Peace Won’t Fix This: The Closure of the Strait of Hormuz Has Already Done Its Damage

Graham Summers

As I’ve outlined previously, the most critical aspect of the conflict in Iran pertains to the Strait of Hormuz, a narrow (~30 miles wide at its narrowest point) critical shipping lane for global energy supplies: 20% of the world’s oil and liquified natural gas (LNG) supplies pass through this lane. As I’ve outlined previously, the most critical aspect of the conflict in Iran pertains to the Strait of Hormuz, a narrow (~30 miles wide at its narrowest point) critical shipping lane for global energy supplies: 20% of the world’s oil and liquified natural gas (LNG) supplies pass through this lane.

You’ve likely heard references to the Strait being “closed” in the media. To be clear, this reference is not to say that Iranian warships or soldiers are physically stopping oil/LNG tankers from shipping through this passage. Rather, the threat of drone/ missile strikes from Iran has resulted in insurancecompanies refusing to cover ships, which in turn is leading to shipping companies opting to NOT take the risk of passing through the Strait.

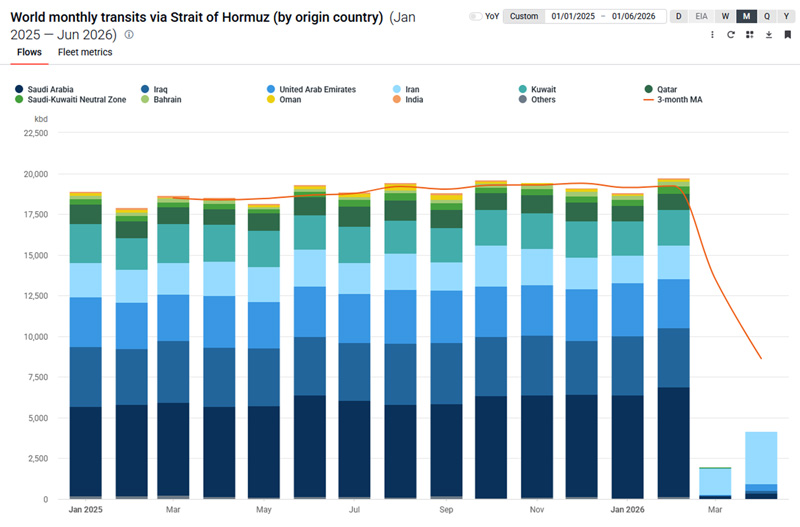

As the below image illustrates, there has been a massive decline in shipping through the Strait since the conflict in Iran began in early March.

This situation is EXTREMELY complicated encompassing numerous issues. In broad strokes:

- The world had energy inventories in place before the conflict started. So, it’s not as if the war started and POOF energy supplies were gone. According to my research global oil inventories stood at 8.2 billion barrels of oil in January 2026 (the world uses about 103 million barrels of oil per day, so this comes to ~80 days’ worth of global supplies).

- There are alternate shipping routes for oil/ LNGs in the Middle East.

- In terms of pipelines there are the:

- Saudi East-West Pipeline (Petroline)

- UAE Abu Dhabi Crude Oil Pipeline (ADCOP / Habshan-Fujairah)

- Iraq-Turkey (Kirkuk-Ceyhan) Pipeline

- Iran’s Goreh-Jask Pipeline

- In terms of shipping routes there are:

- UAE East Coast Ports (Fujairah & Khor Fakkan)

- Omani Ports

- Red Sea Ports (Saudi Arabia)

- The Cape of Good Hope

- There is considerable oil/ LNG sitting in tankers in the Persian Gulf. Some analysts put this amount at ~180 million barrels of oil. This can and should start shipping shortly now that a ceasefire has been announced.

- Even in the ideal situation (shipping traffic returns to 100% immediately and is not disrupted again), tankers need to travel and then be emptied. Depending on their final destinations it will take 30-45 days for oil to arrive.

- Oil producing nations have reduced production in response to the Strait being closed. The current estimate for “shut-in” production for the month of April is ~330 million barrels.

- Onshore storage units will need to be drained (oil producing nations have been storing oil rather than shipping it) before oil production in the Middle East can return to full capacity.

- The world has released Strategic Petroleum Reserves (SPRs) to counteract the drop in shipping through the Strait. The release for the month of April is anticipated to be 75 million barrels of oil.

