they crash). But who cares about a crash, right? That’s far in the future and politicians won’t bear any responsibility anyway. Back in a Bubble Surprise, surprise. We’re back in another one. The average price/earnings ratio of the 10 largest companies in the S&P 500 has now reached 49x.

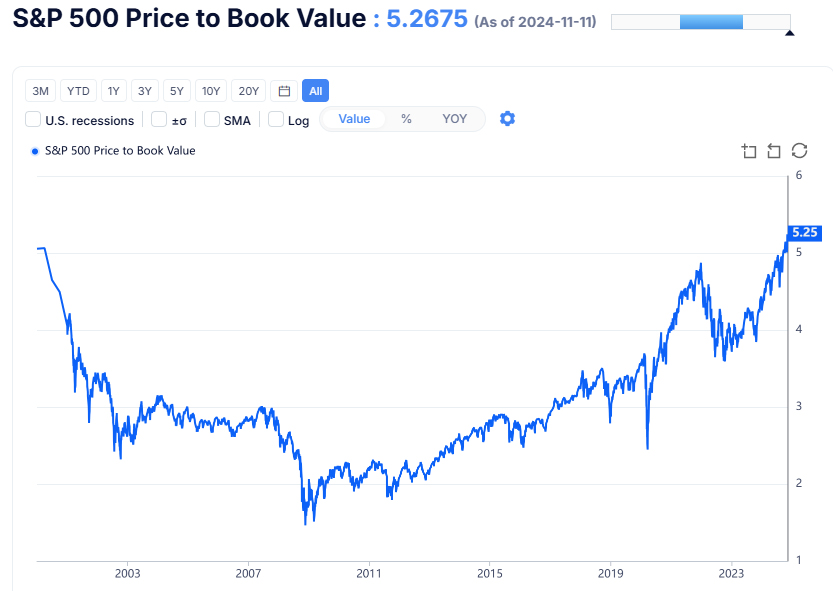

Source: Apollo Academy That is extremely rich pricing. It means if these companies paid out 100% of their annual profits, shareholders would only receive a 2% yield. That’s very low by historical standards. The S&P 500’s price-to-book ratio, another classic valuation gauge, recently surpassed dot-com bubble levels.

This ratio simply compares the “book value” of a company to the market cap of their shares. A price-to-book level this high indicates major overvaluation in US equities. For comparison, the price-to-book ratio in Brazil, an emerging market, is about 1.5. And in Europe, a developed market, it’s 2.0. I could trot out a dozen more metrics that show the U.S. is in bubble territory. Just look at the Buffett Indicator, Warren Buffett’s favorite gauge of valuations. It all shows fresh all-time highs in share prices compared to GDP. It’s easy to see why Uncle Warren has amassed a record cash stash at Berkshire Hathaway. The US is clearly in “bubble” territory. Stocks are priced for perfection going forward. But, of course, that doesn’t mean we can’t go quite a bit higher before it crashes down. In the opening quote to this article, Templeton says that bull markets “die on euphoria”. What he means is there is usually a “blow-off top” (BOT) at market peaks. A tremendous last hurrah! Have we seen a BOT yet? Maybe not. It’s hard to believe markets could go even higher, but they often do just that. The Complicating Trump Factor Markets are fired up about Trump’s win. And for good reason, as I noted in Markets Point to Trump Victory. President Trump will be far better than Kamala for America’s economy. But is Trump’s victory enough to justify the current bubbly valuations? No. Trump was dealt a horrible economic hand, and if everything goes to plan, and he slashes federal spending and eliminates government waste, it will be a difficult 4 years. As we discussed last week in Trump’s Clean-House Mandate, true reform will also bring pain. Short-term sacrifice for long-term growth is required. Markets often rise after elections, but it doesn’t always last, as we saw with Hoover’s win in 1928, which was shortly followed by the 1929 Great Crash.

Source: Bloomberg I’m not saying we’re about to enter another 1929 situation. I’m pointing out that a bullish start to a president’s term doesn’t always continue. I am, however, preparing for a potential crash. I’m keeping more cash on hand than usual. Additionally, I will continue to add to gold and silver positions, especially if the current correction continues. The future for precious metals remains bright. As billionaire Paul Tudor Jones says, “All roads lead to inflation”. Yes, even with Trump at the helm. No matter what happens, the Federal Reserve and Treasury will need to get “creative” in the near future. And that means one thing: fire up the printers.

Adam Sharp has been a financial writer and Fed watcher since 2008. He is a contrarian who specializes in non-traditional assets. Adam founded and sold Early Investing, a newsletter about alternative investments. Sharp lives in Maryland with his wife, two children, and two dogs.

|

Send this article to a friend:

|

|

|