Send this article to a friend:

March

23

2016

|

Send this article to a friend: March |

|

Janet Yellen: Monetary Arsonist - Armed, Dangerous And Lost

Given the overwhelming facts on the ground - 4.9% unemployment, 2.3% core CPI and a 23.7X PE multiple on the S&P 500 - her decision to “pause” after 87 months of ZIRP actually proves she is a blindfolded monetary arsonist - armed, dangerous and lost. That’s right. In the midst of vastly inflated and combustible financial markets, the all-powerful Fed is being led by a Keynesian school marm stumbling around in an explosives vest. She apparently has no idea that a 38 bps money market rate is not a pump toggle on some giant bathtub of GDP; it’s an ignition fuse that is fueling the greatest speculative mania in modern history. Janet and her posse of pettifoggers don’t even have the “Humphrey-Hawkins made me do it” excuse any longer. The truth is, there is nothing in the act that says they must hit 2.00% inflation to the second decimal point or anything else more specific than “stable prices”. Nor is there any quantitative target for full employment, let alone something like 4.85%—- since we apparently are not there at 4.90%. But even if these targets are taken as a serviceable approximations of its so-called ‘dual mandate’, who in their right would be quibbling about the second decimal point so late in the recovery cycle that the next recession is fairly palpable? Indeed, now that they have dot-plotted their way down to only two raises this year—which will soon turn into one owing to the fraught politics of this election year—–here is where we will end in December. To wit, the money market interest rate will have been effectively at the zero bound for 96 months. That’s longer than every post-war business recovery except LBJ’s guns and butter blow-off in the 1960s, which didn’t end well, and the 1992-2000 tech boom, where there is not a chance of repetition in either this world, or the next. Among other things, the central banks were just discovering their printing presses back then and there was only $40 trillion of credit outstanding on the planet, not today’s $225 trillion albatross.

