Send this article to a friend:

June

07

2024

|

Send this article to a friend: June |

|

Mortgage Rates Rise, Over 7% since Early April, Buyers Remain on Strike,

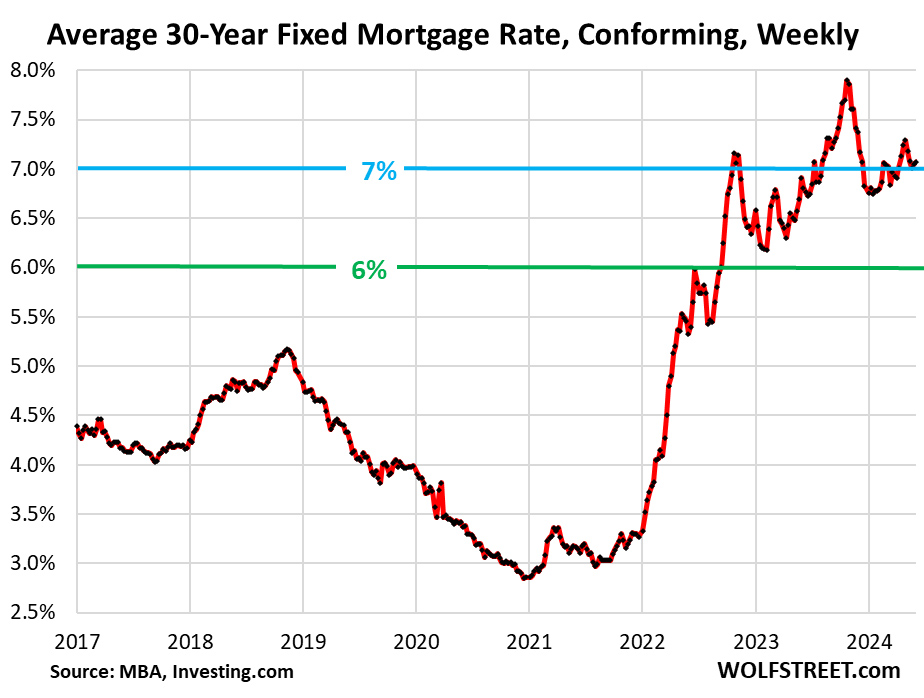

The over-7% mortgage rates seem to have become a fixture in the housing market. The average conforming 30-year fixed mortgage rate edged up to 7.07% in the latest week, and has now been above 7% since early April, according to the Mortgage Bankers Association today. During Rate-Cut-Mania, the average mortgage rate had dropped to 6.76% at the low point in early January. These mortgage rates are not high compared to the pre-QE era. From 1970 through 2001, mortgage rates ranged from 7% to 18%. What was different then that allowed those rates to function were the lower home prices. When mortgage rates dropped below 7% in 2002 and eventually as low as 5.5% in 2005, they fueled Housing Bubble I, which led to the Housing Bust from 2006-2012. So these 7% rates are fairly healthy rates:

