Send this article to a friend:

August

06

2014

|

Send this article to a friend: August |

|

Oilfield Services: Poised to Outperform? One metric that shows why oilfield services have a secular tailwind is drilling intensity. That metric refers to a ratio between the total rig count and the amount of hydrocarbons being produced. (Oil and gas can be grouped together by calculating the total energy they represent as a "barrel of oil equivalent. As Schlumberger (NYSE: SLB) commented in 2011:

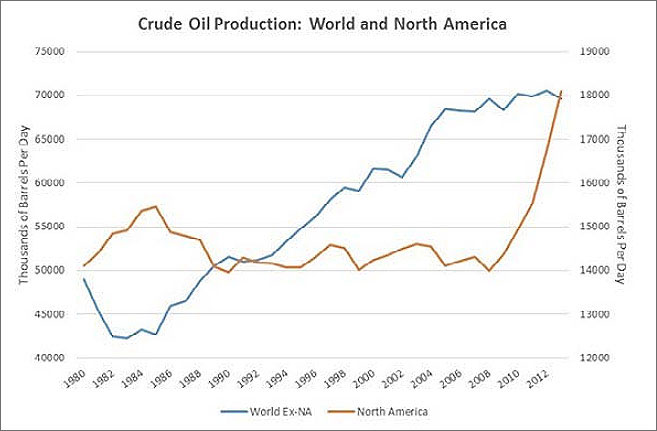

The driving factor is the plateauing of conventional production. To the right is a chart showing global oil production from 1980 to 2013, for North America and for the world as a whole excluding North America. Global production ex-U.S. is basically showing conventional production, since fracking techniques have not been widely applied outside the U.S. And global conventional production seems to be reaching a "bumpy plateau," marked by some geopolitical fluctuations, but with steeper growth in the past.

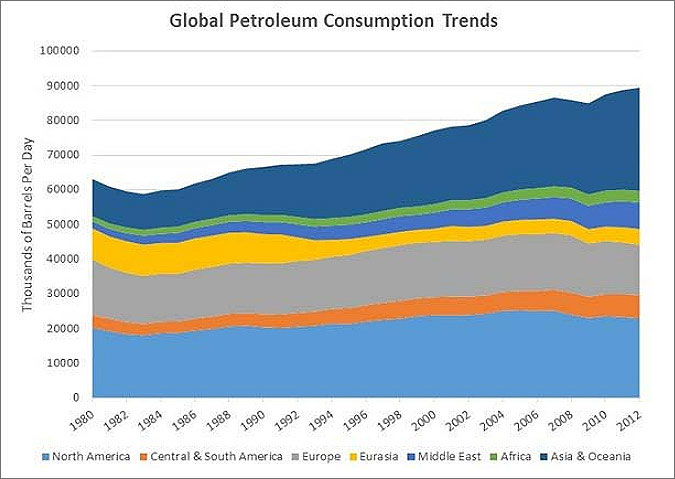

On the other hand, North American production is exploding — and it's unconventional production which is the driver. And the context within which these production trends are occurring is one of relentless demand growth: Demand is falling in North America and Europe, and rising dramatically elsewhere — with demand in emerging Asia being the standout. Putting the Pieces TogetherSo to sum up, we have a global environment in which (1) demand for hydrocarbon energy sources continues to rise dramatically; (2) production of conventional hydrocarbons is riding a bumpy plateau, and subject to various geopolitical stresses and risks; (3) incremental increases in production are likely to come almost entirely from unconventional sources; and (4) the dedication of resources to extraction, as measured by drilling intensity, is rising. With conventional sources unable to meet rising demand, unconventional sources will be required to take up the slack. And it takes more capital expenditure to exploit unconventional resources. That expenditure will increasingly be on technology, since it is technological progress and sophistication that are the most critical components of unconventional production growth. Petroleum Demand From Emerging Asia Will Drive Global Consumption All of this, we believe, is a secular argument in favor of the oilfield services companies that can demonstrate their ability to continue to innovate in unconventional extraction technologies — companies such as Schlumberger (NYSE: SLB), Halliburton (NYSE: HAL), and Baker Hughes (NYSE: BHI). Hydrocarbon extraction will be an ever-more critical component of the global economy; unconventional resources will be the key to production growth; and ever-greater capital and R&D expenditures on technology will be required. Further, as unconventional production moves into geographical areas outside the U.S., especially into China, the demand for the technology of these service providers is only set to grow:

Investment implications: Look for oil services companies with proven track records in deploying new technology and the ability to navigate markets outside the U.S., and consider adding to positions on pull backs. Our favorites for a buy, but only after they fall back at least 10 percent, are Schlumberger (NYSE: SLB) and Halliburton (NYSE: HAL), which is no longer a construction company, but is now a leader in oilfield technology. For more commentary or information on Guild Investment Management, please go to guildinvestment.com.

Mr. Guild is a recognized expert in the areas of international investing and economics. He has been a writer and speaker on economic issues for 30 plus years and has been widely quoted in the world media. He holds a BA in economics and an MBA with highest honors. |

|---|

Send this article to a friend:

|

|

|

The global revolution in oil and gas production that's been sparked by fracking continues to steam ahead - potentially with big benefits to the oilfield services companies who have the expertise that's needed to implement the technology and reap its benefits.

The global revolution in oil and gas production that's been sparked by fracking continues to steam ahead - potentially with big benefits to the oilfield services companies who have the expertise that's needed to implement the technology and reap its benefits.

Monty Guild founded Guild in 1971. Prior to founding the company he was an analyst at a bank and a hedge fund.

Monty Guild founded Guild in 1971. Prior to founding the company he was an analyst at a bank and a hedge fund.