Send this article to a friend:

July

12

2024

|

Send this article to a friend: July |

|

Why All Financial Markets Will Crash

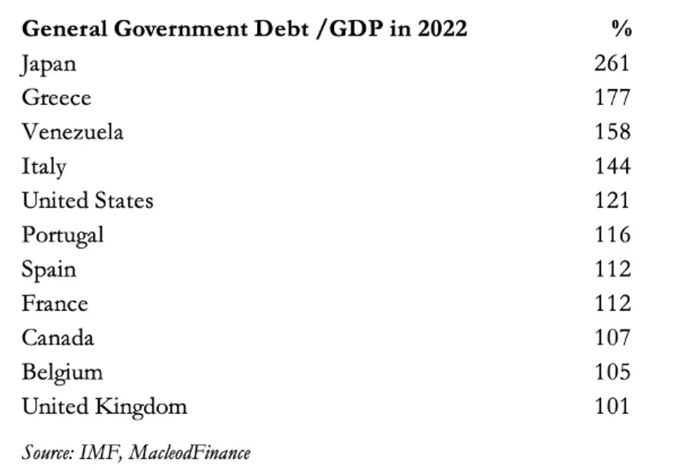

It’s all about credit All transactions and all valuations are in credit. The key aspect of credit is that it is always matched by an obligation, or debt. Credit is extinguished when that obligation is discharged or defaulted upon. But in today’s financial systems, the repayment of debt is always in another form of credit, usually the transfer of ownership of a bank deposit, which is also credit. Clearly, government and corporate bonds are debts. Because they are freely transferable obligations, they have a matching value expressed in credit. And that value is determined by both external influences and those specific to the debt obligation as assessed in markets. For example, interest rates and their outlook will place an external value on a bond, and additional factors specific to the issuer’s creditworthiness also apply. The credit status of bond ownership is unarguable. But there is widespread confusion over equity rights. Most investors believe that ownership of corporate equity is a hedge out of debasement risk of bonds. They believe that they own a defined portion of a corporation’s total property. This is not true, because a share certificate is an obligation of the corporation’s management to deliver or accumulate an income stream on a shareholder’s behalf: possession of a stock or share certificate is simply evidence of that obligation recorded in the corporation’s stock register. It is possession of a right to property, not ownership of property itself. Furthermore, with today’s dematerialised certificate system, unless you insist on taking delivery of your certificates, you don’t actually possess the evidence of your credit interest. Instead, you have an entitlement to a share of a corporation’s overall obligation to its shareholders. You are distanced even further from your property right, your property being simply credit squared. You might think that to eliminate credit risk entirely, you should buy physical property without mortgages. But here you run into a further problem, which is that there is no such thing as absolute wealth. This is because your ownership of property is valued by its exchangeability, for guess what: credit. When the ubiquity of credit in which all wealth is valued is understood, then it is logical that the value of everything depends on the balance of supply and demand for credit. The one exception is money without counterparty risk, which embodied in Roman law and the common laws of the Roman Empire’s successor nations and their colonies is gold, silver, and copper. Today it is primarily gold. But this article is not about these internationally accepted media of exchange. It is about the relationship between the value of credit, and the value of products and property expressed in it. From the foregoing, it is clear that all measures of wealth depend on credit, credit’s value, and its availability. The two principal forms of transferable credit are bank deposits, which are an obligation of a bank to its customers, and currency. The position of a currency must be clearly stated, because modern economists tell us that for all practical purposes, a currency is money. This is never true, not even if the issuer is prepared to exchange it freely for gold. A currency is an obligation of the issuer, today always a central bank, and the possession of a banknote is simply evidence of that obligation. It is recorded on all central bank balance sheets as such and possession of banknotes is simply credit. Furthermore, commercial bank deposits at the central bank, commonly referred to as reserves, are also recorded as a central bank’s liability to commercial banks. It is credit which ranks with banknotes. Economists and others make a gross error in arguing that a currency is not to be regarded as credit. This is particularly grievous in the case of the US dollar, which in the 1970s the US Treasury propagandised as replacing gold as the ultimate form of money. The dollar is the ultimate form of credit, maybe, but as freely admitted elsewhere its value remains dependent on the faith in and credit(worthiness) of the US Government. The value of credit We conduct our daily purchases and sales in credit, we pay our taxes in credit, and we account for all our commercial activities in credit. For all these purposes, we assume that variations in value are entirely confined in the goods and services being transacted, and that credit has a constant value. In reality, this is not the case. For transactional purposes, credit itself has value. It is traded for products and for other credit. For whatever reason, if the value of a currency declines, then it can only be stabilised by a rise in interest rates. Changes in a currency’s value can be detected either on the foreign exchanges or reflected in changes in the general level of prices expressed in it. Therefore, changes in a currency’s value have an obvious impact on interest rates, which reflect a combination of a market expectation of its future value compared with today’s as well as any counterparty credit risks. In addition to these factors affecting credit’s value, in terms of supply and demand credit is like any other product. An increase in supply will tend to lower interest rates, and a restriction of supply raises them. It is ignorance of this common sense that leads the vast majority of monetary commentators to believe that interest rates are set and can be managed by a central bank. Particularly in the current economic conditions, this error will prove to be extremely costly. To understand why, we should categorise demand for credit as emanating from two sources: governments and private sectors. Today, government debt is expanding rapidly in all the major jurisdictions, as the table below illustrates.

