|

|

The Crude Oil Collapse Is Coming

To refresh everyone, as of May 14th this is what I had to say for prices through this time of year. Recall when reading my prior call that oil was trading just under $60 per barrel and was charging upward at a torrid pace. The run up at that time also had a gigantic tidal wave of bullish "green shoot" sentiment behind it. I said this:

Current Supply and Demand Forecasts Before continuing, here is a brief overview of what the most recent OPEC, IEA, and EIA announcements are suggesting and factually reporting. OPEC On Tuesday of last week, OPEC announced that it thought global oil demand would increase during 2010, an estimate which helped to lift the market. It is this same sentiment, along with increased prices, that gave OPEC countries an incentive to cheat quotas and (more on this in a minute) lead them to raise production in June for the third straight month. June production came in at 28.441 million barrels per day, a slight increase from the 28.402 million barrels just a month ago. Although this increase seems small, every drop of oil that hits the market matters when global demand is down as far as it is. Further, this shows that OPEC countries still cannot play by the rules, especially in a recession while prices are rising. In fact, they have an incentive to lead the market with improved demand forecasts. I wrote on this briefly in "Crude Oil, Opec, and Super Contango":

At present production compliance within OPEC is at about 68% which further begs the question, "How reliable are OPEC's forecasts?" IEA Broadly, on July 10th the EIA said that demand would decline by 2.9% percent in 2009; worse than previous estimates. However, in contrast to that estimate, they expect demand to increase by 1.4 million barrels per day or a 1.7% jump in 2010. As for supply the agency suggested that a supply crunch would come by 2014. The terms of this supply crunch would require global GDP growth of 5% from 2010 until then; this seems overly optimistic to me. The IEA also suggested that non-OPEC production would rise more than expected due to strong growth out of Brazil, Azerbaijan, Canada, and Russia. According to the report non-OPEC countries should account for 60% of global production, up from 33%, and will produce an additional 410,000 barrels per day in 2010. Lastly and I think most importantly, the IEA's David Fyfe said:

This is problematic for demand forecasts suggesting that 2010 demand will be much improved. EIA On July 15th, according to the EIA, US inventories were down more than expected and dropped by 2.8 million barrels. They also reported that distillate supplies rose 600,000 barrels and that gasoline supplies rose 1.5 million barrels. This is good news for crude oil producers and refiners, but bad news for shipping companies and the overall market. A lot of what has occurred here is a shift of where oil is stored and the form that it is stored in. The EIA, on July 7th spoke on demand and rose estimates that it would increase slightly in 2009 and climb 170,000 barrels per day to 83.68 million. Although they pointed out that this was still well below 2008's 85.41 million BPD consumption. They also touched on 2010, and suggested oil demand would increase by around 1 million barrels per day globally to 84.79 million. After reviewing supply and demand estimates and reviewing my thoughts from May this is where I think oil is headed during the next 3-6 months. The Unwind of "Super Contango" Several months ago I wrote about contango and what was happening in the oil market. At that time I said this:

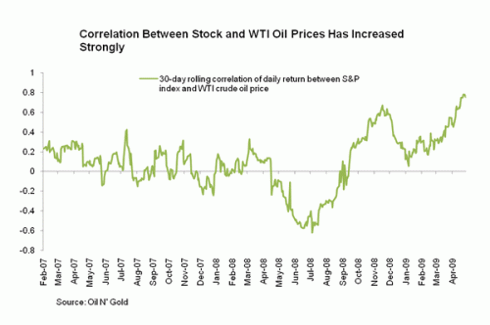

Currently contango is starting to unwind as spreads are narrowing on oil trades of this type. In addition, in order to become more profitable (or to try and offset tremendous credit losses) financial institutions are increasingly turning to trading profits. Where do most of these profits come from? You guessed it, trading speculation from the Treasury and Oil markets. This can be readily seen when evaluating the earnings reports for CitiGroup (C), JP Morgan (JPM), Goldman Sachs (GS) and/or any other major finance company over the last week. The capitalization of trading profits on oil trades, in conjunction with rising distillate and gasoline supplies, points to the start of an unwinding of contango. It also suggests that bank speculation is less likely to lead oil higher as it had over the past several months. Extreme Correlation At the time that I wrote my original article, oil to stock market correlation was at an all time high. To illustrate this I included this chart:

Since that time the equities markets and the oil market haven't decoupled, in fact just the opposite has happened. Now, rather than just oil and equities being coupled, the entire global financial marketplace has become more correlated than ever before. On June 30th Bloomberg wrote this:

To point more specifically at the correlation between equities and oil, on July 8th, 2009 the S&P 500 index and crude oil had a correlation coefficient of .68 according to Bloomberg. This high level of lockstep movement was only slightly under the all time high for oil and equities of .74 which occurred on June 22nd of this year. This to me is incredibly problematic as the equities markets are far from being at full strength. At this time, due to this close knit relationship of the broad financial markets, any hiccup anywhere could very easily be detrimental to all asset classes. In more layman terms, with correlation like this there will be no refuge for anyone trying to diversify a portfolio. As is frequently said, "The market under its current conditions is priced for perfection" and that also does not bode well for the outlook of oil through the end of this year. Add to this the current state of unemployment around the world; the lack of real signs for a housing recovery in the US, and the tremendous amount of global deleveraging which is still required and oil has an even bigger problem. Although deleveraging has been occurring for some time now, more is required before the globe can escape the Great Recession. Deflation Deflation seems to be here, although whether the US government embraces it or not is another story. Again I wrote on this point in "Hyperinflation Is Not Coming:"

