Send this article to a friend:

April

12

2025

|

Send this article to a friend: April |

|

Is Sound Money Politically Impossible?

But if we don’t have sound money what is it we’re using? It goes by the name of fiat money — paper or digits without economic value in themselves. Gold has various non-monetary uses, such as jewelry, technology and medicine. Fiat money? In some cases it’s been a source of poignant creativity. Photos from the German hyperinflation of 1923, such as a lady wearing a dress made from nearly worthless currency, entertains onlookers while trying to remind them of a tragedy. (At one point 4.2 trillion marks equaled one American dollar.) Insanity at this level is only possible when the state shows up with legal tender laws, thereby forcing market participants to accept its depreciating currency. If money holds the potential to control resources or acquire property, then fiat money, even if it loses value by the hour, qualifies as a medium of exchange. Aside from occasional excesses such as in Weimar Germany, should we care whether money is sound or not? People who sit on the FOMC are well-qualified academically and many have banking and investment experience which in some cases is global. Surely they know what’s best for the economy and whether interest rates need adjusting — notwithstanding their Smith-Hayek “conceit” and generations of evidence to the contrary. In past years one of them has even been sympathetic to a gold standard — Alan Greenspan, author of the insightful 1966 article “Gold and Economic Freedom,” who served as Fed chairman from 1987 to 2006. Greenspan, in fact, was more than sympathetic. In discussing the Fed’s monetary policy of the 1920s, he slammed the “paper reserves” the Fed used to augment gold deposits, which “nearly destroyed the economies of the world.” His article was brilliant and original in many respects, condemning deficit spending as “a scheme for the confiscation of wealth” and that without “the gold standard, there is no way to protect savings from confiscation through inflation.” But his comments on the banks’ practice of fractional reserve banking leaves me wondering if he actually understood it: Individual owners of gold are induced, by payments of interest, to deposit their gold in a bank (against which they can draw checks). But since it is rarely the case that all depositors want to withdraw all their gold at the same time, the banker need keep only a fraction of his total deposits in gold as reserves. Lost in his explanation is any distinction between demand deposits and time deposits, though he could hardly be faulted for not mentioning it. Thanks to a series of rulings beginning with Carr v. Carr 1811 UK a banker was no longer considered a custodian or bailee in any deposit contract, obligated to return the funds deposited on demand. The law made the banker a debtor, and though required to “repay the principal” the deposited money was his “to do with as he pleases.” (Foley v Hill and Others 1848). The distinction between a warehouse bank and a loan bank was thus discarded over time. Banks own the money you deposit and it immediately becomes subject to bank-lending multiplication. As with any debtor they may or may not have it when you claim it, though the public counts on it being there at all times. In the UK, MP Douglas Carswell introduced a bill in 2010 aimed at ending fractional reserve banking by declaring there would “henceforth be two categories of bank account: deposit-taking accounts for investment purposes, and deposit-taking accounts for storage purposes.” If enforced, this transformation would eliminate the maturity mismatch between assets and liabilities and force credit expansion from real savings only. The public would need to be aware that a time deposit was a loan to a bank, with the usual risks it entails. Banks would operate without legal privileges, the one thing they have sought to avoid through a fiat system of central banking and deposit insurance. The Carswell bill, of course, did not progress beyond its first read and lapsed soon after. (The bill had an innocent-sounding title: To prohibit banks from “lending on the basis of demand deposits without the permission of the account holder.” Banks could argue that the bill would force them to charge a fee that account holders could avoid by granting permission to lend their deposits in exchange for “free” banking, Banks could promote their spotless records in recent times and claim depositors had nothing to gain and something to lose by withholding permission. To the public whose money would constitute the deposits, granting permission would seem a no-brainer — though the British public might know better.) Tricks of the (government) trade Article IX of the Articles of Confederation says

Nowhere is there a mention of paper money, the abuses of which led to Shay’s Rebellion and helped excite interest in a Constitutional Convention. One might hope the Constitution would clear up the matter. James Madison wrote in Federalist No. 44: “The power to make any thing but gold and silver a tender in payment of debts, is withdrawn from the states, on the same principle with that of striking of paper currency.” The Constitution, following Madison’s comments, says in Article 1, Section 10: “No State shall… coin Money; emit Bills of Credit; make any Thing but gold and silver Coin a Tender in Payment of Debts…”. States, therefore, could not print their own money or make anything other than gold and silver coin legal tender. But the door was open for Congress to authorize or forbid issuing paper money. Subsequent court cases (particularly Knox v. Lee, 1871) settled the matter, giving Congress the power to issue fiat money even in peacetime. Conclusion Is sound money today a political possibility? Mises defined sound money in chapter 21 of his Theory of Money and Credit:

Franz Oppenheimer defined the constitutional State this way: Let us give the mechanics and kinetics of the modern state a moment’s time. In principle, it is the same entity as the primitive robber state or the developed feudal state. (p. 124) Both Mises and Oppenheimer are right. We are ruled by thieves, and sound money is no advantage to these looters. The road to a true sound money economy will require a collapse of the political institutions obstructing it.

|

Send this article to a friend:

|

|

|

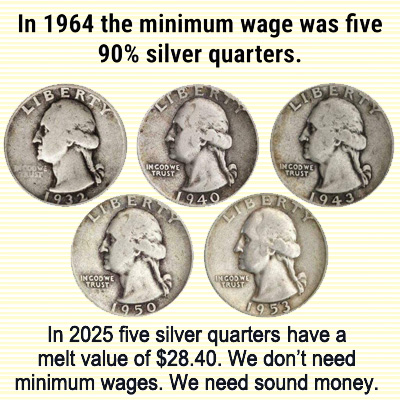

Apparently sound money has no meaning for those controlling the money supply, which is purported to be in the hands of the Federal Open Market Committee (FOMC) of the Federal Reserve System.

Apparently sound money has no meaning for those controlling the money supply, which is purported to be in the hands of the Federal Open Market Committee (FOMC) of the Federal Reserve System.