Send this article to a friend:

February

03

2023

|

Send this article to a friend: February |

|

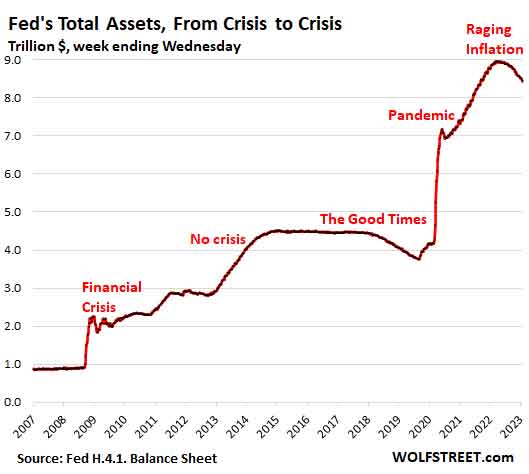

Fed’s Balance Sheet Drops by $532 Billion from Peak,

QT is starting to make a visible dent. The Federal Reserve has shed $532 billion in assets since the peak in April, with total assets falling to $8.43 trillion, the lowest since September 2021, according to the weekly balance sheet released today. Compared to the balance sheet a month ago (released January 5), total assets dropped by $74 billion. Quantitative Tightening is starting to make a visible dent:

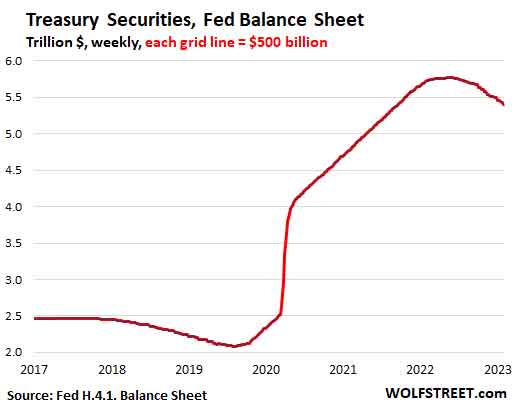

Treasury securities: -$374 billion from peak. Since the peak in early June, the Fed’s Treasury holdings fell by $374 billion to $5.34 trillion, the lowest since September, 2021. Over the past month, the Fed’s holdings of Treasury securities fell by $60.4 billion, a hair above the cap of $60 billion. Treasury notes and bonds come off the balance sheet when they mature mid-month and at the end of the month, which is when the Fed gets paid face value for them. The monthly roll-off is capped at $60 billion.

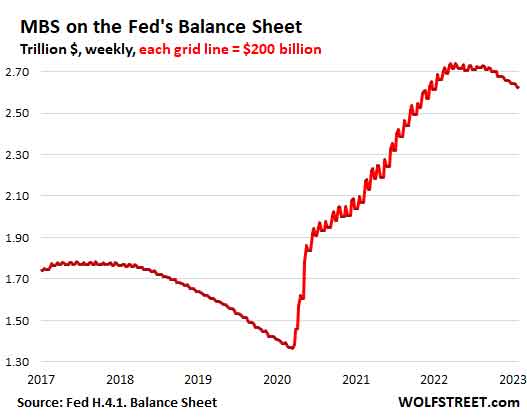

Mortgage-backed securities: -$115 billion from peak. The Fed has shed $115 billion of MBS since the peak, including $17 billion over the past month, with the total balance dropping to $2.62 trillion. Each month since QT started, the total amount in MBS that came off the balance sheet was well below the cap of $35 billion. MBS come off the balance sheet primarily as a function of the pass-through principal payments that all holders receive when mortgages are paid off, such as when mortgages are refinanced or when mortgaged homes are sold, and as regular mortgage payments are made. As mortgage rates have spiked from 3% to over 6%, people are still making their mortgage payments, but mortgage refi volume has collapsed and home sales have plunged, and the torrent of pass-through principal payments has fizzled. Pass-through principal payments reduce the MBS balances, which show up as the downward zigs in the chart below. The upward zags in the chart occurred back when the Fed was still buying MBS, but it stopped this sordid practice entirely in mid-September, and the upward zags in the chart petered out.

