Are Stocks about to Crash?

David Haggith

Sure the Nasdaq just soared above 17000 for the first time in its history today, even though the Dow fell by 200. However, for a number of reasons, the long delirious US stock market finally looks poised to fall this summer if not sooner. Most of the recent rise, of course, has been due to Nvidia and the AI craze, while the rest of the market is not looking nearly as strong. 350 stocks in the S&P 500 went down today, meaning there wasn’t broad participation in the rise. Hence, the tech-heavy Nasdaq is roaring while the Dow is falling. Sure the Nasdaq just soared above 17000 for the first time in its history today, even though the Dow fell by 200. However, for a number of reasons, the long delirious US stock market finally looks poised to fall this summer if not sooner. Most of the recent rise, of course, has been due to Nvidia and the AI craze, while the rest of the market is not looking nearly as strong. 350 stocks in the S&P 500 went down today, meaning there wasn’t broad participation in the rise. Hence, the tech-heavy Nasdaq is roaring while the Dow is falling.

So, let’s take a look at the several signs that say this unhealthy or unbalanced market may be getting ready to tip over at last.

The Hindenburg Omen Let’s start with the ominously named “Hindenburg Omen,” which was triggered last week. Granted, it has a spotty track record for something with such an impressive name, but here is what Investipedia says about the omen:

The Hindenburg Omen is a technical indicator that was designed to signal the increased probability of a stock market crash. It compares the percentage of new 52-week highs and new 52-week lows in stock prices to a predetermined reference percentage that is supposed to predict the increasing likelihood of a market crash.

Even though the market tipped past that point last week, this indicator of a major market change is not always correct, but it’s one pretty solid weight to put on the “market going down” side of the scale.

Given the inherent upward bias that is built into most stock markets, any occurrence that is abnormal usually leads to a flight-to-safety response from investors. This facet of investor psychology is, arguably, the single most relevant factor that leads to precipitous market declines, or market crashes.

The Hindenburg Omen looks for a statistical deviation from the premise that under normal conditions, some stocks are either making new 52-week highs or new 52-week lows. It would be abnormal if both were occurring at the same time.

According to the Hindenburg Omen, an occurrence such as this is a harbinger of impending danger for a stock market. The signal typically occurs during an uptrend, where new highs are expected and new lows are rare, suggesting that the market is becoming nervous and indecisive, traits that often lead to a bear market.

Without going into greater detail on the calculations, the indicator says investor sentiment is looking “shifty.” It may not turn, and it’s not a measure you’d rely on by itself; but investors are looking uneasy according to this measure.

Stocks back in bondage

Even with all the help Fed Chair Jerome Powell has given to jawboning Treasury interest down in order to help his friend Treasury Secretary Janet Yellen out, bond yields rose again today for the fundamental reasons we’ve been talking about of over-supply in the face of weakening demand as the government debt towers.

That took the 10YR back above the 4.5% yield level where it just starts competing against stocks. Stocks fell today right as bonds rose. Of course, we’ve seen things in this stock market don’t get really serious until around the 5% level, but the reason for the yield change is serious. Today’s Treasury auction of 10YR bonds met particularly with weak demand.

It also didn’t help stocks that the fantasy that drives investor mania right now took another hit by a Fedhead today as Minneapolis Federal Reserve President Neel Kashkari said he wants to see “many more months” of data pointing to easing inflation before cutting rates.

I’ve been pointing out how a number of Fedheads have been making that point, but the market keep hearing “months more data before we’ll even consider a cut” as meaning “2-3 more months of data”—the smallest number of months that the plural form of the word can mean. So investors have been pricing for September, while I have been saying I am certain the Fedheads mean something more like, “It sure isn’t going to happen this year.”

As I pointed out in an editorial last week, the Fed has seen many months of inflation creeping up in the data (more if you looked under the hood), and that hasn’t caused it to raise rates, so it will certainly want to see many months of inflation going back down again in the data to become convinced the uptrend is firmly stomped out. However, the market has been interpreting the Fed based on wishful thinking, not sense or context. Here is what I wrote last week:

You don’t lower rates when inflation is consistently rising month after month! In fact, those rising months mean it will take many more consecutive months of falling again before you finally find the confidence to say, “OK, I guest that’s over. We can start moving back to normal policy rates.” (See: “The Market Knows What it Knows but Doesn't Know a Darn Thing.”)

The Fed’s Kashkari finally came along today and spelled it out just like that, and then …

He also said he would not rule out further rate hikes if price pressures tick up again.