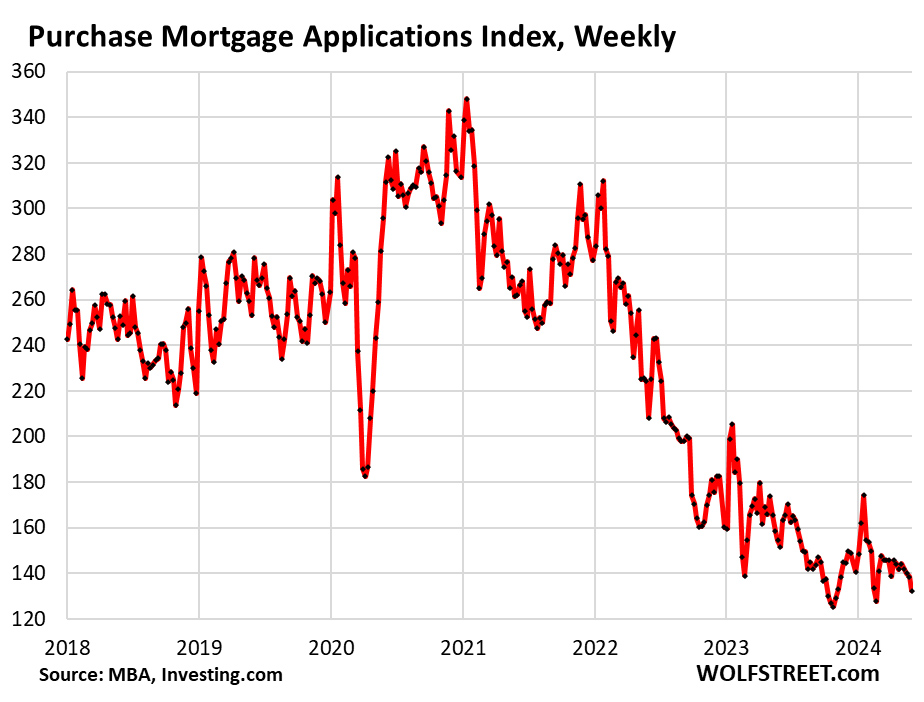

Stuck with a 6% or 7% mortgage that was supposed to be refinanced? Mortgage rates have been above 6% since September 2022. But no problem, the real-estate industry has been telling homebuyers that they should buy now even at these rates because they will be able to refinance at a much lower rate shortly, after the Fed starts slashing interest rates. Meanwhile, there still haven’t been any slashed rates. Instead, recalcitrant inflation in the US has caused the Fed to backpedal on the three rate cuts in 2024 that it has seen as possible in December 2023. The economy is humming along, the labor market hasn’t yet collapsed or whatever, and there really isn’t anything “forcing” the Fed to cut rates. These new homeowners may feel kind of stuck with their 6% and 7% mortgage rates, and their big mortgage payments that may force them to cut back spending on other stuff. But the Fed is counting on them. They’re one of the official transmission channels of Fed policy, via higher interest rates to lower demand in the economy, and thereby to lower inflation. So they’re carrying the Fed’s water in trying to get inflation down. Home sales still frozen; prices are too high. Mortgage applications to purchase a home dropped further in the latest reporting week and are just a hair above the record lows in the data going back to 1995. The records were set in November 2023 and February 2024. The mini-spike of Rate-Cut Mania has by now completely worn off. How far mortgage applications to purchase a home have plunged from the same week in the prior years:

Volume of closed sales of existing homes in April had dropped by 26% from April 2022, by 30% from April 2021, and by 24% from April 2019. Volume of pending sales in April, an indicator of closed sales in May and later, dropped 7.7% from the prior month and by 7.4% from the already beaten down levels a year ago, according to the National Association of Realtors last week.

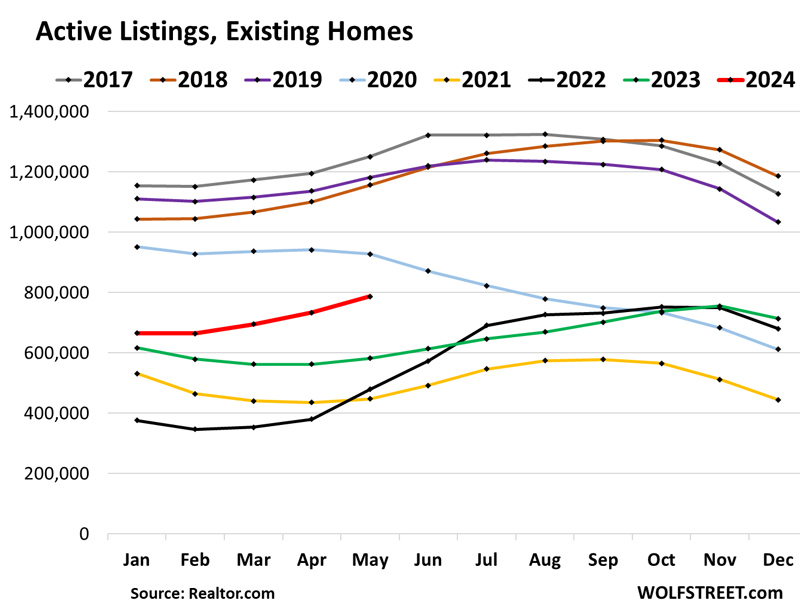

Supply is already increasing. Active listings in May rose to the highest for any may since 2020, according to Realtor.com:

