Send this article to a friend:

June

06

2024

|

Send this article to a friend: June |

|

Corrupt Inflation Reporting Damages Social Security

In previous articles, we’ve covered the topic of “why Social Security’s cost-of-living-adjustment (COLA) isn’t a raise.” In those installments, we also revealed why the COLA never seems to keep up with the official inflation rate, no matter how much it’s adjusted. For example, according to a recent Motley Fool update:

Since July of last year, the monthly CPI (consumer price index) rate has been reported between 3.1% and 3.7%. That means higher prices have already “eaten up” every bit of the COLA for 2024 (only 3.2%), and then some. In addition, the official CPI rate hasn’t dipped below 3% in 2024 in any month. So if the SCL estimate revealed in the above quote ends up correct, the COLA still won’t be enough to account for overall price inflation in 2025. That’s because any personal wealth that is stolen by inflation can never be recovered. With all of that said, it’s quite possible the situation is much worse than I thought. The COLA offered by the Social Security Administration each year could be completely flawed, and isn’t capturing true cost-of-living increases at all… Why official inflation reports are misleading (at best) Whether Federal Reserve Chairman Jerome Powell chooses to talk about the “Core PCE” or the “CPI” when he is reporting on inflation, he could be misleading the public. That’s because the calculations appear to be flawed from the beginning. According to a March report from Geopolitical Intelligence Services (GIS):

The big problem with this calculation is, if the quality of an item in the fixed basket of goods goes up, Fed statisticians can decide it actually costs less:

Wolf Richter does a great job explaining how this works. To summarize, this is why the top-selling light truck and sedan in the U.S. have prices significantly than the CPI would lead you to expect:

Misleading? Absolutely! Dishonest? I think so. Either way, you can see how this sort of statistical jiggery-pokery can camouflage price increases. And there’s more! “Hedonic adjustments” don’t offset higher prices enough to make the data look pretty? Don’t worry – the Fed statisticians have another trick up their sleeves!

In other words, the Fed could simply conceal the actual cost increase of any essential item just by changing its relative importance. And then there’s outright substitution. John Williams explains:

Even with all these tricks up their sleeves, the Fed’s analysts missed one really big cost… A look into the economist’s blind spotOnce upon a time, inflation was considered a public menace. Now it’s just considered a political hot potato. Former Treasury Secretary Larry Summers revealed yet another critical piece missing from the Fed's inflation calculations. He set out to discover why inflation feels so much worse than the official reports – and here’s what he found:

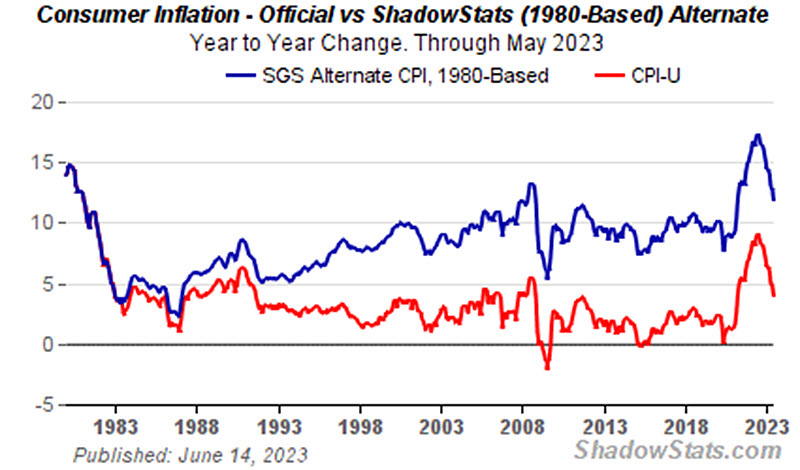

Makes sense, doesn’t it? When the average American owes “$104,215 across mortgage loans, home equity lines of credit, auto loans, credit card debt, student loan debt, and other debts like personal loans,” interest rates matter. When the Federal Reserve raises interest rates to fight inflation, that also raises the cost of money. It’s truly staggering that the Fed completely ignored this for the last 40 years. But it helps to explain one glaring reason why, as we’ve summarized again and again over the years, the official inflation rate simply doesn’t match reality. You can see the real inflation rate below (blue line), as compared to the officially reported inflation (red line) that Chairman Powell and President Biden would like you to focus on:

via ShadowStats Forget about hedonic adjustments and how you weight peanut butter vs. gasoline in your CPI basket. The real inflation rate is running over 10%! Doesn’t that feel more accurate than the official 3.4% to you? Are your own, personal expenses rising at a rate closer to 3.4% or to 10%? Side note: In the chart above, see where the two lines diverge, right about 1983? By the same methodology used in the early 1980s, that was the moment government statisticians started lying with inflation statistics. That’s the moment inflation stopped being an economic indicator and turned into a political weapon. All this nonsense has effectively poisoned any asset that’s indexed to inflation. The poisonous fruit of the poisonous tree In the U.S. court system, prosecutors have to contend with an idea called the “fruit of the poisonous tree.” Here’s how it works: Any evidence obtained illegally is inadmissible in court. If the tree is poisonous, then its fruit is poisonous as well. Obviously, this can hamper or destroy a prosecutor’s case – even if they weren’t involved in planting and watering the poisonous tree. So now let’s apply this same idea to official inflation reporting. Because our current inflation indexes are flawed and massively underreport our true cost-of-living increases, everyfinancial asset that incorporates this metric is also flawed. The most obvious example is Social Security COLA adjustments. (But every “inflation-indexed” financial asset from Series I savings bonds to inflation-indexed annuities suffers the same obvious shortcoming!) The bottom line: You cannot rely on inflation-indexed assets or on Social Security benefits to keep up with cost-of-living increases. Take a moment to consider various inflation-resistant investments to protect your standard of living over the long term. I also hope you’ll take a few minutes to learn more about the benefits of owning physical precious metals. Owning physical gold, for example, has historically proven to be an excellent form of inflation protection. See, real assets like physical gold and silver aren’t “indexed” to anything except supply, demand and dollar purchasing power. Those aren’t numbers the spreadsheet wizards at the Bureau of Labor Statistics, the Bureau of Economic Analysis or even the Federal Reserve can tamper with.

|

Send this article to a friend:

|

|

|