|

A Great Example of the Coming Financial Repression

Imagine you are one of two people playing Monopoly. While you follow the rules religiously, the other player, who also happens to be the banker, does not. He routinely appropriates properties. If he doesn’t like the score on the dice, he simply changes them. He continually takes as much money from the bank as he likes. Whenever the rules don’t suit he arbitrarily alters them in his favour. Oh, and he hates to lose. Rather than concede defeat, he is perfectly willing to set fire to the table. Imagine no longer. This is the state of the financial markets. You are playing against the world’s central banks. For some time now, the Financial Times has been running articles (under the inauspicious label of ‘Collateral Damage’) discussing the merits or demerits of central banking. Only one contributor, Ron Paul, has challenged the status quo:

Every other contributor thus far has sought to defend central banking as a necessary part of the system… a view that seems categorically embraced by most people. In browsing through the comments of Dr. Paul’s FT article, for example, one reader posted:

No, I wouldn’t. But I wouldn’t trust an economic diagnosis from any of those individuals either. Given their track records, why would anyone? Getting rid of central banks (over time, let us be realistic) would have several effects. First, it would require insolvent commercial or investment banks to fail properly, as opposed to feeding off the blood of taxpayers indefinitely.

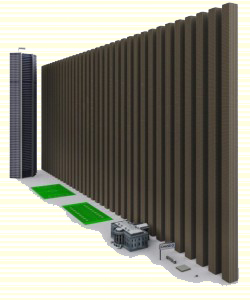

As an example, lest anyone regard the $2 billion loss recently announced by JP Morgan as comparatively trivial, it should perhaps be seen in the context of the same bank’s overall derivatives exposure, which is shown graphically below. JP Morgan’s total derivatives exposure stands at $70.1 trillion, or roughly the same size as the entire world economy. Each of the $1 trillion towers in the image is double-stacked to a height of 930 feet (283 meters). Second, eliminating central banks would require governments to balance their books, no longer able to monetize the debt through its relations with the central banker. Third, asset prices would revert to being determined by the market, and not by unelected economist serving the interests of bankers and politicians. As this is clearly not going to happen anytime soon, most investment managers seem content to embrace the system and continue playing the cards they’ve been dealt. To give you an example, the FT reported that, last year, US pension funds for the very first time put more of their assets into bonds as opposed to equities. Like many investors, these fund managers fail to understand the risks they’re running and seem to have accepted the convention that nothing could possibly go wrong while central bankers are in charge. Yet with Treasury yields as low as they are, this is unlikely to end well. The chart below shows the impact on investors who purchased British Gilts during the stagflation suffered in the UK during the 1970s. |

|

|