A Gold Bug vs. Washington D.C.: Judy Shelton on the Fed, Gold

and Monetary Policy

Mike Maharrey

Judy Shelton isn’t your typical Washington insider.

Sure, she’s advised presidents and rubbed shoulders with the likes of Paul Volcker and Alan Greenspan. She was even nominated to serve as a Federal Reserve governor. But there is one big difference between Shelton and your typical D.C. monetary policy wonk. She’s a “gold bug” who believes in sound money.

Shelton recently joined Gold Telegraph Alex Deluce for a wide-ranging conversation about the future of monetary policy.

Historically, monetary resets have occurred due to wars. Shelton said there is a better way.

“Could we have a monetary reset without war? That to me seems the logical way to do it and without revolution, but it's going to take sort of a revolution of principles among the people to say we actually demand a dependable unit of account.”

Shelton said she believes gold offers the best path forward when it comes to a sound monetary system.

“I wish we had a neutral reserve asset like gold, something universally recognized, something that's had constant purchasing power over centuries. The beauty of gold is that it provides a reference point independent of the government. Money is meant to serve as a reliable measure. It's supposed to be a dependable store of value.”

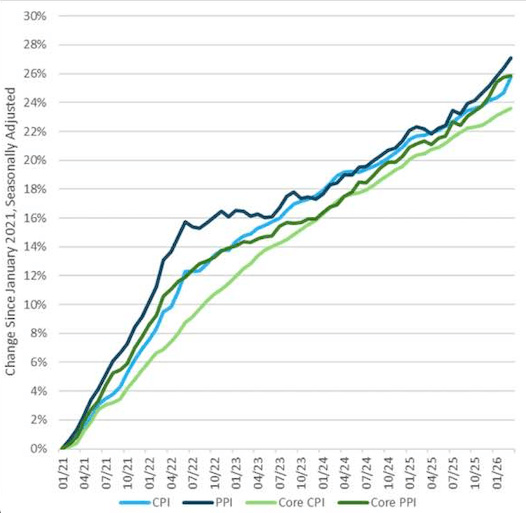

The dollar is anything but dependable. The government devalues the U.S. currency by 2 percent every year as a matter of policy. That’s a 10 percent reduction in the dollar’s purchasing power every five years. And in practice, the dollar is losing value even faster than that. The post-COVID inflation surge provides a case in point. Since January 2021, price inflation has risen between 23.6 percent and 27.1 percent, depending on which metric you choose to use. People are starting to pay attention, and some are starting to question the future of the dollar.

People who support sound money and a gold standard are derisively called “gold bugs.” Economist John Maynard Keynes famously called the gold standard “a barbarous relic.” But Shelton said it seems like the perception of gold is starting to shift in a positive direction.

“The interest in gold, the amazing run up in the price of gold denominated in every currency, would seem to indicate that people are losing faith in fiat currencies. Maybe they don't trust governments to maintain a store of value that's meaningful, that's trustworthy. So, I definitely think there's a strong correlation there, and I hope it's indicative of people saying, ‘I'm not satisfied with money that loses value. And I almost demand a unit of account that's meaningful and dependable.’”

Shelton cut her teeth studying the internal monetary and financial system of the Soviet Union. She quickly came to the conclusion that Soviet central control would eventually collapse the economy.

“I saw what government can really do to turn the money into what came to be called by Soviet citizens ruble trash.”

Ironically, Nixon is the president who ultimately cut the final tie between the dollar and gold when he ended the convertibility of dollars to gold in 1971. When Shelton told Nixon that she was planning on writing a book about the Bretton Woods system (which Nixon ended), he came back with a shocking response.

“I thought, maybe he'll tell me something of his thinking. And what he wrote back was maybe more interesting. He said, ‘I know very little about monetary policy.’ And I thought, and yet he's the one who ended that system.”

Shelton said in another letter, Nixon confessed, “I'm not sophisticated enough on monetary matters to comment on your proposals.”

Shelton said Nixon had a good grasp of economics, but he was advised (poorly) when it came to the intricacies of monetary policy.

During a national television address, Nixon promised the closure of the so-called “gold window” would be temporary to “defend the dollar against the speculators." He also said, “Let me lay to rest the bugaboo of what is called devaluation,” and promised, “Your dollar will be worth just as much as it is today.”

Shelton said the move fundamentally changed our money.

“Americans were kind of told, ‘Oh, don't listen to these rumors. It may cost you a little more to travel in Europe,’ I think is the way Nixon said. ‘Some things may seem a little more expensive, but we're going against the speculators.’ He called them the currency speculators, which were probably the same people who were saying, ‘I'd rather have the gold.’”

Shelton also developed a professional relationship with Paul Volcker. As Fed chair, Volker famously cranked interest rates to 20 percent to tame the rampant inflation that raged out of control after the last tie of the dollar to anything was severed. Shelton taped a three-hour conversation with Volker, who was present when Nixon gave his order and initially supported the move.

“Paul Volcker on the sidelines in between taping would say, ‘I never meant that to be the outcome.’ He said, ‘I thought we needed to temporarily close the system because we had inflated so much to finance both the Vietnam War and new entitlement programs that we had exported inflation around the world, and those countries were now demanding that we redeem US dollars at the old $35 per ounce of gold convertibility rate, which was inherent in the Bretton Woods agreement.’ And he said, ‘I just thought we might have to go to $38 or maybe even 40.’ But he said, ‘Then I thought we would reinstate what was essentially the system that he said everyone at Treasury believed in.’"