Stock investors keep hearing that, too, but they keep blocking it out and settling back on what they want to believe, which is never going to happen for the clear reasoning just given. It makes no sense. However, Powell seems to want to keep luring markets with that false hope, and the only reason I can think he’d do that is to help the government fund its debt, which means Powell is fundamentally putting the government debt ahead of inflation right now, which means inflation is likely to go back up quite a bit. He’s back to hoping the present rise will prove to be transitory, which makes him the greater fool.

So, while the market got a little dose of sense today, let’s not get too far ahead of ourselves, Powell will likely do his best to keep 10YR Treasury yields out of the 5% clouds, even if it kills his inflation fight, and investors will likely do their best to keep finding a way to boost their abstract hopes back up based on any fume of hope Powell gives, though the Hindenburg Omen indicates they may be getting a little edgier now. A lot may ride at this possible tipping point on whether Friday delivers us goldilocks numbers on PCE inflation and on revised Q1 GDP.

Bill Bonner would agree with me on this one:

On the surface, the Fed is four-square, dead-set against inflation. It will swear upon a Trump Bible that it intends to get the CPI down to 2%, and that it will look neither to the right nor to the left until the job is done….

The US economy doesn’t need cheaper credit. Just the opposite; it could use higher interest rates to lower inflation. As it is, consumer prices are still going up at about two times the Fed’s target….

[However,] at a uniform 5% interest … America would need to use almost 20% of its GDP just to pay interest... while swindling the next generation by leaving the principal amount unpaid….

Mathematically, the US could pay down its debt. It would require abandoning its global empire, however. And trimming domestic social welfare programs too. Politically, it is impossible to make those changes; like an alcoholic, the country will have to ‘hit bottom’ first….

That leaves inflation as the only real option. The feds know that. They need to get the inflation rate up, not down, so that the real value of the government’s debt goes down to a more manageable level. That’s why, even with inflation at twice the Fed’s target, Powell is still insisting that the next move will be to lower rates, not raise them.

The public may not want higher prices. But the people who matter do – Big Money, Big Business, and Big Government. Stay tuned.

It certainly appears Powell is moving that way. In the very least, he’s trying to help the government keep its interest rates below that 5% line., but he’s doing it by jawboning down bonds, not with looser policy because that would be huge public cave-in on inflation that would be impossible to answer for with inflation rising.

So, the market is not going to get what it wants as soon as it wants it. There are other signs of a tipping point being reached to report on, too:

One writer on Seeking Alpha points out:

Three key indicators that measure investor expectations for the SPX are suggesting a major top is coming. As you'll see, all three points to an "extreme" degree of bullish sentiment in the universe of traders who trade the SPX. They are all indicating the same thing - the soon ending of this bull market and/or the beginning of a major correction….

Up to 50% or more of an asset's price, either up or down, can be driven by the emotions of fear and greed alone….

History has taught us that prices will move opposite what investors expect when "too many" investors have that expectation. I want to emphasize this last point: The theory applies only when those expectations have reached an extreme….

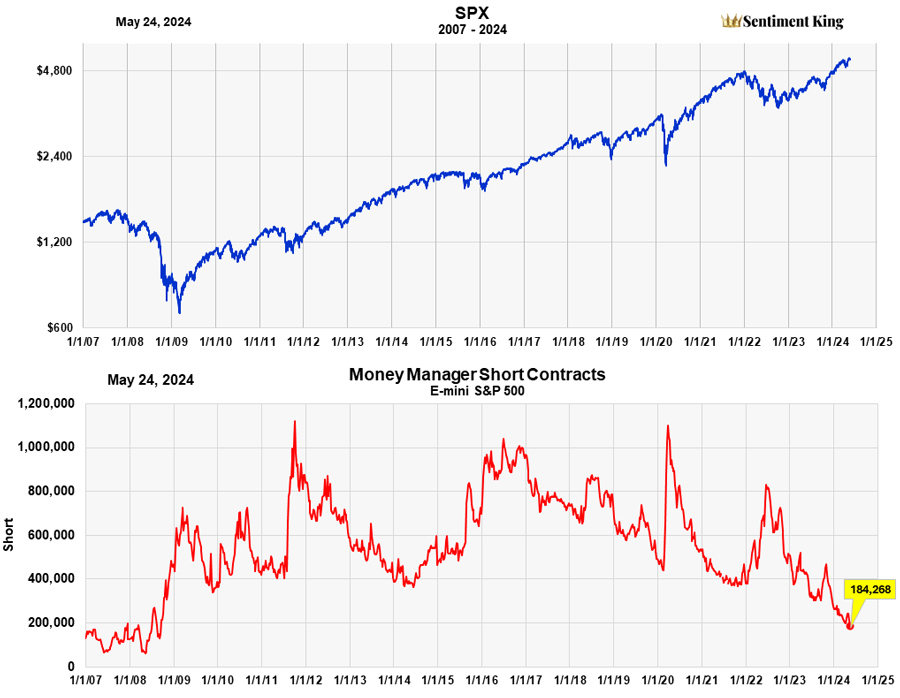

Professional SPX Money Managers Aren't Shorting This Market….