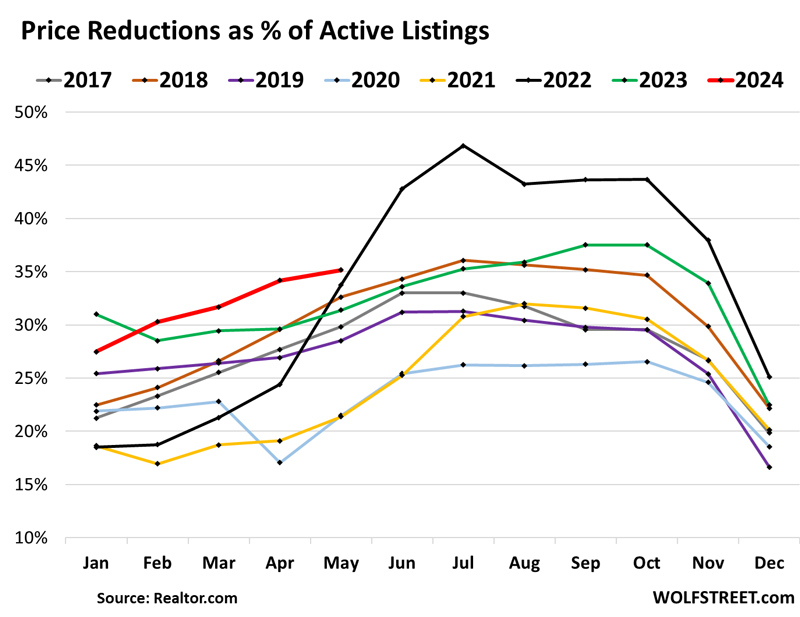

Price reduction rose to the highest for any May in the data by Realtor.com going back to 2017. Price cuts are a first sign that the housing market may be thawing out just a little, but it will take a lot more than cutting exaggerated asking prices a little bit. And for now, the housing market remains frozen because prices are still too high, keeing many potential buyers on strike. And some of them have figured out that they can rent a nice house for a lot less on a monthly basis than buying at these sky-high prices:

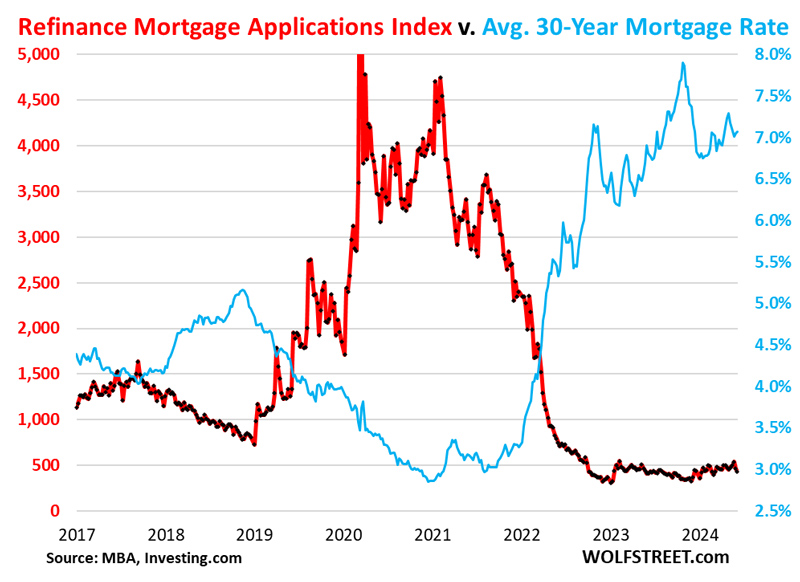

Mortgage applications to refinance a home without cash-out have nearly vanished. The refis that are still taking place are mostly cash-out refis. In the latest reporting week, total refis dropped further and were down by 85% from the same week in 2021 and by 67% from the same week in 2019, having squiggled along historic lows since August 2022. Refis are dependent on low and falling mortgage rates. They had seen a historic boom during the 2.5%-3.0% mortgage-rate era, and in the months as mortgage rates began to rise in the fall of 2021 and early 2022, after the Fed started talking about rate hikes, the end of QE, and eventually QT. And then refis died.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|