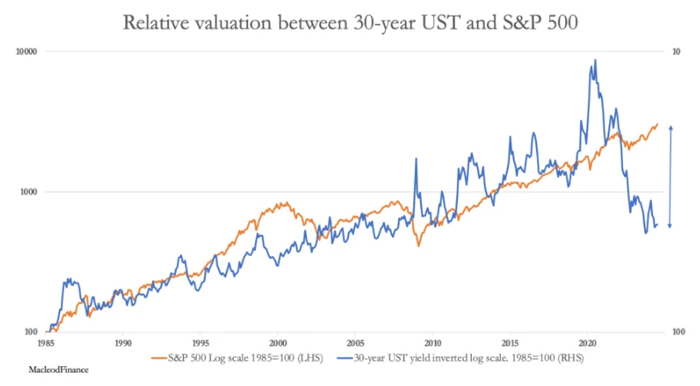

Two years on, the position today is generally worse for nations on this list. France, currently running a budget deficit of about 6%, has just elected a far-left administration which promises to increase the budget deficit materially. And the UK has similarly gone more socialistic, increasing the risk of sterling credit failure. Japan’s finances depend entirely on the Bank of Japan’s ability to suppress interest rates at or very close to zero without destroying the currency. But the central concern must be about the US and its dollar. US Government spending is out of control, with debt increasing at over $1 trillion every 100 days and accelerating. This must be financed. Bearing in mind that interest is not paid and that it is simply rolled up in additional debt, there can only be two outcomes, both leading to the same conclusion, which is higher interest rates. The US Treasury’s increasing demand for credit is currently being satisfied by credit supply being switched from non-financial private sector lending, because banks and shadow banks are reducing their risk exposure. This has led to an explosion in short-term Treasury debt, mainly bills maturing in up to one year. This liquidity is now running low, which is bound to lead to higher funding rates. Clearly, both foreign and domestic holders of Treasury debt will recognise a classic debt trap being sprung. The outcome could easily be interest rates rising to over 10%, perhaps 20%, unless the Fed reintroduces quantitative easing to contain funding costs. In this event, the increase in non-productive currency circulation will simply debase the currency, driving up the interest rate required to prevent foreigners selling dollars to stockpile gold, oil, and wider commodities. Without higher interest rates, the dollar’s purchasing power will be bound to fall, potentially spiralling into a state of collapse. The state of the economy is immaterial. The consequence of earlier QE policies was a fall in the dollar’s purchasing power, evidenced by a sudden rise in the general level of prices, and interest rates rising from the zero bound to current levels. With or without QE, US Treasury bond yields will rise and rise, which means that their values will fall and fall. The dollar is the yardstick from which all other fiat currencies take their value. The consequence of rising dollar interest rates will not only trigger severe difficulties for the US economy and therefore its banking system, but other currencies, particularly those representing highly indebted administrations will similarly be undermined. Consequences for financial asset values We can now see from our understanding of credit, and the consequences of risk factors on supply and demand for it, that markets will determine outcomes not central banks. Those who think otherwise delude themselves. They appear to think that a change in interest rate policy towards lower rates is inevitable. They ignore both the debt funding crisis for government debt, and the reduction of commercial bank credit availability for the non-financial private sector. Obviously, bond investors will face destabilising losses, which being driven by the declining value of credit links bond yields inversely to the general value of equities. My next chart shows how this relationship is already stretched leaving equities extremely vulnerable to interest rate disappointment.

By inverting the long bond yield (the red line, right-hand scale) the long-term negative correlation with the S&P 500 Index (blue line) becomes clear. The exceptions were the 2000 dot-com bubble, the 2008—2009 financial crisis, the various distortions of interest rate suppression and QE policies between 2012—2019, and zero interest rate policies over the covid crisis in 2020—2021. These aberrations can all be explained. But now the valuation optimism of equities continues despite the rise in long bond yields. Never has the disparity between long bond yields and the S&P 500 index become so stretched. It is over twice as much as during the dot-com bubble, following which the S&P halved. For equity investors, this is extremely dangerous ground, sustained only by the availability of credit predominantly supplied by commercial banks to the financial sector, which at the same time is starving the non-financial private sector of the credit it requires. Financial assets provide the collateral for most of the bank credit system. Much, if not most of that credit will end up being extinguished by defaulting obligations. This is why I have been saying the wisest course is to get out of credit and everything whose value depends upon it and into real money, which is gold. It’s not about gold rising, but credit in crisis or even collapsing entirely.

|

Send this article to a friend:

|

|

|