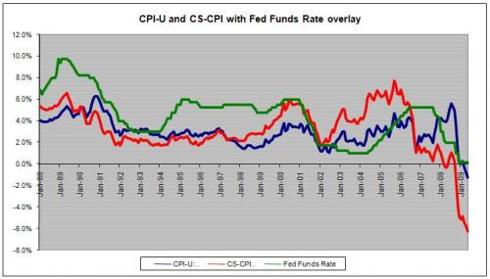

As of today, banks still aren't lending as evidenced by the earnings reports above, credit losses continue to mount at an alarming rate (don't forget they would be worse if it weren't for accounting adjustments to charge off dates as well as the continued suspension of mark to market), and sales of nearly everything (except retail gasoline and cars) have continued to fall. Yes, it is true that CPI was up 0.7% this time around. However is it any wonder that this occurred when two of the major components in the index are non-adjusted retail gasoline receipts and deeply discounted, government assisted, "going out of business-cash for clunkers" auto purchases? In fact in the CPI report, if gas sales were taken out of the index prices moved up only 0.2%. Gee I wonder what happens if we take out auto sales? Under that scenario it is easy to argue that prices didn't climb at all. So if government based CPI doesn't cut it what's better? Case Shiller CPI or CS-CPI: Lastly, on the point of deflation, there has been a dramatic change in consumer attitudes towards spending; this is illustrated in the chart below. Before continuing, note the decrease in savings rate that occurred during US growth periods; note also the stupefying fact that there are periods of actual negative savings rates!

All in all this irrational thought process and the fact that the economy in the US is deflating are also not good signs for oil. Finally - Where Does Oil Go From Here?Throughout the next several weeks I expect to see oil stay in the $65 to $70 per barrel range. Towards the end of August and into the beginning of September I expect more and more people to begin seeing China's current expansion as the beginning of a new credit bubble. I then expect people to realize how irrational equity and commodity pricing has gotten during the most recent run up. At this time I believe people will also recognize that the Chinese have been stock piling commodities on a stimulus lead lending binge. After all of these realizations the market will begin to see that real global demand is much weaker than once thought. As usual, this realization will begin to erode demand forecasts further which will trigger market fear and drive speculative bulls out. Bluntly, I expect to see the "green shooters" go into a panic and flee oil as they did in late 2008 and early 2009. During this period it is also likely the public will start to push back against "green shoots" and realize that they were duped by misrepresentations about the economy. This will further erode already weak consumer demand as those with jobs will be even more afraid of losing work. Individuals will retrench even deeper either by choice or by employment loss and the Great Recession will officially become a depression. These factors will be enough to push the globe towards the double bottom, long slow road to recovery that very few are pointing to at this time. During this period I expect that oil will begin its move downward and should trend towards its previous lows of late 2008 and early 2009 near the $30 per barrel range. When the realizations above become a reality, by early to mid 2010, rather than trying to determine where the recovery started, economists will once again be searching for a bottom. Eventually the deflation that is here will be embraced, as people realize no amount of government spending will create a recovery. At this time the final leg of deleveraging will have to occur as public favor and treasury money runs out. The pain will be deep, and many companies and people will suffer as cheap, easy, loose, or whatever you want to call it, credit is absolved from the system. Only after this shake down will the economy be able to slowly bring itself back to health. All in all it does not seem wise to expect a sharp run up in oil prices until deleveraging is allowed to occur. The next run up will likely not be driven by global growth as the world's current capacity was largely able to handle peak credit demand. A run up will however occur on the back of supply shortages. Lost oil capacity stemming from the great recession and its toll on the energy industry should be the next driving force behind oil. A lack of investment into exploration and capacity during the downturn will coincide with the IEA's forecast of a supply crunch, but I think the crunch will come after 2014. Since I expect a long slow recovery it is not likely demand will outstrip supply in the next several years. However, when this occurs, it is very likely we'll see $100+ oil again.

James Bibbings is an associate editor at Commodity News Center ("CNC"), a website which focuses on providing the latest commodity news and analysis. In addition to this Bibbings is also the president of Hugo James Consulting; a firm which specializes in offering compliance solutions to the brokerage industry. Prior to joining CNC, James worked for the regulatory agency that monitors commodity futures and OTC currency trading within the United States. From there he worked on an electronic currency dealing desk at the Chicago Board of Trade, and eventually helped to create a commodities brokerage in late 2008. Mr. Bibbings writes daily as the "Economic Bibb" for Commodity News Center and through his writings strives to provide a unique outlook on the economy, the financial markets, and the global political landscape.

|

|

|

On May 14th I wrote an article called "

On May 14th I wrote an article called "

I have written on Case Shiller and Owner's Equivalent Rent in the past. I have also touched on the US governments take on CPI previously and why it's flawed. Today I'll leave those two points alone. Instead today I want to direct you to

I have written on Case Shiller and Owner's Equivalent Rent in the past. I have also touched on the US governments take on CPI previously and why it's flawed. Today I'll leave those two points alone. Instead today I want to direct you to  Regardless of what is being said about consumer driven economies, it is good for Americans to save. In fact, the only really good economic news I’ve seen lately is that US households are saving

Regardless of what is being said about consumer driven economies, it is good for Americans to save. In fact, the only really good economic news I’ve seen lately is that US households are saving