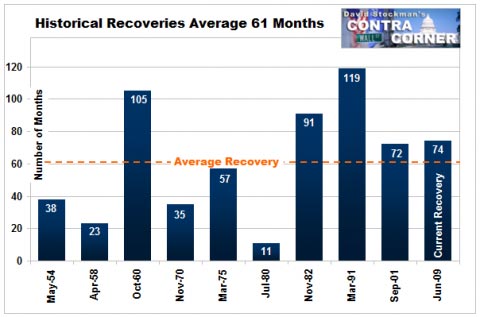

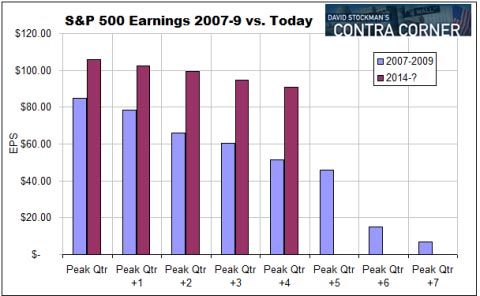

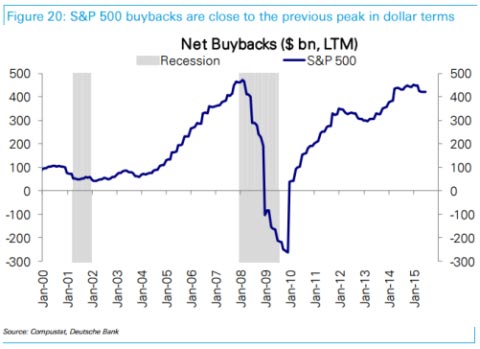

Historical Length of Recoveries The fact is, the Fed doesn’t have a snowball’s chance of ultra-fine tuning to the second decimal place the nation’s $18 trillion GDP. Not in the context of today’s bloated, bubble-ridden global economy that is now sliding into an epic deflation. After 20 years of relentless money printing by the central banks and pell-mell credit creation throughout the world economy there exists massive over-investment, malinvestment and unserviceable indebtedness. On the margin, it is this overhang which will drive worldwide commodity and goods prices, CapEx, industrial output and the general level of profits, incomes and consumer inflation. The idea that 25 basis point moves in the New York money market can hold a candle to these massive planetary forces is truly laughable. It is not the FOMC that matters now. The world’s $225 trillion credit bubble is already in place and the resulting glacial distortions and deformations can’t be recalled. What is in the driver’s seat, therefore, is tens of millions of redundant employees in China’s faltering rust belt and its global supply chain, and hundreds of billions of sunk and wasted capital there and throughout the EM. It is these stranded loss-making investments in mining, energy, shipyards, steel mills, car factories, construction faciltities, ports, warehousing and distribution and much more that will result in massive capital losses, defaulted debts and sinking profits and incomes. Needless to say, the present great deflation is occurring on a worldwide basis. The idea that the US domestic economy has somehow been “decoupled” is simply one more Wall Street whopper. In that respect, Simple Janet is lost in a time warp. The 1960’s notion that the US economy is a closed bathtub in which inflation, unemployment and all of the other crude, ill-measured macro-variables on Janet’s dashboard can be mushed around by central bank injections of ethers called “aggregate demand” and “financial accommodation” was not true even back then. That is, when Yellen was being mis-educated by Professor James Tobin and the rest of the Keynesian professoriate of that bygone era. And that isn’t the half of it. It was also never true that the financial market is merely a neutral transmission channel to the main street economy that can be used as a pumping device to manage GDP and the dual mandate variables embedded in it. In fact, financial markets are the delicate mainspring of the entire capitalist economy. The nuances of pricing in the money and debt markets, the exact shape of the yield curve, the cost of carry and maturity transformations, the price of options and hedging insurance, capitalization rates on earnings and cash flows and much more are what actually enable sustainable growth, real wealth creation and financial stability. But the blunderbuss Keynesians who have taken control of the Fed and other central banks lock, stock and barrel are clueless. Their massive, chronic, heavy-handed intrusions in financial markets have falsified all prices and turned the financial markets into incendiary gambling casinos. There is no true price discovery left—-just an endless cycle of speculation and front-running that eventually reaches a breaking point and implodes. We are there now. At today’s close, the S&P 500 was valued at nearly 24X the reported GAAP profits for the year just ended. That is crazy under any circumstances, but especially so in a context were corporate profits are literally cliff-diving. That’s right. S&P 500 profits peaked 18 months ago during the LTM period ending in September 2014. Reported GAAP profits clocked in at $106 per share compared to just $86.44 per share in the most recent LTM period. Yes, profits are down 18.5% from the cycle peak, and heading lower this quarter and for as far as the eye can see, yet at 24X the casino is trading in the nosebleed section of history. After a prospective 96 months of ZIRP what else could be expected? Simple Janet strapped on an explosive belt long ago. In fact, corporate earnings have been dropping for five quarters, notwithstanding record stock buybacks and continued shrinkage of the float. As we learned in 2007-2009, denial can persist only so long; it’s only a matter of time before the bubble blows.