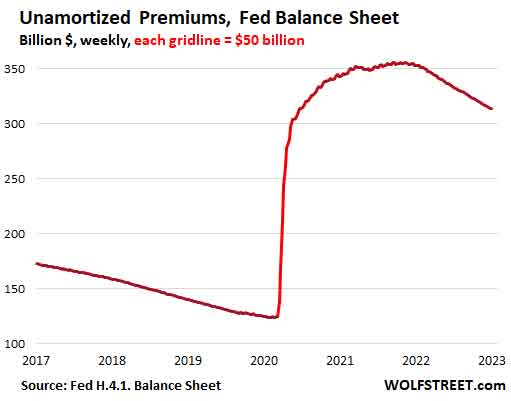

Selling MBS outright? We’re still waiting for the Fed to give any indication that it is seriously considering selling MBS outright to bring the roll-off up to the cap of $35 billion a month. At the current rate, it would have to sell $15 billion to $20 billion a month to get to the cap. Several Fed governors have mentioned that the Fed might eventually move in this direction. Note in the chart above that in 2019 and 2020, MBS rolled off the balance sheet at the pace of the cap as dropping mortgage rates caused refis and home sales to surge. QT-1 ended in July 2019, but MBS continued to roll off through February 2020, and the Fed replaced them with Treasury securities, whose balance began to rise again in August 2019, as you saw in the prior chart. The Fed has said many times that it doesn’t like to have MBS on its balance sheet, in part because the cashflows are so unpredictable and uneven, which complicates monetary policy, and in part because holding MBS gives preference to one type of private-sector debt (housing debt) over other types of private-sector debt. This is why we may see some serious discussions soon about selling MBS outright. Unamortized Premiums: -$45 billion from peak.Unamortized premiums dropped by $3 billion for the month and were down by $45 billion from the peak in November 2021, to $311 billion. What is this? The securities that the Fed bought in the secondary market, at a time when market yields were lower than the coupon interest of the securities, the Fed, like everyone else, had to pay a “premium” over face value. But when the bond matures, the Fed, like everyone else, gets paid face value. In other words, in return for the above-market coupon interest payments, there will be a capital loss in the amount of the premium when the bond matures. Instead of booking the capital loss when the bond matures, the Fed amortizes the premium in small increments every week over the life of the bonds. The Fed accounts for the remaining premiums in a separate account.

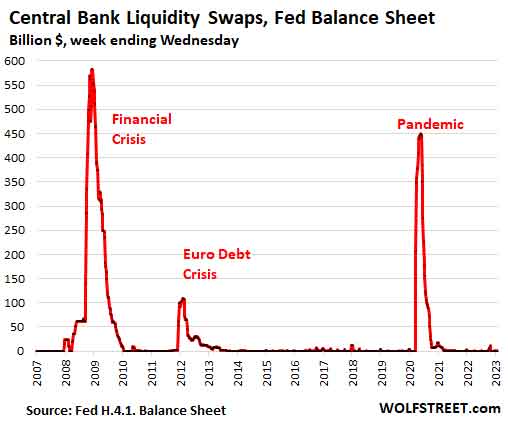

Keeping an eye on potential warning signs. Central Bank Liquidity Swaps.The Fed has long had swap lines with major other central banks, where that central bank can swap local currency for US dollars with the Fed, via swaps that mature over a certain time period, such as seven days, at which point the Fed gets its dollars back and the other central bank gets its currency back. There are currently only $427 million (with an M) in swaps outstanding:

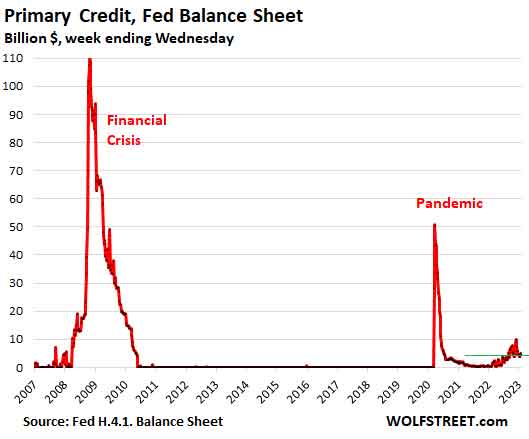

“Primary Credit” – the Discount Window. The Fed lends money to the banks at the “Discount Window,” for which it charges banks 4.75% in interest, following the rate hike yesterday. So this is expensive money for the banks. They could borrow money for much less if they can attract depositors. So having to borrow at the discount window at this high rate would cause eyebrows to be raised. About a year ago, Primary Credit started rippling higher just a little, and at the end of November 2021 hit a still small $10 billion. In mid-January, the New York Fed published a blog post, “The Recent Rise in Discount Window Borrowing.” It didn’t name names, but surmised that mostly small banks were coming to the discount window, and that quantitative tightening may have temporarily reduced their liquidity positions. But borrowing at the Discount Window has dropped off since November, and today the balance was $4.7 billion. Just keeping an eye on it:

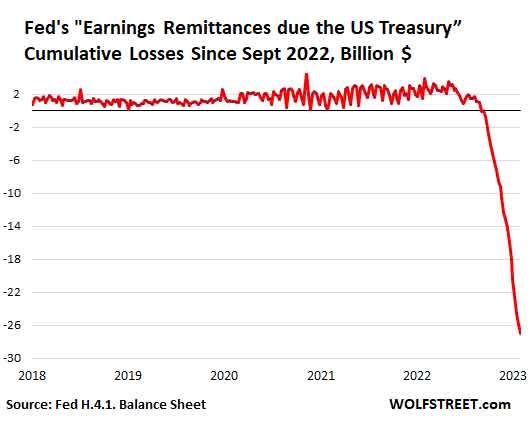

The Fed’s cumulative losses. The Fed’s vast securities holdings are usually a money-making machine. And they still are, but last year, it started paying much higher interest – as it began hiking rates – on the cash that banks deposit at the Fed (“reserves”) and on the cash that mostly Treasury money market funds send the Fed via overnight reverse repurchase agreements (RRPs). Since September, the Fed started paying out more in interest on reserves and RRPs than it was making in interest on its securities. From September through December 31, the Fed lost $18.8 billion, but it had made $78 billion from January through August, and so for the year as a whole, it still had a net income of $58.4 billion. Last month, it reported that itremitted its income through August of $78 billion to the US Treasury, which the Fed is require to do. Those remittances stopped with the losses starting in September. The Fed tracks those losses weekly in an account, called “Earnings remittances due to the U.S. Treasury.” The cumulative losses since September reached $27 billion on the current balance sheet. But don’t worry. The Fed creates its own money and can never run out of money, and can never go bankrupt, and how to deal with these losses is just an accounting question. It solved the question by treating the losses like a deferred asset and putting it in the liability account, “Earnings remittances due to the U.S. Treasury.” With the losses squared away in the liability account, the Total Capital account has remained unchanged at roughly $41 billion. In other words, the losses will not deplete Fed’s capital. Funniest looking account — in more than one way — on the Fed’s balance sheet:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)