Send this article to a friend:

October

31

2023

|

Send this article to a friend: October |

|

Fed’s QE Giveth, Fed’s QT Taketh Away: Russell 2000 Hits 3-Year Low, Nasdaq Back to Dec 2020, S&P 500 Back to Apr 2021

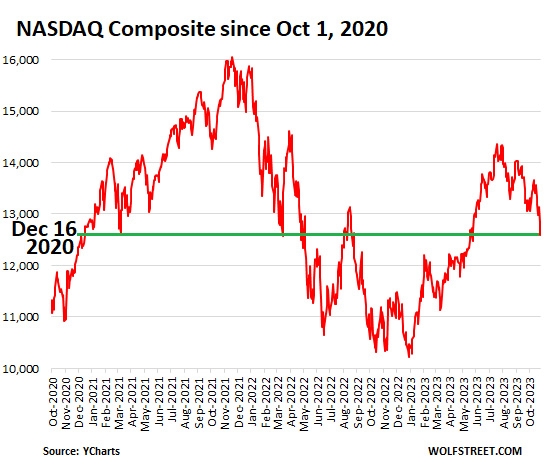

There are some things happening in this inflationary world that contradict well-established previous wisdoms, including that stocks are a hedge against inflation. Turns out, since QE started in 2008, all prior wisdoms had to be thrown out the window, and the new wisdoms are all about QE and now QT: QE makes stocks go up, and QT makes stocks go down, no matter what inflation and the real economy do. The Nasdaq Composite closed on Friday at 12,643, down 22% from the peak in November 2021, and back where it had first been on December 16, 2020. Despite huge gyrations, it has gone nowhere in nearly three years. And the huge rally through July 2023, fired up by the Fed’s lightning-fast $400 billion in bank-panic liquidity injection, is threatening to turn into the biggest sucker rally ever. The problem is that the Fed then had quickly withdrawn the liquidity and followed up with record QT, now amounting to over $1 trillion.

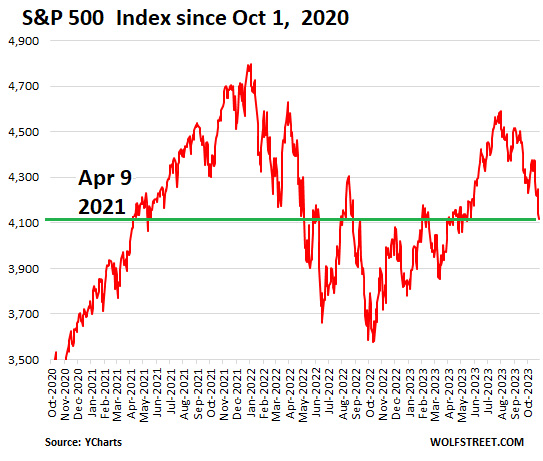

The S&P 500 index closed on Friday at 4,117, down 14.6% from the peak on January 3, 2022, and back where it had first been on April 9, 2021 In other words, despite all these gyrations, it has gone nowhere in about two-and-a-half years. And the huge rally, driven by the Fed’s $400 billion in bank-panic medication, fizzled out at the beginning of August, and it been careening downhill QT Way.

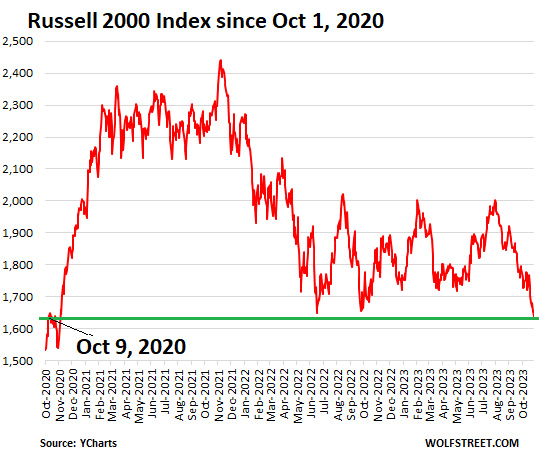

The Russell 2000 index, which tracks small stocks, which often lead the big stocks, closed on Friday at 1,637, a three-year low, down 33.4% from the peak on November 8, 2021, and back where it had been on October 9, 2020. It’s getting curiouser and curiouser. The small stocks in the index had largely been forgotten by the effects of the Fed’s $400 billion liquidity injection, which caused the biggest stocks to spike by huge amounts – and they came to be called the Magnificent 7, because they and a few other giants largely carried the entire market, until they too sagged. But this is the small fry:

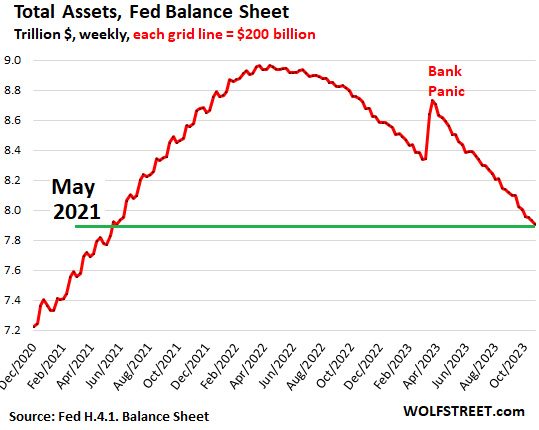

The Fed, over roughly the same period, has fueled the surge in stocks with huge QE until the end of 2021, when it began to taper QE. It ended QE in early 2022; and it started QT in July 2022. Since then, its balance sheet has dropped by $1.06 trillion to $7.91 trillion, the lowest since May 2021. Stocks and the Fed’s balance sheet obviously don’t move in lockstep. But the liquidity that the Fed throws at the markets drives up asset prices, and it drives up stock prices the fastest, and the withdrawal of liquidity pulls the rug out from under stocks.

When QE was driving up stock prices, everyone investing in stocks was a genius, and people were coming up with all kinds of theories why stocks were going higher and higher, when in fact, the only reason they were going higher and higher was the Fed’s QE. Then something big broke, the biggest thing the Fed is in charge of: Price stability. We got the worst bout of consumer price inflation in 40 years, and even the Fed, after being in denial for way too long, acknowledged that this was an issue and cracked down with big rate hikes, bringing its policy rates from 0.25% to 5.5%, and with so far $1.06 trillion in QT. And there is still a long way to go with QT, as inflation appears to have become nicely entrenched, with suddenly worsening inflation data in the worst parts of the spectrum of goods and services coming out on Friday, which caused me to mutter: Powell’s Gonna Have a Cow When He Sees the PCE Inflation in “Core Services,” Housing, and Non-Housing Core Services. And so hopes of an immediate Fed pivot, which have been bandied about really since June 2022, have now largely vanished. QT is running along on autopilot in the background, rates and inflation are on the higher-for-longer track, and for the first time in many years, stocks are on their own after having been babied by the Fed since 2008, and it’s not working out for them. Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|

Since QT started, stocks have been on their own, after having been babied by the Fed since 2008. And it’s not working out.

Since QT started, stocks have been on their own, after having been babied by the Fed since 2008. And it’s not working out.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)