- Finally, Iran may or may not introduce a toll fee to ships passing through the Strait of Hormuz. If they do, how much will it be? And how many countries will accept this?

And so on.

My point with the above outline is that this is an EXTREMELY complicated situation to navigate even if the cease-fire holds, peace breaks out, and there are no more disruptions to oil production or shipping in the region.

Having said that, the main takeaway is clear: significant damage has been done to global oil supplies. According to HFI Research (a firm that specializes in energy/ oil analysis) even if the Strait of Hormuz is 100% open/ back to normal by April 30th, the total production outage related to the Strait closing will be ~1.12 BILLION barrels of oil.

This means that higher oil prices will remain in place for at least the intermediate future. And this has major implications for inflation and the U.S. economy even if stocks continue to rip higher.

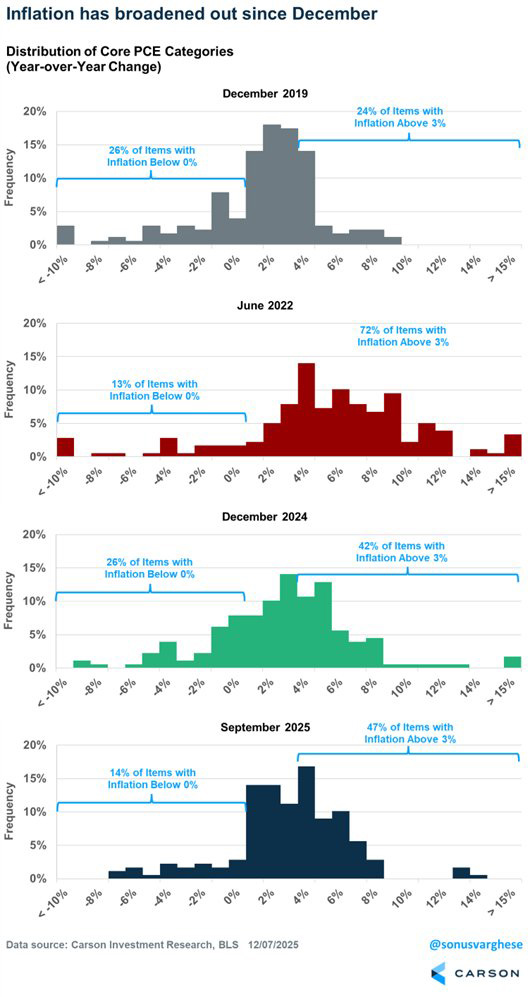

The reality is that the U.S. was primed for another wave of inflation BEFORE the war in Iran began. The Fed’s preferred inflation measure is the Core-Personal Consumption Expenditures (Core PCE). Core PCE has 178 components within it. As Ryan Detrick notes, 54% of these components are clocking in at over 3% right now.

Last year it was just 45%.

Put simply, inflationary pressures are broadening. And again, this was before the conflict in Iran ignited oil prices which will have significant inflationary implications.

Smart investors are moving now to prepare for it.

On that note, we just published a Special Investment Report concerning FIVE secret investments you can use profit from the next major bull run in precious metals miners.

The report is titled Survive the Inflationary Storm. And it explains my top precious metals plays, including their names, their symbols, and the resources they own. These are HIGH OCTANE positions that rallied 75%, 140%, 150%, 180%, 280% and an incredible 574% in 2025! And I wouldn’t be surprised to see them repeat this performance in 2026.

Normally I’d charge $499 for this report as a standalone item, but in light of what is unfolding today, we are making just 100 copies available to the public.

To grab one of the last remaining copies…

CLICK HERE NOW!

Graham Summers, MBA is Chief Market Strategist for Phoenix Capital Research, an investment research firm based in the Washington DC-metro area.

Graham’s sterling track record and history of major predictions has made him one of the most sought after investment analysts in the world. He is one of only 20 experts in the world who are on record as predicting the 2008 Crash. Since then he has accurately predicted the EU Meltdown of 2011-2012 (locking in 73 consecutive winners during this period), Gold’s rise to $2,000 per ounce (and subsequent collapse), China’s market crash and more.

His views on business and investing has been featured in RollingStone magazine, The New York Post, CNN Money, Crain’s New York Business, the National Review, Thomson Reuters, the Fox Business, and more. His commentary is regularly featured on ZeroHedge and other online investment outlets.

gainspainscapital.com

|