There are now simply "too many" bulls and far "too few" bears.

Study the chart. It's obvious that … low short positions occur at market peaks.

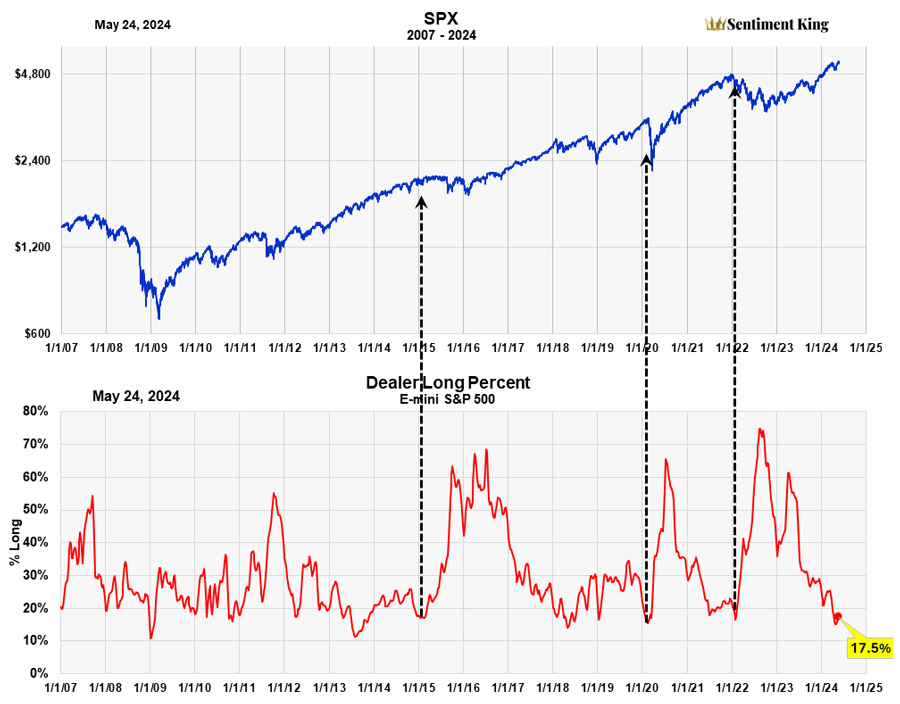

Dealer's long positions are just 17.5% of their total. This is highlighted in yellow in the chart below.

We believe it is highly probable the SPX will have a zero return over the next nine months, and a negative return over the next eighteen….

While we believe the market has begun the actual topping process (which could take months), we still think the actual peak in the SPX index will be in August.

Says another Seeking Alpha writer

The recent Guardian/Harris poll finds that most Americans think that the US economy is in a recession. This is corroborated with the recent sharp drop in the Michigan Consumer to sub-70, which is consistent with the recessionary readings. In fact, consumer confidence has been at recessionary levels since 2022….

In addition, businesses also think that the US economy is in a recession. The ISM manufacturing index has been in contraction (sub 50 level) since November 2022. In addition, the ISM service PMI index just dipped in contraction (sub 50) in April 2024.

So, everybody thinks we're in a recession now, the majority of people, managers of manufacturing firms, and managers or services firms.

The truth of this, I just wrote about in my latest “Deeper Dive: Record-Shattering Stealth Recession Approaching.”

Because it is a stealth recession, there is a huge …

disconnect between what managers and consumer think/feel, and what the official data is showing….

The S&P 500 (SP500) is primarily pricing earnings growth, and in a recession, earnings drop by 10-15%, which results in a recessionary bear market.

The consumer and manager surveys indicate the perception that we are in recession or contraction. And yet, the earnings expectations growth for the S&P 500 is 9.5% for 2023 and 14% for 2025.

There is clearly a disconnect. The earnings growth projections are likely irrational, as this would require a perfect soft-landing, where inflation falls, the Fed cuts, and consumer sentiment rises.

However, the consumer is telling us that a brief period of deflation will be necessary - and that means a recession. Thus, the S&P 500 is facing a recessionary bear market.

(Note that Seeking Alpha articles require a membership, so I have not included them in the headlines below, but I did put links in the texts above for those who have such memberships.)

Share

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world.

www.thedailydoom.com

|