Of course, that never happened. We ended up with a free-floating currency that the government could inflate at whim to fund its ever-growing welfare/warfare state.

As Deluce put it, the U.S. effectively traded discipline for “flexibility” in its monetary system.

“In a way, that flexibility is kind of a weasel word that can sound good. I mean, the governments like to say we need the flexibility, but what it really means is the flexibility to not be disciplined, and then that translates into the flexibility to reduce purchasing power, to incur inflation, to debase the currency, to carry out some other goal the government deems as being important. And that's when you reduce money to being just another economic variable to achieve whatever government objective they think is in the interest of government.”

Shelton believes the objective should be simple – preserve people’s earnings.

“When someone earns money, that's like property. And in fact, James Madison argued that a depreciating currency is the same as stealing property and therefore unconstitutional. He considered it government expropriation.”

Shelton argued that a common global currency would be ideal.

“We should all use the same unit of account for cross-border. Why would you have exchange rates moving around? People complain about tariffs, but tariffs have a minor impact on relative prices compared to exchange rate changes. At least Paul Volcker always thought that. He said, ‘You could work two years to get a tariff whittled down one or 2 percent.’ And he said, ‘And you could lose all that in 10 minutes of trade on foreign exchange markets.’ So, I think that's very important to bring back.”

Shelton said talk of a common currency may sound futuristic. However, it’s really “retro.” For hundreds of years, gold and silver served as a common currency. Many people are coming back around to this idea because there is a growing desire to “decentralize finance.”

“What does it mean, this attention to gold around the world? What does it mean that China is accumulating gold and silver? What does it mean that other countries have asked to have their gold repatriated back from the basement of the New York Fed? I think it shows this declining faith in government-issued currency and a desire to have a reserve asset that is more dependable.”

Shelton has advocated remonetizing gold through a long-term gold convertible bond.

“I tried to come up with an idea to start moving toward honest money, to start getting back to some kind of a gold link for U.S. currency, because I think that it performed in a more stable way when we had some kind of gold link between the dollar and gold. And so, I've suggested the treasury should issue a long-term gold convertible bond, where, at the option of the bondholder on maturity, you could redeem either a pre-established amount of gold or at the nominal value, the face value denominated in dollars of the instrument. But where I think this could be particularly interesting would be we see stablecoins moving forward. Stable coins are one-to-one backed by the collateral, which can be gold, it could be readily marketable securities, most likely treasuries. I think it would be very interesting to launch stable coins that were backed, let's say you had one exclusively backed by gold convertible treasuries, and I've said a solidus to invoke both, I think it's from the Byzantine period, the currency that was ... It was around the world.”

President Trump nominated Shelton for the Federal Reserve Board during his first term. She was quickly marginalized as a “gold bug.” As Deluce explained it, “The Washington machine built explicitly to protect politicians' ever-growing spending demands quickly closed ranks.”

“I couldn't believe it. And I sent, I had a wonderful friendship with Alan Greenspan, and I would email him some of these articles. And I remember one where he wrote back and said, ‘If gold is such a worthless medal, why does the US government and every other major government keep so much of it?’ And so, I felt reinforced by that, but I was amazed at the power of pundits, who I knew didn't know as much as I knew about monetary systems and history, or the fact that both Volker and Greenspan had great respect for the role of gold as a bulwark against runaway money. So, it was difficult. I had a hard time understanding that.”

Shelton is not shy about criticizing the current Fed chair. Although she was more diplomatic, she essentially called Jerome Powell’s handling of the “transitory” inflation in the post-pandemic years incompetent. While he played lip service to accountability, nobody ever took responsibility for the debacle.

“He repeatedly said, ‘Price stability is the responsibility of the Federal Reserve.’ Well, we didn't get price stability. We still don't have it. Yet he not only never apologized, but he refuses to resign. And I think that's outrageous, and it's cheap grace to say, ‘You take responsibility and nobody gets fired.’”

Shelton said now is the time for substantial reforms at the Federal Reserve. In fact, it almost sounds like she thinks we could do without the central bank’s constant tinkering with the monetary system and the economy.

“I think there's been great dissatisfaction. Inflation continues to be a lead issue for people. And I think the focus on the Fed, the constant presence of the Fed is sort of, for me, it's kind of an irritant. I don't think they should have this massive footprint, and where people make financial decisions by first weighing in on what the Fed might do, 25 basis points up or down. And now there is, in a way, we're addicted to that. I sometimes think if we ended the Fed, I don't know what all of these armies of analysts and commentators, what would they do? But we'd have a healthier economic system if people could just take for granted that the money is not going to depreciate, that a unit of account can figure into your planning for your whole future, and that you're not just trying to keep up constantly with inflation and forced to put your money at risk. I think that would be a much better world.”

Shelton said the bottom line is: “We need to guarantee honest money.”

“I think what's at risk is this sense of people increasingly that they are victims of monetary favoritism, that the Fed maintains policies that increase the inequality of wealth and income, that they reward people who are already wealthy enough to have financial assets. I think we need a revolution of valuing honest work, honest government, and honest money. And by that, I mean, celebrate people who actually make goods, who produce goods and services, not just people who arbitrage the anomalies of financial markets. I think we have to insist on honest government. I think deficit spending is unacceptable. That's immoral because you're robbing from future generations, you're putting liens on goods that have yet to be produced, and it just enhances the likelihood of ever-increasing government.”

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

Judy Shelton isn’t your typical Washington insider.

Judy Shelton isn’t your typical Washington insider.