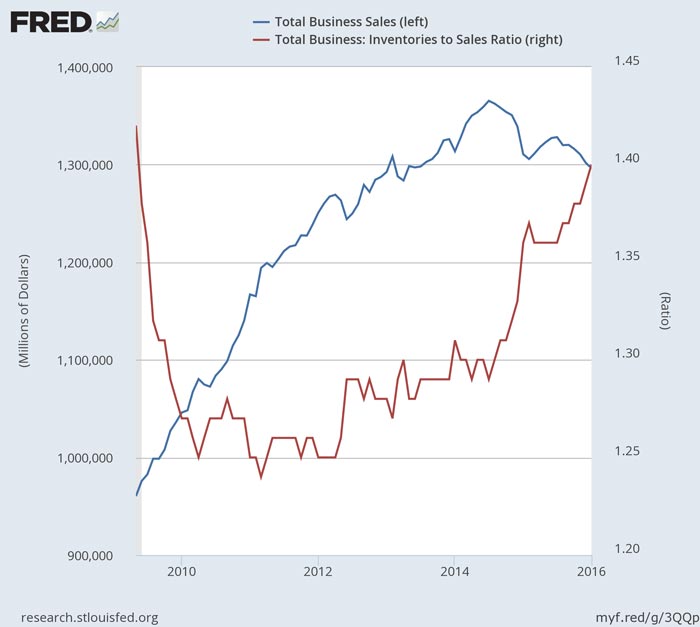

Worse still, it is also only a matter of time before the next recession sends profits plummeting. The economy, in fact, is already rolling over. Total business sales are down 5.1% from their mid-2014 peak and the inventory-to-sales ratio has retraced to the recessionary levels of June 2009. Business Sales Down 5.1%, Inventory Ratio At June 2009 Recession Level

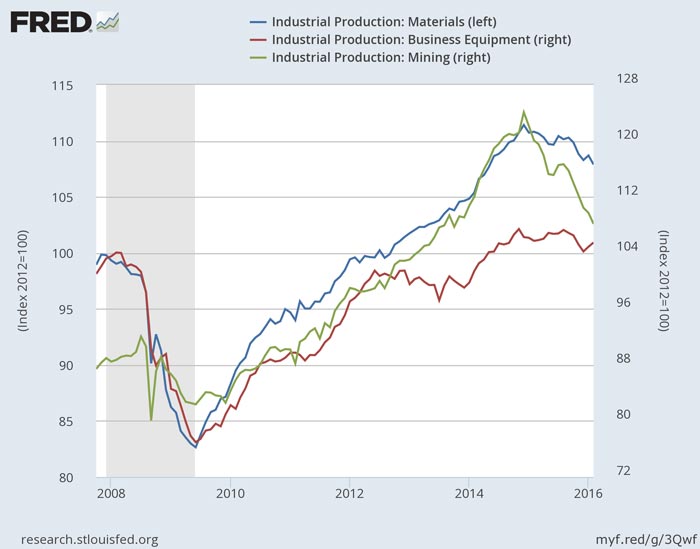

Likewise, during the first 10 weeks of 2016, rail shipments have been 5.5% lower than prior year. Industrial production is also heading south in numerous categories including energy and mining, industrial materials and capital equipment.

The real day of reckoning can’t be far behind.

At the podium, Stockman’s expertise and experience cannot be matched, and he has a reputation for zesty financial straight talk. Defying right- and left-wing boxes, his latest book catalogues both the corrupters and defenders of sound money, fiscal rectitude, and free markets. Stockman discusses the forces that have left the public sector teetering on the edge of political dysfunction and fiscal collapse Stockman’s career in Washington began in 1970, when he served as a special assistant to U.S. Representative, John Anderson of Illinois. From 1972 to 1975, he was executive director of the U.S. House of Representatives Republican Conference. Stockman was elected as a Michigan Congressman in 1976 and held the position until his resignation in January 1981. He then became Director of the Office of Management and Budget under President Ronald Reagan, serving from 1981 until August 1985. Stockman was the youngest cabinet member in the 20th century.

davidstockmanscontracorner.com

|

|---|

Send this article to a friend:

|

|

|

Simple Janet should have the decency to resign. The Fed’s craven decision last week to punt on interest rate normalization is not merely a reminder that she is clueless and gutless; we already knew that much.

Simple Janet should have the decency to resign. The Fed’s craven decision last week to punt on interest rate normalization is not merely a reminder that she is clueless and gutless; we already knew that much.

David Stockman is the ultimate Washington insider turned iconoclast. He began his career in Washington as a young man and quickly rose through the ranks of the Republican Party to become the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street.

David Stockman is the ultimate Washington insider turned iconoclast. He began his career in Washington as a young man and quickly rose through the ranks of the Republican Party to become the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street.![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)